Most advice on supply chain risk management still treats disruption as an external shock. Something unexpected happens, freight slips, a factory misses a shipment, customs holds stock, and the business scrambles. That framing is comfortable because it implies the problem arrived from outside.

In practice, international expansion usually exposes weaknesses that were already there.

A brand can perform well in one market while carrying hidden operational fragility for years. Local replenishment windows may have been forgiving. A narrow supplier base may have worked because volumes were predictable. Compliance may have been manageable because the product only moved through one regulatory environment. Once that same brand starts pushing into overseas marketplaces, those assumptions break fast. Listing quality and advertising don't fix a supply chain that can't absorb distance, complexity, or variance.

The Hidden Costs of International Marketplace Expansion

The most common mistake is believing supply chain failure sits in the category of rare events. It doesn't. Gartner has reported that 89% of companies experienced a supplier risk event in the past five years, which is widely cited as evidence that disruptions are routine operating conditions, not exceptional ones, as noted in this supply chain risk management analysis.

That matters because international marketplace expansion multiplies the number of places a brand can fail.

Growth exposes what domestic trade can hide

A business can look operationally sound in Australia and still be structurally unprepared for the UK, US, or Canada. One issue we repeatedly observe is that founders often invest first in channel entry mechanics. Listings, ads, account setup, creative, and marketplace launch planning. Those matter, but they sit downstream of a harder question. Can the business consistently land, clear, store, replenish, and support the product without margin damage?

When the answer is no, the hidden costs emerge:

- Stockouts become brand damage: Marketplace customers don't separate product quality from fulfilment reliability.

- Rush freight distorts margin: A profitable SKU can become a weak one once emergency logistics enters the picture.

- Compliance gaps stall momentum: A product that sells well domestically may still trigger friction in a new market.

- Supplier drift becomes visible: Quality inconsistency that was tolerable at lower volume becomes commercially dangerous during expansion.

Practical rule: If a brand's supply chain only works when everything goes to plan, it isn't expansion-ready.

This is also where profitability starts slipping for reasons many teams misread. The catalogue may be strong. Demand may be real. Yet the business still underperforms because operational instability forces expensive decisions later. The margin pressure discussed in why products can sell on Amazon but still make less money often begins long before the sale, inside the supply model itself.

Fulfilment confidence is part of brand credibility

Across multiple marketplace ecosystems, stronger brands tend to share one trait. They don't treat fulfilment as a back-end service function. They treat it as part of the customer promise and part of market-entry strategy.

That changes how they view supply chain risk management. Not as a procurement checklist. Not as a compliance file. As a commercial capability that protects service levels, margin integrity, and customer trust when the business enters a more fragmented environment.

International expansion doesn't create supply chain risk. It reveals how much unmanaged risk was already embedded in the business.

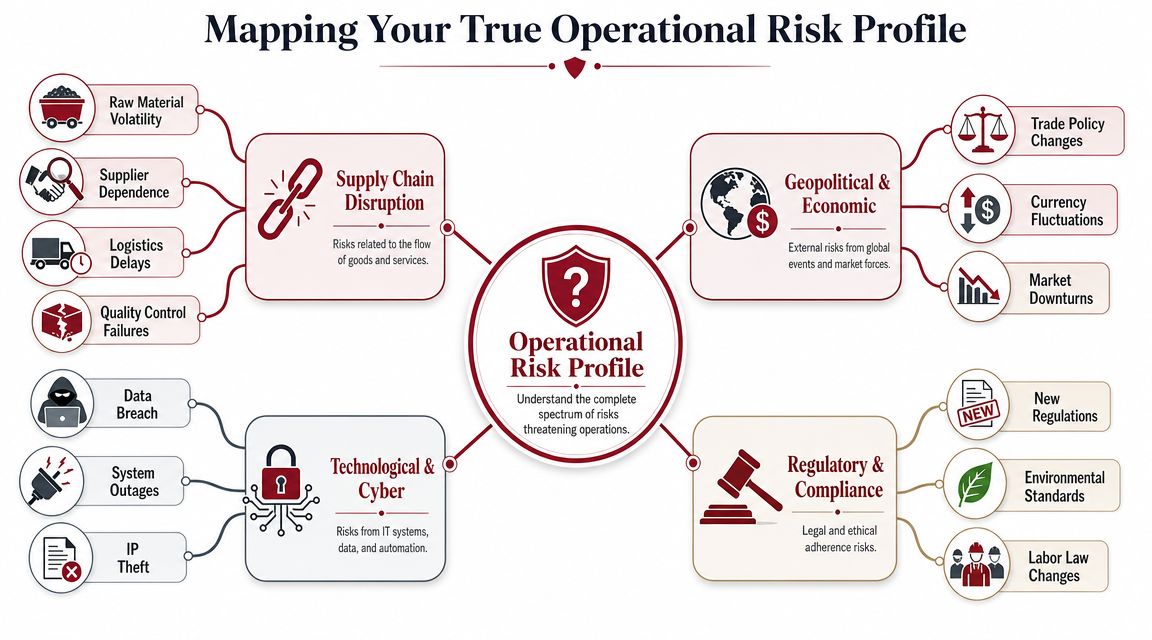

Mapping Your True Operational Risk Profile

Most brands don't have one supply chain risk problem. They have a cluster of smaller exposures sitting across suppliers, freight, compliance, systems, and product quality. The issue is that these exposures often get reviewed separately, while the commercial impact lands all at once.

The first job is to see the risk profile as a whole.

Supplier risk isn't just about factory failure

When operators hear supplier risk, they often think of shutdowns or insolvency. Those are obvious issues, but they're not the only ones that matter. A supplier can remain operational and still become commercially unstable.

Common patterns include:

- Quality drift: The factory keeps shipping, but tolerances loosen, materials change, or finish quality varies.

- Capacity conflict: Your supplier takes on a larger account and your production slot becomes less secure.

- Communication lag: Minor delays in answers create major delays in approvals, packaging sign-off, or remediation.

- Sub-tier opacity: The direct supplier looks stable, but a component maker or raw material source creates hidden dependency.

For hardware, household, and connected-product categories, this gets serious fast. A small component issue can trigger returns, poor reviews, and retailer friction across multiple channels at once.

Logistics risk sits closer to revenue than many teams realise

Australian brands are especially exposed to logistics risk because freight distance isn't a side issue. It's built into the model. That makes lane design, lead-time tolerance, and carrier optionality commercially significant.

One pattern we continue seeing is that brands describe logistics risk too broadly. "Freight delays" is not specific enough to manage. Operators need to separate ocean booking risk, transhipment risk, port dwell-time risk, customs clearance risk, domestic transfer risk, and final replenishment risk. Each has different triggers and different consequences.

For a broader expansion lens, this is tightly connected to global logistics strategy for international expansion. The supply chain doesn't just move product. It sets the cadence for pricing, inventory depth, and marketplace availability.

A useful second lens is operational visibility across teams.

The risk categories that usually hit expansion first

A practical risk profile for an established product brand usually needs at least these categories:

- Regulatory and compliance risk: Product labelling, chemical declarations, packaging standards, testing records, and import documentation can all block market entry or create post-launch exposure.

- Quality risk: Product failure in-market is rarely just a warranty issue. It affects review velocity, marketplace confidence, and return economics.

- Geopolitical and trade risk: Tariff changes, route instability, and policy shifts can alter landed cost assumptions after range planning has already been done.

- Technology and data risk: If forecasting, inventory, and supplier data sit in disconnected systems, the business reacts late even when warning signs exist.

- Commercial concentration risk: Overreliance on one supplier, one lane, one broker, or one warehouse can create brittle growth.

The brands that manage expansion best usually don't have fewer risks. They have clearer visibility on where those risks actually sit.

That distinction matters. Supply chain risk management becomes useful when it moves from generic concern to named exposure.

Developing a Structured Risk Assessment Framework

Many teams know their risks in conversation form. They can tell you that one supplier feels stretched, one freight lane is unreliable, or one market has awkward compliance requirements. The problem is that conversational risk doesn't allocate capital well. It leads to overreaction in one area and neglect in another.

A structured framework forces comparison.

Score risk by business consequence

The simplest version still works. Score each risk for likelihood and impact, then multiply the two to create a risk score. The point isn't mathematical precision. The point is disciplined prioritisation.

A useful way to think about impact for product brands is to go beyond delay. Ask what the risk would do to:

- Revenue continuity

- Gross margin

- Customer experience

- Marketplace account health

- Operational workload

- Brand credibility in a new region

That changes the quality of discussion immediately. A supplier issue that seems manageable in procurement terms may be severe once its effect on launch timing, review generation, and replenishment continuity is considered.

Example risk assessment matrix for a hardware brand

| Risk Type | Example Scenario | Likelihood (1-5) | Impact (1-5) | Risk Score (L x I) | Priority |

|---|---|---|---|---|---|

| Supplier capacity | Core factory delays production during peak order period | 4 | 5 | 20 | High |

| Compliance | Product packaging for a new market requires revision after shipment booking | 3 | 5 | 15 | High |

| Logistics | Ocean freight congestion causes inbound replenishment slippage | 4 | 4 | 16 | High |

| Quality | Component defect drives return complaints after marketplace launch | 3 | 5 | 15 | High |

| Data visibility | Inventory records lag actual sell-through and reorder timing slips | 3 | 4 | 12 | Medium |

| Currency and landed cost | Input cost movement weakens planned margin on expansion SKUs | 3 | 3 | 9 | Medium |

| Single warehouse dependence | Domestic transfer bottleneck delays final availability | 2 | 4 | 8 | Medium |

| Political or trade change | Import process changes create friction in one target market | 2 | 4 | 8 | Medium |

This kind of matrix doesn't remove judgement. It improves it.

Heat maps are useful when they drive action

A recent marketplace review revealed that many businesses build risk registers that become static documents. They look thorough, but they don't influence operating behaviour. A risk heat map only matters if it changes what gets funded, audited, or redesigned.

The wrong use of a risk matrix is to document concern. The right use is to decide where management attention goes first.

For example, if a high-volume SKU relies on one supplier, one shipping pattern, and one packaging format that hasn't been localised for the destination market, that cluster should move higher than a lower-probability issue that feels dramatic but sits further from immediate revenue.

Mature operators distinguish themselves. They don't chase the loudest risk. They work the most consequential one. That discipline matters even more when expansion decisions are being made across channel, country, and assortment at the same time. A strong international retail expansion strategy for brands depends on this kind of operational ranking, because the expansion plan is only as strong as the weakest dependency inside it.

Governance matters more than templates

The framework has to live somewhere in the business. Someone owns updates. Someone challenges assumptions. Someone checks whether a previously acceptable risk has changed because volumes, markets, or product mix changed.

Without that cadence, risk assessment turns into a launch-phase exercise. That doesn't work. Expansion keeps changing the operating environment, so the assessment has to keep moving with it.

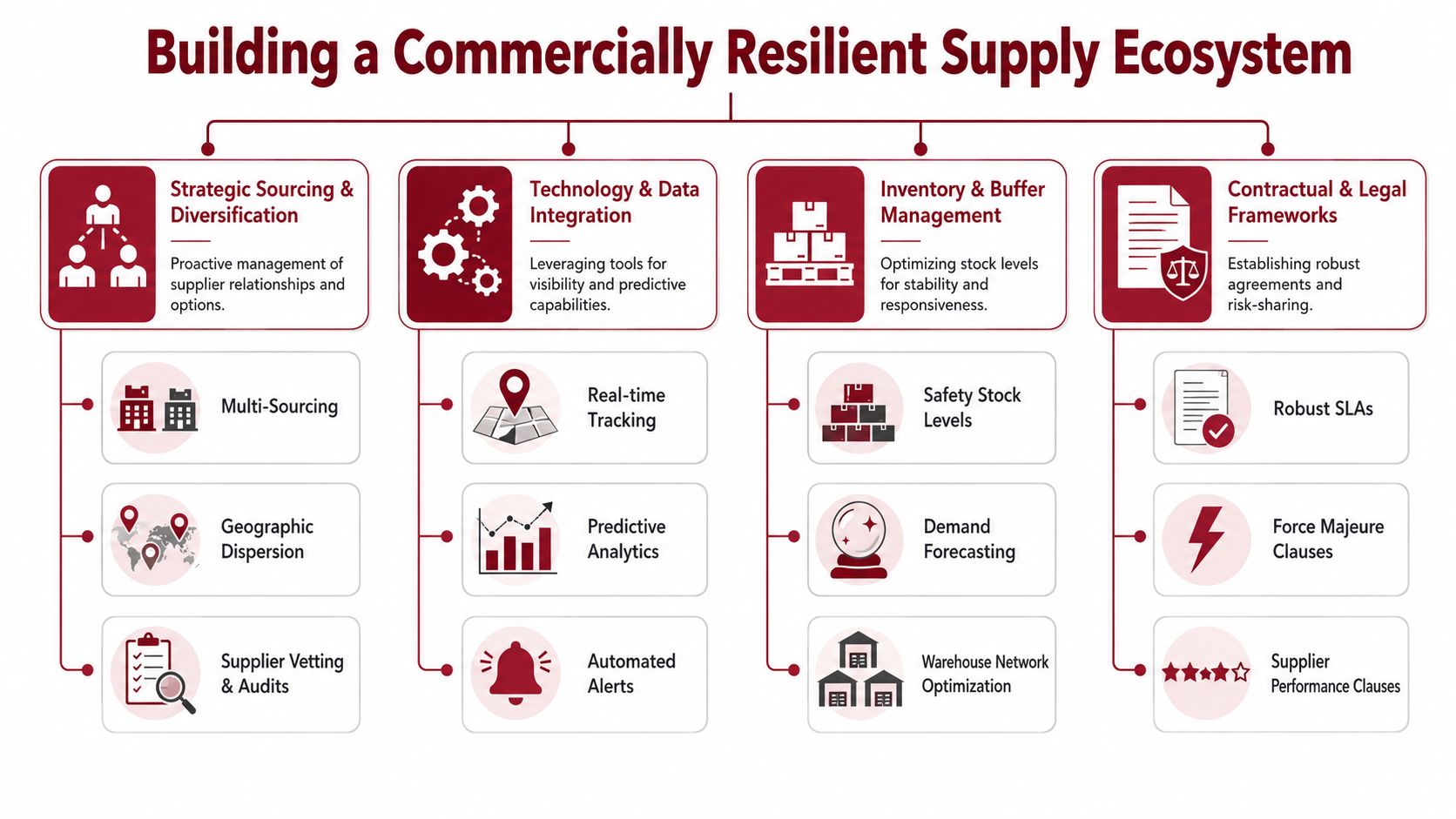

Building a Commercially Resilient Supply Ecosystem

Resilience is often discussed as though it's a defensive overhead. In reality, it behaves more like commercial infrastructure. It allows a brand to enter new markets without making panicked decisions every time a supplier slips, a lane tightens, or a compliance issue surfaces.

That shift is already visible in investment priorities. An industry analysis reports that 70% of organisations are prioritising supply chain visibility and resilience as key areas of technological investment, reflecting how risk management has moved into strategic capability, as outlined in this industry guide to supply chain risk management.

Diversification is useful, but only when it's commercially coherent

Founders often hear "dual source" and assume the answer is adding another factory. That's too blunt. A second supplier can reduce one risk while introducing three more. Different tooling standards, inconsistent finish, new quality variation, fragmented ordering economics, and more coordination burden can all erode the benefit.

What works is selective diversification.

- Protect core SKUs first: Start with the products where disruption would hurt revenue and marketplace continuity most.

- Avoid mirrored risk: A backup supplier in the same region, using the same sub-tier inputs, may create the appearance of resilience without changing the exposure.

- Align operational standards: Backup capacity only helps if quality, packaging, documentation, and lead-time expectations are already defined.

Inventory buffers should be intelligent, not emotional

When supply pressure rises, many businesses default to carrying more stock. Sometimes that's right. Often it's just expensive.

Better operators size inventory buffers around actual vulnerability. They hold protection where lead times are variable, replenishment windows are narrow, or marketplace penalties for stockouts are severe. They don't scatter excess stock across the entire catalogue.

That approach becomes especially relevant when marketplace fulfilment models create their own constraints. Inventory planning isn't isolated from channel structure. It sits alongside range architecture, distribution design, and replenishment logic, including decisions around Amazon distribution.

A resilient inventory position isn't about holding more units everywhere. It's about protecting the right units in the right places.

Monitoring needs leading indicators

Most underperforming supply models rely on lagging indicators. Late orders. Claims. Returns. Margin erosion. By the time those show up, the problem is already expensive.

A stronger operating rhythm tracks earlier signals such as:

- Supplier confirmation slippage

- Changes in defect or rework patterns

- Transit-time variability by lane

- Documentation error frequency

- Forecast deviation on expansion SKUs

- Customs clearance friction by market

These signals don't eliminate disruption. They let the business respond while options still exist.

Contracts still matter

Commercial resilience isn't only operational. It is also contractual. Service levels, quality standards, remedy paths, document requirements, and escalation expectations all need to be explicit. Informal supplier goodwill can carry a business to a point. It won't carry international scale.

The brands that expand with more control usually build a supply ecosystem that is visible, monitored, and commercially disciplined. Not perfect. Just less fragile.

The International Expansion Stress Test in Practice

What becomes visible during international expansion is that a supply chain designed for Australia often carries assumptions that don't travel well. Lead times feel longer because they are. Compliance questions get more granular. Last-mile performance stops being a generic logistics matter and starts affecting review quality, return rates, and reorder confidence inside the marketplace itself.

For Australian brands, the freight structure alone creates a distinct exposure. The Department of Infrastructure, Transport, Regional Development, Communications and the Arts reports that 99% of Australia's international trade by volume moves by sea, which means maritime disruption sits at the centre of the risk model rather than at the edge, as discussed in this McKinsey approach to supply chain risk management.

Small differences become structural under distance

A hardware or home-improvement product that moves cleanly through Australian retail may hit friction when launched into the US or UK for reasons that look minor on paper.

Consider the types of issues that surface:

- Packaging language and warnings: A product may need revised labelling, warnings, or supporting documentation before it can move confidently into a new region.

- Landed cost distortion: Duty treatment, brokerage, handling, and local storage can reshape SKU economics after the initial range plan looked sound.

- Marketplace fulfilment mismatch: The product's dimensions, fragility, or storage profile may behave differently inside overseas warehouse and parcel networks.

- After-sales strain: Replacement parts, warranty handling, and return routing become harder once the customer sits in another country.

None of those problems are dramatic in isolation. Together, they can make a promising expansion commercially unstable.

The real test is ecosystem fit

Across multiple marketplace ecosystems, one pattern keeps appearing. Brands often assume that a successful domestic supply model can be easily extended outward. It usually can't. The supply chain has to be requalified against the target ecosystem.

That means testing questions such as:

| Expansion variable | What needs to be tested |

|---|---|

| Ocean freight lane | Whether one lane disruption could affect several priority SKUs at once |

| Port and customs flow | Whether delays at arrival points create stock gaps that local safety stock can't cover |

| Regional compliance | Whether product, packaging, and claims align with the destination market |

| Warehouse network | Whether storage location supports the expected service level and return path |

| Local customer expectation | Whether the current support model can absorb delays, defects, or replacements |

International expansion is rarely derailed by one catastrophic error. It is weakened by a series of assumptions that were never retested for a different market.

Why some brands hold their position and others wobble

The stronger operators don't just ask whether the product will sell. They ask whether the whole operating model can survive the distance between order placement and end-customer experience.

That includes lane choice, customs readiness, inventory posture, carton design, service policy, and local market adaptation. In other words, expansion is an ecosystem transition, not a listing exercise.

When that distinction is ignored, the marketplace becomes a stress amplifier. When it's understood, the same marketplace can become a disciplined growth engine.

Turning Supply Chain Resilience into a Commercial Asset

The brands that scale well internationally usually stop viewing supply chain risk management as a defensive function. They use it as a commercial filter for growth decisions.

That changes behaviour in practical ways. SKU selection gets sharper because the team understands which products travel well operationally. Market entry gets more disciplined because compliance, freight, and replenishment are assessed before demand is assumed. Margin planning becomes more honest because the business isn't pretending emergency fixes won't happen.

Reliability creates competitive space

In crowded marketplaces, product quality alone rarely protects a brand. Buyers respond to the full experience. Availability, delivery reliability, replacement handling, and consistency all shape whether a brand earns trust or creates hesitation.

A resilient supply model supports that trust in ways that are easy to underestimate:

- It protects margin by reducing expensive reactive logistics and remediation.

- It protects ranking stability by reducing out-of-stock periods and service failures.

- It protects brand perception because customers experience consistency, not operational noise.

- It protects expansion confidence because management can add channels and regions without losing control.

One pattern we continue seeing is that commercially mature brands treat operational resilience as part of brand architecture. They know that a premium product with weak supply control won't hold premium positioning for long.

Strong products still need strong operating systems

Great products don't automatically become strong international brands. They become strong brands when the surrounding ecosystem is coherent enough to support repeatable delivery, stable economics, and local market confidence.

That's why supply chain risk management deserves a wider commercial lens. It isn't just there to prevent disaster. It gives leadership a clearer view of which growth paths are durable, which margins are real, and which operational assumptions need rebuilding before expansion goes further.

For founders and commercial teams planning entry into complex marketplace environments, that's the difference between surface-level growth and scalable growth.

If you're assessing whether your current supply model can support international marketplace expansion without margin erosion, TPR Brands works with established product brands to build commercially cohesive growth across Australia, the US, Canada, and the UK. The focus isn't on generic marketplace activity. It's on creating the operational and ecosystem structure that lets strong products scale with control.