Most international growth advice assumes demand will travel. In reality, international retail expansion strategy for brands is not about demand—it’s about execution.

Strong products fail globally when market selection, compliance, channel design, and pricing are not built for the target market.

That thinking burns capital.

A product can win at home and still stall abroad because international retail expansion strategy for brands isn’t just about demand generation. It’s a discipline that sits at the intersection of market selection, compliance, channel design, pricing, freight, inventory, and local commercial judgement. Founders often discover this too late, usually after the first distributor underperforms, the first retailer asks for packaging changes nobody budgeted for, or the first shipment gets delayed because the product file wasn’t built for that market.

The hard truth is simple. Great products do not automatically become great international brands. They become international brands when the business can translate product-market fit into market-specific execution.

That translation is where most brands break. A hardware product that sells cleanly in Australia may need different certifications in the US, Canada, or UK. A household product that performs well on Amazon may need a different margin structure for retail. A brand with strong founder-led momentum may lose trust fast if the local customer experience feels imported rather than built for the market.

Practical rule: Global growth is rarely limited by ambition. It’s limited by operational precision.

The brands that expand well don’t chase geography first. They build a system. They choose the right market, enter with a controlled model, localize properly, protect margin, and use partners where local knowledge changes the economics. That’s what works. Everything else is usually expensive education.

An international retail expansion strategy for brands is a structured approach to entering new markets by aligning product fit, compliance, channel design, pricing, and operations to local conditions.

Why Great Products Fail in International Retail Expansion

Founders rarely lose overseas because the product is weak. They lose because they assume a domestic operating model will survive contact with a new market.

That assumption is expensive.

A strong home market creates false confidence, especially in hardware and consumer products. The product works. Reviews are strong. Retailers or distributors show interest. Supply looks under control. It starts to feel like expansion is mainly a sales problem. In practice, global growth breaks where commercial model, compliance, channel structure, and operations meet.

A product that sells well in Australia or the US can still fail abroad for ordinary reasons. Packaging misses a retailer requirement. Product files are incomplete for local approvals. Margin disappears once freight, duties, distributor terms, and promotional support are added. A channel partner wins the account but cannot drive sell-through. The team celebrates shipment into market, even though the market has not accepted the brand.

For operator-led teams, the pattern is familiar. Demand is rarely the first thing to fail.

What usually breaks first sits underneath the launch story:

- Commercial logic falls apart when home-market margin assumptions do not survive local channel economics.

- Operational design falls apart when replenishment, returns, lead times, and service levels were never built for that market.

- Compliance readiness falls apart when localization is treated as a labelling exercise instead of a product, documentation, and market access exercise.

- Customer fit falls apart when the brand imports its home-market positioning into a market that buys for different reasons, through different channels, at different price points.

Starbucks in Australia is a well-known example of a business misreading local buying behavior and market expectations. The lesson is not that every brand should pursue acquisition or extreme localization. The lesson is simpler. Product quality and brand recognition do not protect you from local commercial reality. In hardware and consumer categories, that reality shows up in specification choices, certification pathways, fixture requirements, warranty expectations, and who explains the product at the shelf.

A market is not proven because inventory arrived. It is proven when customers buy, retailers reorder, and the margin still justifies the effort.

The brands that expand well treat each new country as a fresh business model with linked decisions across market sizing, compliance, supply chain, and channel economics. Speed matters. Control matters. Profitability matters more.

How to Choose the Right Market for International Expansion

The biggest market is often the most expensive place to learn.

Founders and boards still default to population, GDP, and category size because those numbers look objective. For hardware and consumer product brands, they are only the starting point. A market can be large, visible, and strategically wrong if the compliance burden is heavy, the channel structure strips margin, or the product needs more adaptation than the P&L can carry.

Build a scoring model that reflects execution reality

A weighted market scorecard forces discipline. It also exposes where a market looks attractive in theory but weak in practice.

The right model measures demand alongside the frictions that determine whether demand can be served profitably. For operator-led brands, especially in hardware, that means looking at product fit, regulatory path, channel economics, fulfilment design, and the amount of local adaptation required to earn repeat purchases.

| Factor | What to assess | What founders often miss |

|---|---|---|

| Category fit | Does the market already buy products like yours for the same use case? | Assuming a familiar category behaves the same way everywhere |

| Regulatory friction | How hard is certification, labelling, and customs readiness? | Treating compliance as something to fix after launch |

| Channel maturity | Which channels can actually move your product at the right price point? | Confusing channel access with channel productivity |

| Competitive density | How crowded is the segment, and how entrenched are incumbents? | Entering a large market without a clear wedge |

| Operational viability | Can you service lead times, returns, and inventory flow profitably? | Ignoring replenishment economics and reverse logistics |

| Brand translatability | Will the positioning make sense locally without forcing a full reset? | Assuming translation is enough |

Rank markets by attractive demand adjusted for friction. That is a better filter than ranking them by headline size or founder enthusiasm.

Australia shows how mature markets reward precision

Australia is a useful example because it often looks easier than it is. Language overlap lowers perceived risk, but mature retail markets are usually less forgiving, not more. Buyers already have alternatives. Retailers understand their negotiating power. Service expectations are high, and a weak local offer gets exposed quickly.

According to Statista’s retail market overview, Australia’s retail sector reached AUD 450 billion in annual sales as of 2024, Costco reached 2.5 million members by 2023, and brands adapting pricing and channels saw 35% higher retention. The lesson is not that every brand should rush into Australia. The lesson is that mature markets reward brands that localise the commercial model, not just the website.

For some brands, that starts with marketplace validation before broader retail rollout. Teams assessing that route should understand the local mechanics of assortment, margin, and channel conflict before committing inventory. This guide on how overseas brands can sell on Amazon Australia is useful if Amazon is part of the entry mix.

This video gives useful context on how operators think about market entry trade-offs:

The best first market is usually narrower than the board expects

Early expansion works better when the market gives you room to learn without breaking the model.

A strong first-entry market usually has a clear use case, manageable compliance work, one or two viable channels, and enough demand to validate repeatability before you add complexity. That can mean choosing a market with lower theoretical upside but better operating conditions. I would take a market where the product can be sold, supported, and replenished properly over a larger market that forces deep discounting, retailer dependence, and expensive compliance rework.

Use that lens when pressure builds to go after the biggest opportunity on paper. In international expansion, the first win should buy learning, proof, and margin.

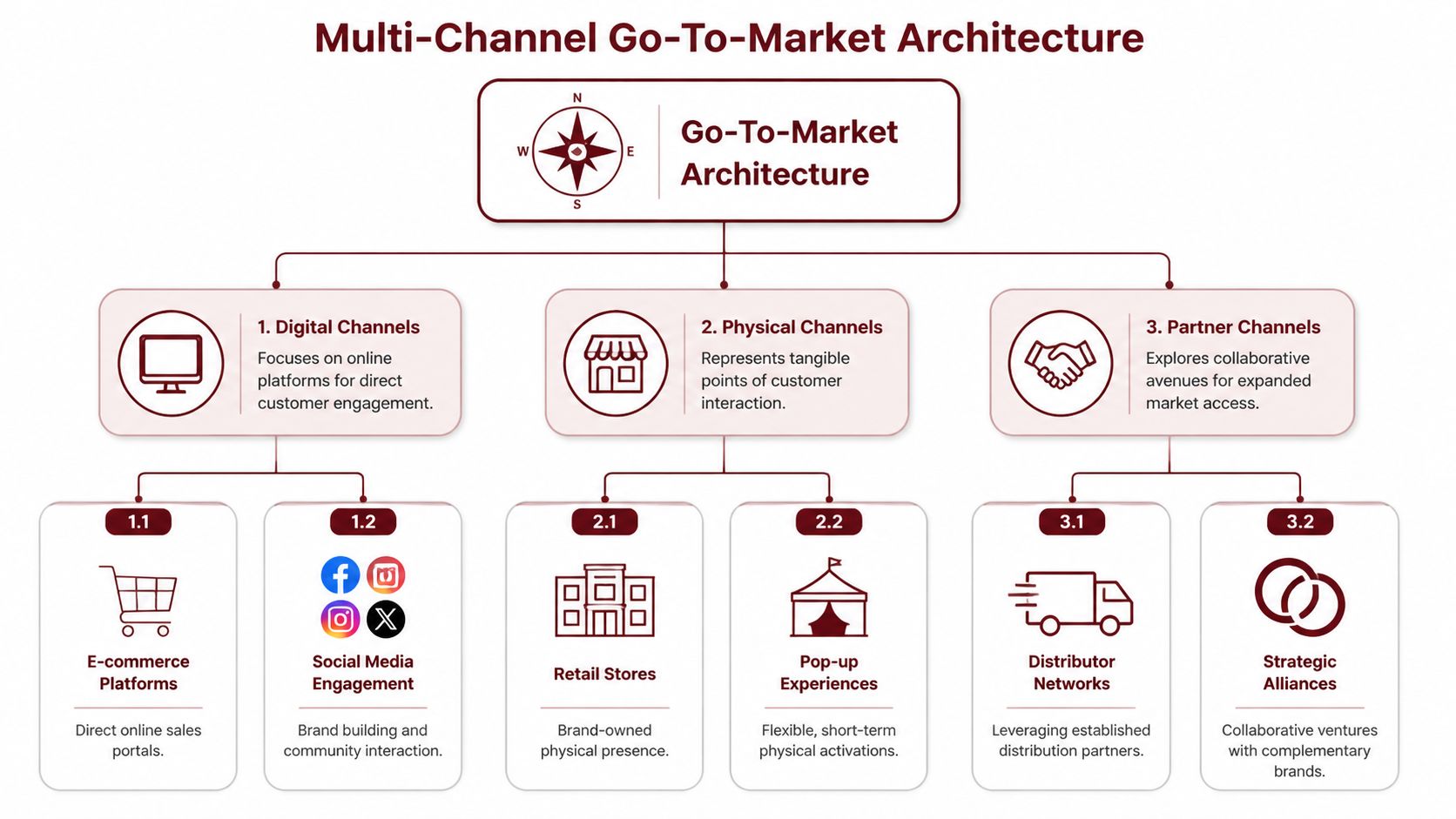

Building a Multi-Channel Go-To-Market Strategy

Most brands don’t have a market-entry problem. They have a channel-design problem.

A lot of expansion plans still come down to a false binary. Go all in on Amazon, or build D2C first. Push retail immediately, or stay online until awareness grows. That framing is too narrow. Strong international execution usually comes from channel architecture, where each route to market plays a different job in the system.

Each channel should have a role

Think of channels by function, not by fashion.

D2C is where you control brand education, gather direct customer signals, and test bundles, claims, and positioning. It’s useful early because it exposes what local customers respond to.

Marketplaces are effective for capturing existing demand and accelerating discoverability, especially when buyers already shop by category rather than by brand. But marketplaces can compress pricing discipline if the catalogue architecture is weak or if channel conflict starts early. Brands exploring this path should think carefully about how marketplace presence fits broader expansion strategy, especially in markets like Australia where channel sequencing matters, as discussed in this guide to selling on Amazon Australia from overseas.

Retail builds legitimacy and physical trial. For some products, especially in hardware, household, and home improvement, shelf presence still shapes trust in a way paid media can’t replicate.

Distributors and commercial partners extend reach when local relationships, compliance processes, or account access would otherwise take too long to build internally.

What smart sequencing looks like

The mistake isn’t using one channel. The mistake is expecting one channel to do every job.

A cleaner sequence often looks like this:

-

Controlled digital entry

Launch where the brand can test messaging, service levels, and demand concentration without overcommitting inventory. -

Marketplace capture

Add marketplace presence where there is already high-intent category traffic, but keep assortment and pricing disciplined. -

Selective retail proof

Enter a limited set of retail doors where the product can be merchandised properly and where reorder behaviour can be observed. -

Partner-led distribution scale

Expand through operators who can handle local account relationships and execution without forcing margin-destructive shortcuts.

The trade-off founders need to face

More channels don’t automatically create more strength. They create more complexity.

| Channel | Main upside | Main risk |

|---|---|---|

| D2C | Brand control and direct insight | Slower trust-building in unfamiliar markets |

| Marketplace | Fast demand capture | Price pressure and weak brand differentiation |

| Retail | Credibility and physical presence | Margin compression and listing complexity |

| Distributor | Local reach and operational leverage | Reduced control if partner incentives are misaligned |

A founder should ask one question before adding any channel: What capability does this channel add that we do not already have? If the answer is vague, the channel is probably a distraction.

Your channel mix should widen reach without fragmenting accountability.

The strongest brands don’t argue about whether D2C or retail is better. They design a system where digital builds signal, marketplaces catch demand, retail adds trust, and partners accelerate what the internal team can’t yet do efficiently.

Product Localization and Compliance for Global Markets

International expansion usually breaks at the product layer before it breaks in marketing.

For hardware and consumer product brands, localization is an operating decision. It affects certification cost, packaging runs, channel eligibility, return rates, installation success, and retailer confidence. A product can be popular at home and still be wrong for the target market in ways that are expensive to fix later.

Translation is the easy part. The harder work is confirming that the product is fit for sale, fit for use, and fit for the channel.

A founder entering a new market should test the product on three fronts:

-

Functional fit

Confirm the product works the way the market expects. Check voltage, plug type, dimensions, installation norms, refill systems, climate tolerance, and pack size. -

Retail fit

Confirm the product can be ranged. Check shelf dimensions, barcode format, warning labels, carton markings, display requirements, and any retailer-specific packaging rules. -

Trust fit

Confirm the brand looks credible after purchase, not just before it. Review claims, manuals, care instructions, warranty terms, spare parts access, and customer support language.

Hardware brands face specific difficulties. A minor mismatch can stall a launch. A power spec that needs retesting. A warning statement that fails local review. A carton size that does not fit the retailer’s planogram. None of these issues look strategic in isolation. Together they decide whether the market opens cleanly or turns into months of rework.

Marketplace entry does not reduce the burden. It often exposes it faster. Listings, packaging, manuals, and customer messages need to match, especially when the product sits in categories with safety, performance, or installation implications. Brands using Amazon as part of entry should treat compliance and listing quality as one workstream, not two separate tasks. That is why serious operators build a broader Amazon selling strategy for international market entry instead of treating the channel as a simple upload exercise.

A practical compliance audit

Compliance should sit inside the commercial launch plan because every delay hits revenue, margin, or both.

A useful audit covers:

-

Product standards

Check whether current certifications are accepted, partly accepted, or unusable in the target market. Do this at SKU level, not brand level. -

Labelling and documentation

Review warnings, user instructions, carton labels, country-of-origin marking, language requirements, and any retailer submission standards. -

Claims review

Strip back any packaging, listing, or advertising claim that cannot be supported locally or that crosses into a regulated category. -

Import readiness

Confirm tariff codes, customs paperwork, restricted material exposure, battery handling rules, and any testing required before goods clear. -

Returns and warranty design

Set the policy, parts flow, and service process before launch. A warranty promise without a local process becomes a margin problem very quickly.

Brands usually budget for freight, samples, and launch spend. They miss the cost of rework.

That cost shows up in destroyed packaging, delayed purchase orders, repeated testing, relabelled stock, missed seasonal windows, and channel frustration. In international retail, compliance errors are rarely isolated legal issues. They become commercial losses.

What good operators do differently

They build a market-specific product file before serious selling starts.

That file should include approved artwork, certification status, test reports, local instructions, warranty terms, packaging specifications, import notes, and channel constraints by SKU. Sales uses it to answer buyer questions consistently. Operations uses it to ship the right stock. Marketing uses it to keep claims aligned with what the product can legally and practically support.

Without that file, every team creates its own version of readiness. That is how brands end up selling products that are not fully cleared, promising features that do not translate cleanly, or accepting retailer terms they cannot operationally support.

The payoff is speed with fewer surprises. Buyers trust brands that arrive prepared, and prepared brands make better decisions about where to adapt the product, where to hold the line, and where a market is not worth entering yet.

Pricing Strategy for International Retail Expansion

Strong demand is one of the easiest ways to misread an export market.

I have seen hardware and consumer product brands celebrate early purchase orders, then discover six months later that every unit sold is funding channel margin, freight variance, launch rebates, and after-sales support they never priced in. The result is familiar. Revenue looks healthy. Cash conversion does not.

An international retail expansion strategy for brands needs a commercial model before it needs a forecast. If you cannot explain where profit is created by SKU, by channel, and by market, you are still testing demand, not building a business.

Cost-plus pricing misses how international retail actually works

Factory cost is only the starting point. For physical products, especially hardware, the full pricing discussion starts once you map the full cost-to-serve in each market.

That means landed cost, duties, local warehousing, retailer margin expectations, promotional funding, reverse logistics, warranty exposure, and payment terms. Add channel-specific setup costs and the picture changes again. A direct-to-consumer price can absorb one economics profile. A distributor-led retail model often needs a very different one.

Use four inputs to set price with discipline:

| Pricing input | Why it matters |

|---|---|

| Landed cost | This sets the real floor after freight, duties, and import charges |

| Channel structure | A distributor, retailer, marketplace, and DTC channel each remove margin differently |

| Local value perception | Customers in some markets pay more for reliability, service, or brand proof than others |

| Brand positioning | Price signals whether the product sits in premium, mass, or promotional territory |

For operator-led teams, the job is not choosing one global price and adjusting for FX. The job is deciding what role each market plays, then building a price ladder that protects margin and supports that role.

Discounting usually covers a weaker problem

Price cuts are often used to solve issues that pricing did not create. Weak merchandising. Low brand recognition. Poor in-store staff training. An underpowered distributor. A range architecture that gives the buyer no clear good-better-best story.

Cutting price may buy short-term sell-through, but it can also train the market to wait, compress retailer confidence, and make future margin recovery expensive. That is a bad trade if the brand needs long-term shelf stability.

Chemist Warehouse is a useful reminder that international growth is often built through commercial structure, not pricing aggression. The brand expanded into the United States by acquiring a majority stake in Walmart’s pharmacy business, and its revenue surpassed AUD 5 billion in FY2023, according to Chain Store Age’s coverage of international retail brands entering the US. The lesson for founders is narrower and more useful. Expansion structure affects margin as much as shelf price does.

Model contribution before you model volume

A forecast without contribution logic is just optimism in spreadsheet form.

Before launch, the commercial model should answer a few hard questions:

- What gross margin is required by channel to justify the operating load?

- Which SKUs win placement, and which SKUs carry the business?

- How much launch funding can the market absorb before payback breaks?

- What price floor protects the brand if a retail partner pushes for promotions early?

- How do returns, warranty claims, and local service obligations change contribution margin?

- What fulfilment setup is needed to hit service levels without destroying unit economics? For many brands, that means choosing a fulfilment model that matches channel and market complexity.

For consumer products, this usually leads to a clear trade-off. Faster market entry often means giving up margin through distributor layers, launch support, or retail terms. More control can improve unit economics, but it raises execution load and working capital pressure.

Commercial discipline: If the model only works when demand is strong, discounting stays shallow, returns stay low, and the partner performs well, the model is too fragile for international scale.

The better approach is restraint. Accept lower early volume if that is what it takes to preserve price integrity, keep contribution positive, and learn what the market will support. Global growth rarely fails because a brand priced too carefully. It fails because the business accepted volume that never had enough margin behind it.

Supply Chain and Partnerships in Global Expansion

A founder signs a new overseas partner and feels momentum immediately. The partner has retailer relationships, local language capability, and an ambitious revenue target. On paper, it looks solved.

Then the first real operating month starts.

Forecasts are vague. Packaging approvals drag. The partner wants stock depth before they’ve proven sell-through. Customer service expectations aren’t aligned. Retail conversations move faster than compliance work. Nobody owns the inventory risk clearly. The partnership didn’t fail because the opportunity was bad. It failed because the operating backbone was never built.

What to vet before signing anyone

A partner should be assessed on execution, not enthusiasm.

Here are the questions that matter most:

-

Operational depth

Can they manage onboarding, forecasting, replenishment, and account follow-up, or are they mainly a sales front? -

Category credibility

Have they sold adjacent products that require similar education, service levels, or compliance handling? -

Brand fit

Do they understand how to grow the brand without turning it into a discount commodity? -

Reporting discipline

Will they provide sell-through visibility, not just purchase orders? -

Financial behaviour

Do their terms, stock expectations, and launch requests indicate a sustainable relationship?

Supply chain choices shape partner quality

The wrong fulfilment model can make a good partner look weak. A decent operator can’t compensate forever for poor inventory positioning or unreliable service windows.

That matters even more in categories with technical or regulatory complexity. For Australian hardware brands entering the US, Canada, or UK, clashes between AS/NZS standards and CPSC, CSA, or UKCA requirements can create delays, and operator-led models with pre-built compliance can cut entry time by 40%, according to Endear’s discussion of retail internationalisation. In practical terms, compliance readiness and supply chain design shouldn’t be separated. If one slips, the other pays for it.

Brands also need to decide how they want the market served:

| Operating model | Best use case | Main watch-out |

|---|---|---|

| Cross-border fulfilment | Early demand testing | Service levels can be inconsistent |

| Local 3PL | Faster delivery and cleaner returns handling | Requires stronger forecasting discipline |

| Partner-held stock | Useful when partner incentives are aligned | Can create pressure for premature volume |

| Hybrid model | Good for phased entry | More complex accountability |

For teams evaluating local service structure, the logic behind fulfilment strategy in Australia and adjacent markets often applies more broadly. The fulfilment model isn’t a back-office detail. It’s part of the offer.

A weak partner with inventory will create noise. A strong partner without operational support will create frustration. You need both capability and infrastructure.

The right partnership reduces learning curve, not just sales effort. If a partner can’t help the brand manage compliance, replenishment, account realities, and channel discipline, they’re not really reducing risk. They’re moving it around.

How to Launch and Scale in International Markets

International launches fail when brands mistake activity for proof. More channels, more doors, and more inventory can make the business look like it has traction, while hiding an essential question. Can this product win in this market at an acceptable margin once the initial push is over?

For hardware and consumer product brands, that question gets answered in operations as much as in sales. A market can show healthy early orders and still be the wrong bet if returns are messy, replenishment is slow, packaging creates confusion, or channel margins collapse after the first promotion. Early expansion needs to be designed to expose those weaknesses fast.

Start with a pilot built for diagnosis

A pilot should isolate cause and effect. If you launch too broadly, you lose that. You cannot tell whether weak performance came from poor retail execution, the wrong price architecture, a compliance-related delay, or a product issue that only shows up in local use.

A narrower pilot gives you cleaner readouts. For some brands that means a small retail cluster. For others it means one marketplace, one specialist wholesale account, and one local operating partner. The structure matters less than the discipline behind it. Each channel in the test should have a clear job, and each job should generate evidence you can use.

The Across Magazine analysis of retail expansion mistakes argues for starting with a limited store pilot and allowing enough time to gather operating data before scaling. That is the right instinct. Founders usually underestimate how long it takes to see reorder behaviour, service issues, staff adoption problems, and the true cost of supporting the market after launch week.

Measure what predicts scale

Early-stage reporting should stay tight. A bloated KPI pack creates noise and gives weak channels too much room to hide.

Track indicators that answer four commercial questions.

-

Is demand real?

Look at sell-through after the launch window, not just initial fill or first-month revenue. -

Will the channel reorder?

Repeat purchase behaviour from retailers, distributors, or end customers tells you more than launch enthusiasm. -

Is the product holding up in-market?

Returns, warranty claims, complaints, and support tickets often reveal localisation gaps before revenue does. -

Are the economics improving or deteriorating?

Measure contribution by channel after freight, handling, trade spend, markdown support, and partner fees.

I also look closely at execution lag. If stock lands late, listings go live slowly, or retail staff are not trained in time, demand data becomes unreliable because the offer was never properly available.

Build a risk register before the first shipment

This does not need a corporate template. It needs named risks, an owner, and a response plan.

A usable launch risk register usually covers:

-

Regulatory and claim risk

Missing documents, incorrect labelling, unsupported product claims, or approvals that slip. -

Inventory risk

Stock loaded into the wrong node, poor forecast accuracy, or reorder settings that force either stock-outs or excess ageing inventory. -

Partner execution risk

Slow reporting, weak account follow-up, poor merchandising discipline, or incentives that push the wrong behaviour. -

Price and channel risk

Early discounting, grey-market leakage, marketplace undercutting, or conflict between direct and wholesale accounts. -

Demand quality risk

Strong opening interest with weak conversion, low attachment, or no meaningful reorder signal.

Strong operators treat launch as a test period with spending controls, review gates, and predefined scale criteria. If those criteria are not met, the answer is not to push harder everywhere. It is to identify what failed, fix the system, and decide whether the market still deserves more capital.

Scale should follow evidence. In international retail, that is how brands keep control while they grow.

Conclusion A Tactical Checklist for Controlled Global Growth

International growth works when founders stop treating it as export momentum and start treating it as system design.

The durable version of expansion is deliberate. It selects the right market, not the biggest headline market. It builds channel architecture instead of chasing isolated wins. It localizes product and compliance before demand is forced. It protects margin through disciplined commercial design. It backs all of that with operational infrastructure and partner accountability.

If you want a blunt readiness test, use this checklist.

Expansion readiness checklist

-

Market choice

Have you chosen the market based on fit, friction, and serviceability rather than size alone? -

Customer relevance

Can you explain why local buyers will choose your product over incumbent options? -

Channel logic

Does each channel in the plan have a distinct job, or are you duplicating effort? -

Product readiness

Have you adapted specifications, packaging, and documentation for local reality? -

Compliance file

Is there a complete market-specific product file ready before major selling starts? -

Commercial model

Do you know landed cost, required gross margin, and acceptable promotional boundaries by channel? -

Partner diligence

Have you tested prospective partners for operational capability, not just sales claims? -

Supply chain design

Is your fulfilment and replenishment model matched to the service promise you’re making? -

Pilot structure

Are you entering with a test that can generate clear learning rather than broad but muddy results? -

Decision rules

Have you defined what would trigger scale, pause, or market reset?

Founders don’t need more generic encouragement to “go global”. They need a stricter operating lens. Expansion rewards businesses that can combine ambition with control. That’s the difference between international activity and international growth.

A disciplined international retail expansion strategy for brands turns global growth from a risk into a repeatable system.

If you’re an established brand looking at controlled expansion into new retail channels or overseas markets, TPR Brands works with teams that want structure before scale. The focus is on proven products, strong positioning, and practical routes into new regions without losing brand value in the process.