A product can lead its home category, win repeat customers, and still enter the wrong marketplace ecosystem at exactly the wrong time.

That's the gap many expansion plans miss. Founders often ask whether a new market is large enough, visible enough, or strategically attractive enough. The harder question is whether the market is commercially workable for their brand once fulfilment, localisation, compliance, pricing architecture, retailer behaviour, and marketplace norms start pressing on margin and customer trust.

That's where commercial due diligence matters. Not as a corporate formality. Not as a spreadsheet exercise bolted on late. As a discipline for testing whether a market entry is viable in the world, under the conditions your team will encounter.

The Question Every Scaling Brand Must Answer

The most dangerous assumption in expansion is simple. If a product performs well in one market, it should perform well in the next.

In practice, that assumption breaks down quickly. A hardware brand that works through Bunnings, Mitre 10, or an established domestic reseller network may struggle when the next market expects different delivery speeds, different product content, different support standards, and very different price visibility across channels. The product hasn't changed. The commercial environment has.

One pattern we continue seeing is that domestic traction creates a false sense of transferability. Teams read strong sell-through, healthy repeat demand, and stable channel relationships as proof that the brand is ready for another region. Sometimes it is. Sometimes those same strengths are tightly linked to conditions that don't travel well.

The real question isn't whether expansion is possible

Almost any brand can make a market entry look possible on paper. A listing can go live. A distributor can be appointed. A retailer can be approached. Inventory can be shipped.

The more useful question is this: will the next market support the brand's economics, positioning, and operating model without eroding what made the business strong in the first place?

That's why commercial due diligence has become more than a transaction term. It's a way of pressure-testing commercial reality before a brand exposes itself to avoidable risk.

One industry source states that almost 60% of deals fail because poor due diligence misses critical issues, a reminder that teams can't rely on historical performance alone when they move into new channels or regions (commercial due diligence overview).

Strong domestic performance can hide fragile assumptions. Expansion exposes them.

What experienced operators look for

Founders usually begin with upside. Operators begin with failure points.

That means asking uncomfortable questions early:

- Demand durability: Are customers in the target market likely to reorder, replace, or recommend at the same rate?

- Channel fit: Does the product belong in marketplaces, trade distribution, specialist retail, or a hybrid structure?

- Margin resilience: What happens when fees, returns, localisation costs, and promotional pressure hit the model?

- Brand translation: Does the current value proposition still make sense once claims, packaging, and use cases are viewed through another market's expectations?

Commercial due diligence sits inside those questions. It doesn't kill growth. It clarifies whether growth is strong enough to deserve capital, inventory, management attention, and brand exposure.

Redefining Commercial Due Diligence for Brands

Founders often hear the phrase and think of an M&A team reviewing a target business before a deal closes. That definition is too narrow for modern product brands.

For an operator, commercial due diligence is the process of testing whether an expansion thesis is commercially sound before the brand commits itself to a new ecosystem. It brings together channel economics, customer behaviour, competitive positioning, operational readiness, and localisation friction. It asks whether the business can work, not whether the idea sounds persuasive in a boardroom.

Why the old definition no longer holds

In Australia, 43.2% of M&A professionals expected diligence requirements to increase over the following year, reflecting deeper screening of market demand, customer durability, and competitive position before capital is committed (Australian due diligence trend data).

That shift matters beyond transactions. It reflects a broader commercial reality. Financial performance on its own doesn't tell you whether a brand can survive entry into a new channel structure or a new country.

A business can look healthy in headline terms and still carry hidden weaknesses:

| Commercial question | Traditional review often checks | Brand-focused CDD should check |

|---|---|---|

| Revenue | Historical sales performance | Whether revenue is durable in a new channel mix |

| Competition | Category presence | How the ecosystem is already positioned and defended |

| Expansion | Topline potential | Whether margin, fulfilment, and trust can survive localisation |

| Operations | Current capability | Whether the team can execute without fragmenting the brand |

What this looks like in practice

For hardware, home improvement, household, and consumer product brands, due diligence becomes an audit of the go-to-market thesis itself.

That means examining whether marketplace fee structures damage unit economics, whether fulfilment expectations force inventory placement changes, whether product content needs rewriting, and whether the customer journey still supports confidence at the point of purchase. Across multiple marketplace ecosystems, the deciding issue is rarely product quality alone. It's whether the surrounding system helps the product convert, travel, arrive, and be trusted.

One issue we repeatedly observe is that teams underestimate ecosystem adaptation because they're still thinking in catalogue logic. They assume a strong range, proven packaging, and domestic retailer acceptance will carry the next stage. In reality, expansion is an ecosystem transition.

For brands working through that transition, a stronger marketplace ecosystem strategy usually starts with diligence, not launch mechanics.

A market can be attractive and still be wrong for your current operating model.

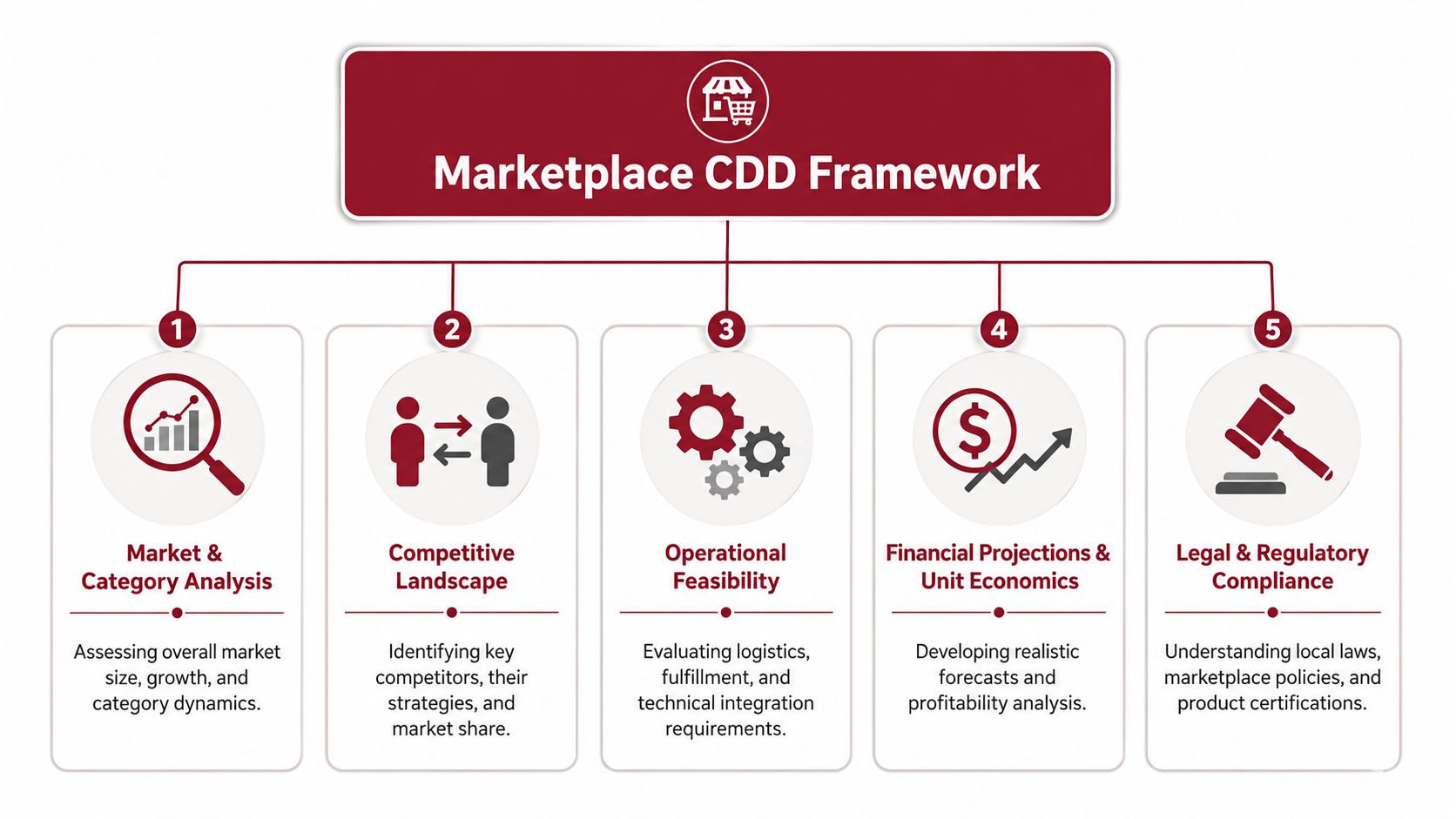

Core Components of a Marketplace CDD Framework

A useful framework for marketplace expansion doesn't begin with optimism. It begins with exposure. Where could the commercial case break? Which assumptions are carrying too much weight? Which parts of the model only work if conditions stay unusually favourable?

Market and category reality

A category can be active without being attractive. Operators look beyond broad demand and ask how the category behaves inside the target ecosystem.

That includes:

- Category maturity: Is the market already dominated by entrenched incumbents, price-led private label, or platform-native sellers?

- Search and discovery behaviour: Are customers browsing broadly, shopping by spec, or filtering by delivery confidence and review depth?

- Replacement logic: Is the product bought on urgency, planned improvement, professional recommendation, or seasonal need?

A large market with weak entry conditions often matters less than a narrower market with better structural fit.

Competitive position and ecosystem shape

Competitor analysis isn't just a list of rival brands. It's an examination of who already owns trust, speed, visibility, and pricing power.

One pattern we continue seeing is that brands underestimate indirect competition. A premium storage brand may think it's competing with adjacent premium organisers, while customers on a marketplace compare it against lower-priced alternatives, imported substitutes, and “good enough” bundles that solve the same job.

This is where ecosystem reading matters. If customer confidence flows through fulfilment badges, installer familiarity, retail credibility, or strong review density, then the competitive moat may sit outside the product itself.

Revenue quality and forecast reliability

At this stage, many teams move from theory into evidence. CDD checklists commonly stress customer concentration, churn, and segment-level revenue mix because they help create a quantified vulnerability map linking retention, pricing power, and channel dependency to forecast reliability (revenue quality in commercial due diligence).

That principle applies directly to marketplace expansion. If a brand's domestic performance is concentrated in a few key accounts, one trusted retail environment, or one customer segment, the next market may expose how narrow the revenue base really is.

A disciplined review asks:

- Customer concentration: Is performance anchored by a handful of accounts or buyer types?

- Channel concentration: Would one marketplace or one retail partner carry too much of the expansion case?

- Segment mix: Which products or variants generate margin, and which merely create volume?

- Retention quality: Do buyers reorder because the brand is strong, or because the current channel is convenient?

Operator test: If one large customer, one key SKU group, or one dominant channel disappeared, would the forecast still hold?

Unit economics and operating feasibility

Promising categories often fail scrutiny. A market may support demand but not acceptable economics.

Review the model through the full operating chain:

Landed cost integrity

Include freight, storage, duties where relevant, marketplace fees, compliance adjustments, and returns handling.Fulfilment confidence

Delivery speed, damage risk, oversize handling, and stock placement all affect conversion and review quality.Support burden

Hardware and improvement products often need clearer pre-purchase information and stronger post-purchase support than general consumer goods.Documentation readiness

Expansion often slows down on product files, declarations, manuals, certifications, testing records, and claim substantiation. Strong compliance documentation support is often a commercial enabler, not just a legal safeguard.

Localisation and regulatory fit

The final pillar is often treated too lightly. Product adaptation isn't cosmetic when claims, instructions, standards, use cases, and retailer expectations differ by market.

A brand can enter with the same product and still need a different commercial presentation. The copy may need to become more technical. The imagery may need to show local use environments. The pack may need to communicate compatibility, safety, or installation steps in a different hierarchy. Those details affect conversion as much as they affect compliance.

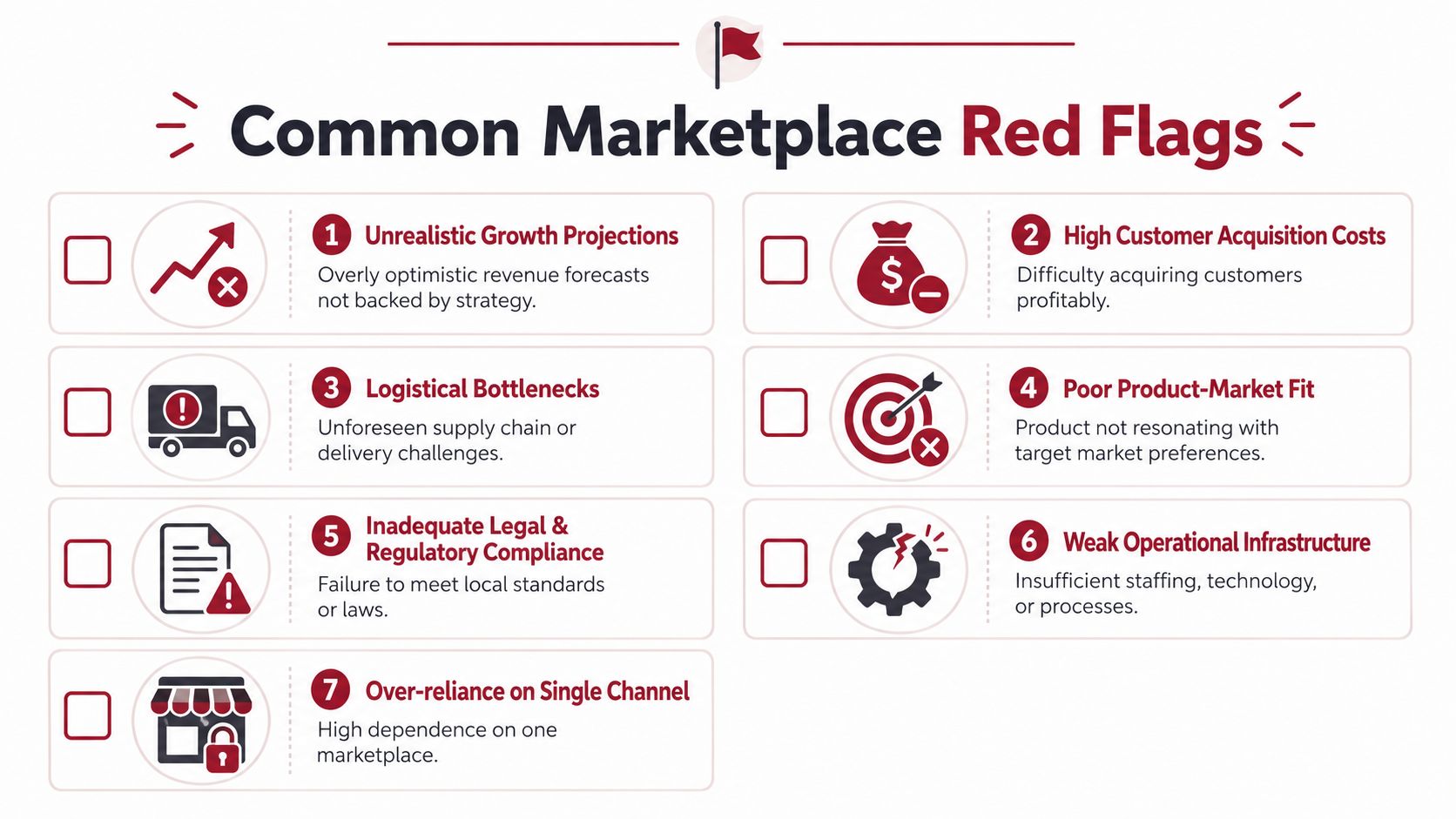

Red Flags We See in Marketplace Ecosystems

A healthy-looking opportunity can still produce a weak commercial outcome. The red flags usually appear in the gaps between the spreadsheet and the customer journey.

Fragmentation that looks like reach

Some markets appear attractive because the brand can list broadly, appoint multiple partners, and spread inventory across channels. That can create visibility, but it can also weaken control.

When catalogue structure, pricing, fulfilment standards, and content quality vary by channel, the customer stops seeing one brand. They start seeing disconnected buying experiences. In premium and specification-led categories, that disconnect often lowers trust before it lowers sales.

A recent marketplace review revealed a recurring pattern in mature consumer categories. Brands weren't failing because demand was absent. They were losing coherence across sellers, content standards, and delivery promises.

Price visibility without price discipline

Marketplaces compress pricing mistakes. Once products become easily comparable, weak channel discipline shows up fast.

Red flags include:

- Frequent undercutting: Sellers chase the buy box or retailer parity without regard for long-term positioning.

- Promotional dependence: Sales only move when discounts do the work.

- Margin blindness: Teams pursue gross sales while contribution erodes.

- Bundle confusion: Different pack sizes, accessories, or variants make pricing architecture harder to defend.

This matters most for brands trying to preserve a premium position. If the target ecosystem trains customers to sort by price first and evaluate quality second, the brand may need a different route to market.

Fulfilment structures that damage trust

Customers don't separate product quality from delivery experience as neatly as operators do. If the item arrives late, damaged, incomplete, or poorly supported, they blame the brand.

That makes fulfilment a commercial issue, not just an operational one. One issue we repeatedly observe is that teams model fulfilment as a cost line when they should model it as part of conversion, review quality, and retention.

| Warning sign | Why it matters commercially |

|---|---|

| Unstable delivery performance | Customers hesitate to buy higher-value items |

| Poor oversize handling | Damage and returns erode trust and margin |

| Weak inventory positioning | Delivery promises become inconsistent |

| Fragmented seller fulfilment | The same product creates uneven customer experiences |

Claimed demand that doesn't convert cleanly

What becomes visible during international expansion is the gap between stated interest and actual buying behaviour. Customers may say they value quality, durability, or design. On the marketplace, they may still choose the better-reviewed option, the faster-delivered option, or the one with clearer install guidance.

That's why diligence needs more than category enthusiasm. It needs evidence that the product's real strengths are visible and rewarded in that ecosystem.

Brands exploring broader online selling strategy often discover that channel access is the easy part. Commercial fit is harder. The winning brands don't just enter more places. They enter places where their economics and trust signals remain intact.

If a marketplace forces the brand to behave like a commodity, the issue isn't traffic. It's fit.

Cross-Border Diligence for Hardware Brands

A well-established Australian hardware brand can look ready for international growth long before it's operationally ready for international execution.

Take a hypothetical brand with strong domestic sell-through, recognised packaging, and dependable retail relationships. It now wants to enter the US through Amazon and a home improvement channel. The internal story sounds convincing. Proven product. Existing traction. Clear category demand. That's usually the point where commercial due diligence starts stripping away convenient assumptions.

Where the first cracks usually appear

The product may already perform in Australia, but region-specific validation is still essential. Public commercial due diligence guidance notes that a brand can show strong domestic traction and still fail internationally if packaging, claims, distribution model, or compliance burden change the economics of the deal (cross-border commercial due diligence considerations).

For hardware brands, those issues show up quickly.

A drill accessory range may need revised claims language. A fastening product may need different standards references. Installation instructions may need rewriting for local terminology, substrate assumptions, and use-case expectations. Even where the core product remains the same, the surrounding commercial presentation often doesn't.

What the diligence process would test

An operator-led review becomes more useful than a generic market-entry memo.

It would pressure-test at least five areas:

- Compliance translation: Does the product file support the target market's standards, labels, manuals, and claim hierarchy?

- Packaging fit: Will the existing pack communicate clearly in a US aisle, a US product page, or a contractor-led buying environment?

- Distribution design: Is the model built for direct marketplace fulfilment, local warehousing, retail replenishment, or a staged mix?

- Return logic: Can the business absorb the practical cost and operational friction of returns, replacements, and support requests?

- Channel conflict: Will marketplace entry disturb existing distributor ambitions, pricing logic, or future retail negotiations?

The result isn't just yes or no

Good diligence rarely produces a simple answer. It usually produces a more disciplined one.

Sometimes the conclusion is to proceed, but with narrower assortment, revised claims, local stockholding, and a different support model. Sometimes the answer is to delay launch until product files, packaging, and service workflows catch up. Sometimes the product is viable, but only through one route to market rather than several.

That's especially true for brands considering how to sell on Amazon while also preserving longer-term value in wholesale, trade, or specialist retail. The marketplace decision can't be separated from the rest of the ecosystem.

Cross-border success usually depends less on whether the product can be listed, and more on whether the full operating model still makes sense after localisation.

For hardware and home improvement brands, that distinction protects more than launch efficiency. It protects brand value.

From Diligence to a Defensible Growth Strategy

The strongest expansion plans don't begin with certainty. They begin with scrutiny.

Commercial due diligence earns its value when it turns an attractive expansion narrative into a tested commercial position. It shows where the assumptions are solid, where the model is fragile, and what has to change before the next market becomes worth pursuing. That's very different from expansion by momentum, where domestic success becomes proof by default.

What disciplined brands do differently

They don't confuse access with fit.

They ask whether the next market can support the brand's margin structure, service expectations, pricing architecture, channel relationships, and customer trust signals. They treat fulfilment, localisation, and compliance as part of the commercial model. They don't leave those issues for “after launch”.

That discipline matters because international growth isn't just additive. A poorly structured expansion can distort pricing, increase support load, fragment the customer experience, and weaken confidence in the brand across channels.

Why this protects long-term value

A strong diligence process creates better decisions in both directions. It gives leadership the confidence to proceed when the case is real, and the discipline to pause when the market is only superficially attractive.

That's how brands avoid entering markets that reward the wrong behaviour. It's also how they identify the adjustments that make a good opportunity workable. Different packaging. Different assortment. Different inventory strategy. Different route to market. Better timing.

The commercial point is simple. Expansion should strengthen the brand, not just extend its footprint.

When commercial due diligence is handled properly, market entry stops being a hopeful leap. It becomes a deliberate move with clearer economics, stronger execution logic, and a much better chance of compounding value over time.

If you're assessing whether a new marketplace, region, or channel is viable for your brand, TPR Brands helps established product companies evaluate expansion through an operator-led commercial lens. That includes channel fit, localisation risk, compliance readiness, marketplace ecosystem structure, and the practical realities that determine whether growth will hold once the launch excitement fades.