A brand finally gets the call it has been chasing. A serious retailer wants terms. A distributor wants exclusivity. A marketplace partner says they can generate volume fast. On paper, this looks like commercial validation.

In practice, this is often where brand erosion begins.

One pattern we continue seeing is that wholesale pricing is treated like a finance exercise, but it functions as a channel control system. If the price architecture is too loose, the wrong partner can discount aggressively, train the market to wait for lower pricing, and destabilise every other account around them. If it's too simplistic, margin disappears before the brand has enough influence to fix it. And if it's copied across regions without local adaptation, expansion starts profitable in theory and ends fragile in reality.

That's why a serious wholesale pricing strategy isn't just about what you charge. It's about what behaviour your structure rewards, what kind of partner ecosystem it creates, and whether the brand still looks coherent after channel expansion.

The Founder's Dilemma in Wholesale Expansion

The founder's dilemma usually starts with momentum. A product is working. Retail demand is real. Online traction has created inbound interest. Then a larger wholesale opportunity appears, and the commercial instinct is to secure the order first and refine the structure later.

That sequence causes more damage than teams often expect.

A wholesale account doesn't only buy inventory. It changes the shape of your market. It influences where customers encounter the brand, what price they come to expect, how smaller stockists perceive fairness, and whether future partners trust the commercial structure. Once pricing enters multiple channels, it stops being a private internal decision.

Why top-line excitement creates pricing mistakes

Founders often focus on immediate revenue because the purchase order feels tangible. The less visible issue is that poor pricing terms can lock in future instability. A low opening price may help close a deal, but it also creates a reference point that other accounts will eventually discover, directly or indirectly.

Across multiple marketplace ecosystems, the same pattern appears. Brands that expand quickly without pricing discipline often confuse distribution growth with ecosystem strength. They aren't the same thing. More doors can mean less control.

Practical rule: If a wholesale deal only works because the price is unusually soft, the problem usually isn't partner acquisition. It's that the commercial structure hasn't been designed to survive scale.

This is especially relevant when brands move into marketplaces alongside wholesale distribution. A marketplace listing can expose pricing inconsistencies much faster than traditional trade channels. One discounted seller can make the entire brand look disorganised.

That's why expansion shouldn't be framed as “getting on more channels”. The more useful framing is building a controlled commercial environment. The same logic sits behind why launching on Amazon is the wrong goal. Ultimately, the objective is channel coherence, not channel presence.

Pricing is a brand governance tool

The strongest operators treat wholesale pricing strategy as part of brand governance. They don't ask only, “What margin can we afford to give?” They ask tougher questions.

- What partner behaviour does this structure encourage

- Can a retailer still earn properly without racing to the bottom

- Will this price hold if freight, compliance, and support costs rise

- Does this structure protect the brand when the catalogue expands

The Australian context makes this more commercially concrete. The retail trade industry recorded A$367.4 billion in turnover in the 2023–24 financial year, and the ABS tracks retail turnover monthly because pricing, promotion, and channel mix can materially change sales outcomes across categories, as noted in this discussion of Australian wholesale pricing dynamics. For wholesalers, that means pricing can't sit still. It has to account for retailer margin expectations and channel realities, not just internal cost assumptions.

A healthy wholesale model protects both margin and market trust. A weak one seeds channel conflict long before anyone notices it in the P&L.

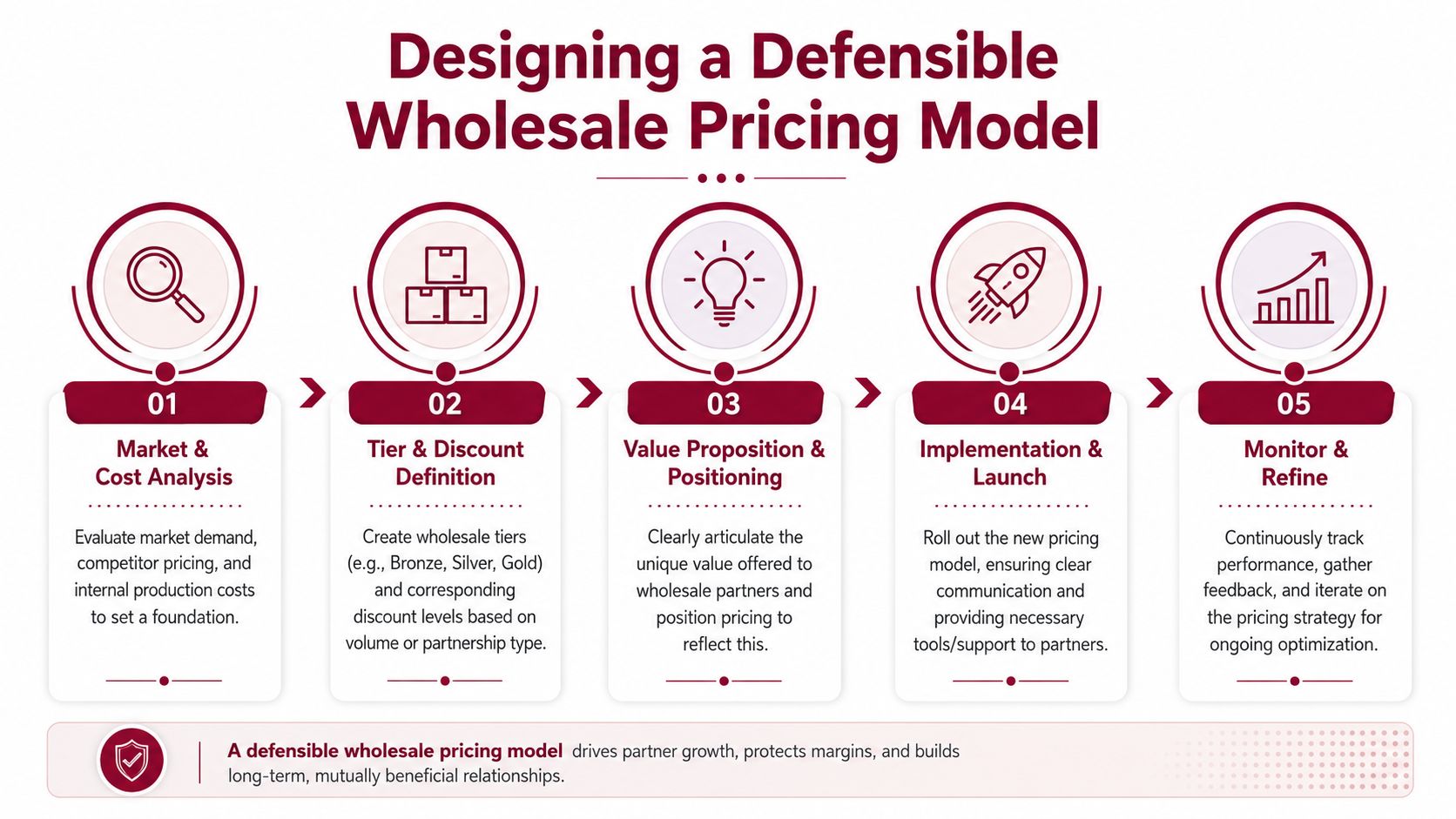

Designing a Defensible Wholesale Pricing Model

A founder agrees to a wholesale deal that looks profitable on paper. Six months later, the account is growing, reorder volume looks healthy, and margin is worse than expected. The problem usually sits in the pricing architecture, not in sales execution.

A defensible wholesale pricing model sets commercial boundaries before the channel starts testing them. It gives the brand a floor it can protect, enough room for partners to earn properly, and a structure that can survive expansion into new accounts, new marketplaces, and new countries.

Start with fully loaded unit cost

Founders often treat cost as a manufacturing number. Wholesale punishes that shortcut. The usable floor has to reflect what it takes to supply, support, and protect the account over time.

That usually includes:

- Product acquisition cost. The direct cost of the item itself.

- Inbound freight and handling. The cost of getting stock into the network in saleable condition.

- Storage and fulfilment burden. Warehousing, pick-pack complexity, and channel servicing overhead.

- Commercial friction costs. Packaging compliance, account support, damage allowance, and operational exceptions.

Some brands also need to account for sampling, promo contributions, retailer onboarding work, or marketplace compliance overhead. If those costs sit outside the model, the wholesale price becomes an optimistic guess.

Set the floor first

The starting point is straightforward. Build the floor from fully loaded unit cost and required gross margin, then test that number against retail reality.

A floor price is not a target for the sales team. It is the point where the brand stops funding channel growth out of its own margin.

That market test matters because a mathematically clean price can still fail in trade. If the retailer cannot earn enough after freight, markdown risk, and shelf competition, they will force the issue later through discount requests, range rationalisation, or poor replenishment behaviour. Price tension usually shows up after the deal is signed, when it is harder to correct.

Don't apply one margin across the whole range

A flat margin target across the assortment looks tidy and creates the wrong incentives. Different SKUs place different demands on the business and play different roles in the channel.

A small accessory with low handling cost can carry margin differently from a fragile item with higher claims risk. A hero SKU that drives discovery should not always be priced the same way as a long-tail product that moves slowly and ties up working capital. Premium bundles bring another problem. They can look margin-rich while absorbing more support, more returns exposure, or more promotional pressure than expected.

We see brands damage their own channel position when they standardise margin too early. Retailers then over-index on the easiest products to sell, underinvest in the rest of the line, and judge the brand by the weakest economics in the range.

External pricing guidance reaches the same conclusion. This analysis of wholesale pricing mistakes points to lowball pricing and one-size-fits-all margin setting as recurring causes of margin leakage.

Design pricing layers around channel role

Strong wholesale pricing models are built in layers. The question is not only how much discount an account wants. The better question is what role that account plays in the ecosystem and what behaviour the price structure is rewarding.

| Channel situation | Pricing consideration | Strategic purpose |

|---|---|---|

| Independent retailers | Protect enough margin for local selling effort | Preserve advocacy and store-level commitment |

| Volume wholesale accounts | Reward scale carefully, with guardrails | Capture reach without collapsing brand value |

| Marketplace-focused partners | Tighter controls and clearer rules | Reduce undercutting and pricing noise |

| Regional distributors | Build in support for logistics complexity | Reflect service burden and local execution risk |

Commercial discipline matters. A lower net price can be justified if the partner improves geographic coverage, funds inventory, supports launch execution, or reduces servicing cost. It is a poor trade if the only outcome is more volume at a lower quality of demand.

The same logic applies to marketplace exposure. Many margin problems blamed on Amazon start earlier, in wholesale terms that gave the wrong partner too much room to discount. That pattern sits close to why margins shrink on Amazon when upstream pricing lacks control.

Defensible pricing protects more than gross margin. It protects account quality, channel trust, and the brand's ability to expand without training partners to expect concessions every time growth slows.

Using Tiers and MAP to Build Ecosystem Cohesion

When pricing discipline breaks down, brands usually blame discounting. The deeper issue is often structural. The channel has no clear rules for who gets rewarded, who gets protected, and what kind of pricing behaviour is acceptable.

That's where tiering and MAP become commercially useful.

Tiering creates incentives without chaos

A tiered structure tells partners that growth is possible, but not on arbitrary terms. It separates committed accounts from opportunistic ones and gives the brand a mechanism for rewarding desired behaviour.

Useful tiering usually considers a mix of factors rather than simple volume alone:

- Order pattern quality. Consistent replenishment is often healthier than sporadic bulk buying.

- Channel fit. A partner that represents the brand well can be more valuable than one that moves cartons.

- Operational reliability. Forecasting discipline, claims management, and payment behaviour all affect account quality.

- Brand stewardship. Partners who protect positioning should not be treated the same as those who create constant pricing friction.

Equal treatment can create unequal outcomes. If every account receives roughly the same economics regardless of behaviour, the brand effectively funds disorder.

MAP is about trust, not restriction

A Minimum Advertised Price policy is often misunderstood as a punitive device. In practice, well-run brands use it to preserve channel confidence. Smaller retailers need to believe they can stock the brand without being immediately undercut by a high-volume marketplace seller willing to sacrifice margin for turnover.

That doesn't mean MAP solves every pricing problem. It doesn't. If wholesale terms are already too soft, MAP becomes a patch on a deeper structural issue. But when paired with sensible tiering, it helps create a more predictable ecosystem.

Smaller stockists rarely leave because they dislike the product. They leave because the pricing environment tells them the brand won't protect their effort.

Brand perception and channel mechanics intersect. If consumers see erratic advertised pricing across the market, they don't interpret that as “healthy competition”. They often interpret it as inconsistency, overdistribution, or low control.

What stronger brands do differently

The better operators usually make a few disciplined choices.

First, they separate wholesale access from pricing privilege. Not every approved account gets the same commercial terms.

Second, they define consequences in advance. If a partner repeatedly creates pricing instability, the brand doesn't improvise its response under pressure.

Third, they communicate the structure clearly enough that partners understand the logic. Ambiguity invites negotiation games. Clarity builds confidence.

A useful benchmark is whether your best partners feel safer as the network grows. If growth makes good partners more anxious, the architecture is wrong.

For founders dealing with aggressive marketplace discounting, why discounting on Amazon is a sign you've lost control is usually less about the platform itself and more about what happened upstream in pricing design.

For a practical view on channel discipline, this short clip is worth watching:

Adapting Your Pricing for International Markets

A founder signs a new distributor in another country, converts the domestic wholesale price into local currency, and expects the model to hold. Six months later, the distributor is asking for support, retailers are resisting the margin structure, and the brand is being advertised at prices that clash with its home market. The problem usually started long before the first discount. It started in the price build.

International wholesale pricing is a channel design decision. Currency matters, but it sits inside a larger system of duties, tax treatment, freight, local compliance, payment terms, inventory risk, and retailer margin expectations. If those factors are handled loosely, the brand enters the market with a structure that encourages exceptions from day one.

Why domestic pricing logic breaks across borders

The same SKU can be healthy in one country and weak in another because the local cost stack changes who absorbs pressure. In one market, the importer carries more working capital. In another, the retailer expects a wider margin to justify shelf space or promotional activity. In another, compliance, labelling, and registration costs sit in the background until they start eroding every order.

I see this often with brands entering Australia. The opening numbers usually reflect factory cost, broad freight assumptions, and a target markup. They often miss what happens from port to warehouse, and what local partners need to make the brand commercially worth backing. That gap rarely looks dramatic in a spreadsheet. It becomes obvious once stock lands and everyone starts protecting their own margin.

Generic advice on wholesale pricing often stays too close to COGS and markup. It does not spend enough time on landed cost, channel margin, and in-market operating friction. That is why this perspective on wholesale pricing strategy and competitive edge is useful as a broad reference point, even though each market still needs its own commercial model.

Build the price from the market back to the factory

Good international pricing starts with the downstream reality. What price can the market support without damaging the brand position? What margin does the retailer or distributor need to stay engaged? What local costs must be covered before the brand sees a clean gross margin?

Then work back through taxes, duties, freight, storage, compliance, payment terms, and support costs until the ex-factory economics are clear.

That discipline matters in Australia. GST, import costs, and local service expectations affect quoting structure as much as they affect margin. Wholesale offers need a clean separation between ex-GST pricing, freight, and any other chargeable elements so commercial teams, finance teams, and channel partners are all working from the same logic. If that separation is blurred, the quote may look attractive at first and unworkable once accounts start reconciling real costs.

A region-specific pricing checklist

Brands entering a new country usually need a fresh price architecture, not a translated domestic sheet.

| Pricing variable | Why it matters in international wholesale |

|---|---|

| Local tax structure | Changes invoice treatment, quoting logic, and margin visibility |

| Import duties and border costs | Raises the floor price before local selling begins |

| In-country warehousing | Affects service levels, reorder economics, and account profitability |

| Retailer margin expectations | Shapes whether the offer works downstream without forced discounting |

| Compliance requirements | Adds cost and operating friction that simple markups miss |

The practical question is straightforward. What must this price absorb in that market, and can every participant in the channel still make money without degrading brand position?

This is also why Amazon distribution strategy in international channel planning needs to be addressed early. Marketplace distribution is not a side issue once a brand crosses borders. It influences price visibility, reseller behaviour, and how quickly local inconsistencies become public.

Local adaptation protects more than margin

Poorly adapted pricing creates brand conflict before it creates a finance problem. One country starts discounting because the importer bought into a weak margin structure. Another holds full price because the local model was built properly. Customers compare. Retail partners notice. Sales teams start asking for one-off concessions to keep the peace.

I have seen brands blame distributors for this when the actual failure sat upstream in the price design.

Strong operators localise pricing to preserve channel order. They decide in advance what the market needs, what the brand can tolerate, and what the floor price must protect. That approach supports expansion without teaching each new market that pricing is open for negotiation.

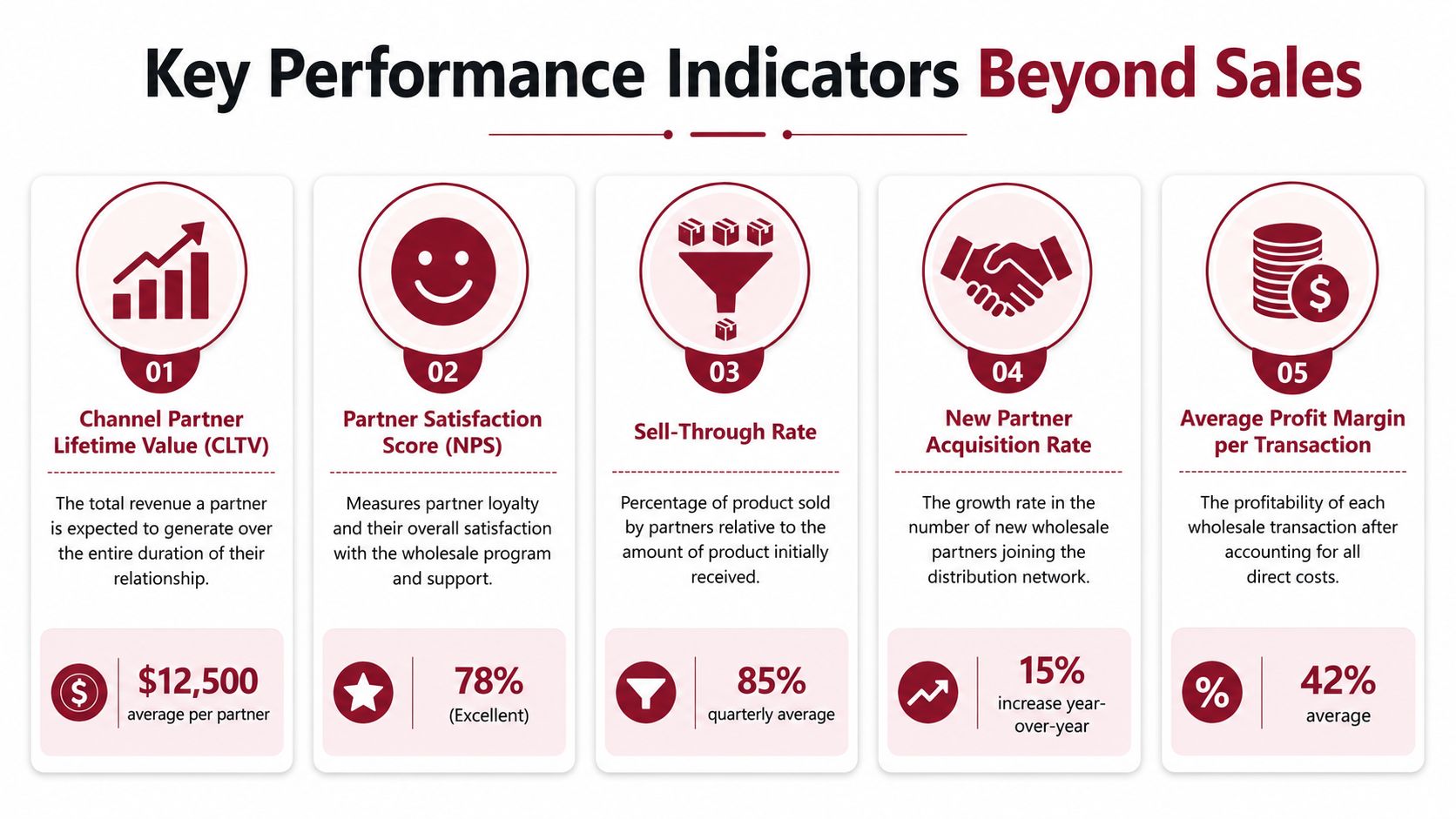

Measuring Success Beyond Volume and Revenue

A distributor places a strong opening order, the sales team celebrates, and the quarter closes ahead of target. Six months later, the same account is asking for credits, retailers are discounting to clear stock, and your better partners are asking why they are protecting a price that others are free to break.

That is why shipment volume and top-line revenue are weak signals on their own. They show movement. They do not show whether the channel is getting healthier, more disciplined, or harder to control as you grow.

The metrics that actually reveal channel health

The useful question is not how much product left the warehouse. It is whether the pricing model produced a stable market after the product arrived.

A better review process tracks a small set of indicators together:

- Margin integrity by channel. Which account types hold the planned economics, and which ones erode them through discounts, rebates, or service costs.

- Sell-through quality. Whether partners are creating repeat consumer demand or just taking in stock for a short-term buy.

- Price compliance behaviour. Whether partners stay inside the structure you set, or keep probing for exceptions.

- Reorder pattern stability. Whether replenishment follows a credible sales rhythm or swings between overbuying and silence.

- Exception frequency. How often the business approves one-off terms, credits, extended dating, or special pricing to keep accounts active.

None of these metrics looks impressive in a board deck. All of them show whether the channel can scale without damaging the brand.

Review price performance before partners reset the market

Review cadence matters because markets learn fast. If a brand waits until margin pressure becomes visible in the P&L, retailers and distributors have usually already adjusted their expectations. At that point, the discussion is no longer about strategy. It is about damage control.

The practical test is straightforward. Revisit your floor price, your realised margin by channel, and the gap between intended sell-through and actual sell-through. Then check where exceptions are clustering. If one partner segment needs constant help to make the model work, the problem is usually in the structure, not in the latest negotiation.

I have seen brands misread this stage. They treat repeated pricing requests as isolated account management issues when they are really signs that the wholesale model is teaching the market the wrong behaviour.

A management lens that keeps the signal clear

Founders and commercial leads do not need a complicated dashboard. Four recurring questions usually expose the problem early:

- Are we earning the margin we planned, by channel?

- Are our strongest partners getting healthier, or harder to retain?

- Is sell-through strong enough to support predictable reordering?

- Are pricing exceptions becoming routine?

If those answers start to weaken, the brand is losing control of the ecosystem, even if reported revenue is still rising.

The hardest pricing problems to fix are the ones a business starts treating as normal operating practice. Once exceptions become part of the channel contract, recovering price authority gets far more expensive.

Volume matters. Revenue matters. The better measure is whether wholesale growth is producing a more resilient channel, stronger partner behaviour, and better protection for brand value.

Pricing as a Strategic Capability

A founder opens wholesale in a new market, signs a few promising accounts, and sees revenue move quickly. Six months later, the channel is noisy. One retailer wants special terms, another is discounting early, a distributor is asking for market-specific support, and the direct channel is starting to feel the pressure. At that point, pricing is no longer a spreadsheet exercise. It is the control system for the brand.

Leadership teams need to treat wholesale pricing that way. Price determines who can sell the brand profitably, how partners behave under pressure, and whether expansion adds reach or weakens positioning. If those decisions sit too low in the organisation, the business starts solving strategic problems through one-off concessions.

The stronger operators build pricing into commercial design. They set the boundaries for discounting, define which channel roles justify different terms, and decide who has authority to approve exceptions. That discipline protects more than margin. It protects retailer trust, keeps marketplace activity from undermining account relationships, and gives international growth a structure that can hold together.

In practice, leadership should own four areas:

- Term boundaries. Set which elements of the offer can change, and which ones stay fixed across the channel.

- Partner fit. Match pricing to the role each account plays in reach, positioning, and reorder potential.

- Enforcement rules. Document pricing expectations, breach handling, and the consequences of repeated non-compliance.

- Approval control. Limit who can alter trading terms so short-term sales pressure does not rewrite channel policy.

This matters even more once tax, freight, and cross-border selling enter the picture. In Australia, GST affects how prices are quoted, reconciled, and compared across channels. Serious operators separate the ex-GST base price from taxes, landed cost inputs, and market-specific adjustments because loose headline pricing creates confusion fast, especially when distributor and marketplace economics are already under strain.

The long-term test is simple. Does the pricing model help the brand expand while keeping partner behaviour aligned with brand value?

Strong products can win an opening order. A coherent pricing structure is what keeps the channel investable. It tells good partners the brand is stable, tells weak partners the rules are real, and gives the business a way to grow internationally without teaching each new market a different version of the brand.

If your business is preparing for channel expansion, distributor conversations, or international marketplace entry, TPR Brands helps established product companies build commercially coherent growth plans that protect brand value while opening the right next markets.