The most popular advice on international expansion still gets one thing badly wrong. It assumes risk is mainly about compliance paperwork after the commercial decision has already been made.

That's backwards.

For Australian hardware and home improvement brands, a risk assessment framework isn't an admin layer that sits behind growth. It's the operating structure that tells you whether the growth path is commercially sound in the first place. A product can be proven in Australia, loved by domestic retail buyers, and still underperform or create liability once it enters a different marketplace ecosystem.

One pattern we continue seeing is founders treating overseas entry as a channel extension. In practice, it's an ecosystem transition. Product expectations shift. Fulfilment pressures change. Returns behaviour changes. Liability standards change. Even a small mismatch between product claims, packaging, testing evidence, and local platform requirements can turn a strong catalogue into a fragile one.

Why Strong Products Falter in New Marketplace Ecosystems

A strong domestic product often fails overseas for reasons that have nothing to do with product quality. The problem is usually structural. The brand enters a new market carrying assumptions that were built for Australia, then discovers the surrounding system works differently.

That's why a risk assessment framework matters far earlier than often realized. It helps founders pressure-test the operational fit between the product, the market, and the compliance environment before inventory is committed and channel conflict starts to build. Businesses expanding through online selling channels across regions usually discover that marketplace traction depends on much more than listing visibility.

The product is rarely the only variable

A hardware brand can be well made, competitively priced, and commercially proven in Australia, yet still struggle in the US or UK because the surrounding ecosystem asks different questions. Local regulators may focus on different labelling details. Marketplaces may enforce documentation standards differently. Retail and marketplace pricing may collide in ways that weaken trust instead of strengthening it.

A 2025 ACCC report found that 68% of non-compliance incidents among expanding Australian manufacturers stemmed from using a single, AU-centric risk framework across multiple jurisdictions, while overlooking differences in labelling, testing, and liability standards, as referenced in this risk framework analysis.

Strong products don't automatically become strong international brands. They become exposed products if the operating assumptions don't travel with them.

Where founders usually misread the risk

The common mistake isn't carelessness. It's overconfidence in domestic proof. Teams assume their Australian compliance history, supplier relationships, and packaging logic will transfer cleanly into new regions. Often, they don't.

A simple way to think about it is this:

| Expansion assumption | What often happens in-market |

|---|---|

| Domestic compliance should be enough | New jurisdictions ask for different evidence, warnings, or test references |

| Existing packaging can be reused | Local labelling or consumer disclosure rules create rework |

| Marketplace launch is a sales event | It becomes an operational stress test across returns, claims, and support |

| One risk model can cover all countries | Regional differences create hidden gaps and duplicated effort |

When static planning fails, a risk assessment framework gives leadership a way to identify which assumptions are stable, which are market-specific, and which could damage margin or brand trust if left unresolved.

What a Risk Assessment Framework Actually Is And Is Not

Many organizations say they have a risk framework when what they possess is a collection of compliance files, supplier notes, and issue logs. That isn't the same thing.

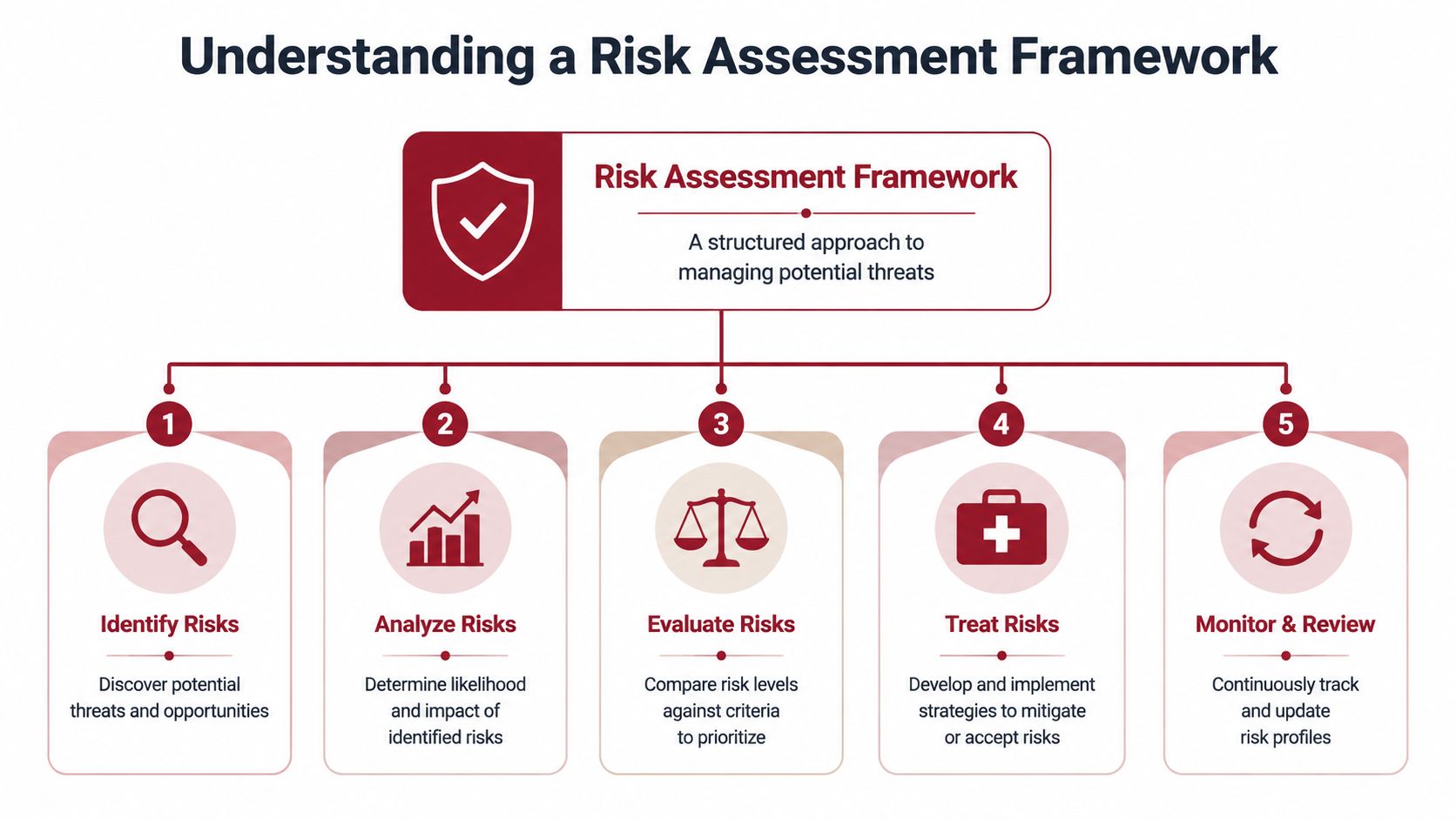

A genuine risk assessment framework is a decision system. It gives the business a consistent way to identify risk, judge severity, decide what needs action, and review whether the controls still hold once trading conditions change.

What sits inside a real framework

At a practical level, most effective frameworks include five working parts:

- Risk identification. What could disrupt product launch, compliance, supply continuity, margin, or customer trust?

- Risk analysis. How likely is that issue, and how severe would the impact be?

- Risk evaluation. Which risks are acceptable, and which exceed the business's thresholds?

- Risk treatment. What controls, documentation, supplier changes, insurance decisions, or market restrictions will reduce exposure?

- Monitoring and review. What has changed since the last decision?

This isn't theoretical. Historical data shows adoption of risk assessment frameworks in the Australian consumer product sector rose from 32% to 79% between 2015 and 2025, correlating with a 28% increase in successful international market expansions, according to this definition of risk assessment frameworks.

What it is not

It's not a once-a-year workshop.

It's not a spreadsheet that nobody updates.

It's not a supplier declaration folder being mistaken for active risk management.

And it isn't a substitute for commercial judgement. Good operators still make calls under uncertainty. The framework forces those calls to be made with clearer thresholds and better evidence.

Practical rule: If the document can't tell your team whether to delay a launch, rework packaging, switch suppliers, or limit a market entry, it isn't functioning as a real framework.

Why checklists fail under expansion pressure

A checklist can confirm whether a task was completed. It can't tell you whether the control is still valid once you change geography, channel mix, freight flows, or retail structure.

That's the key distinction. A checklist asks, “Did we do the task?” A risk assessment framework asks, “Does this decision still make sense under these conditions?”

Commercially mature brands often borrow from standards such as ISO 31000 because the discipline is useful. Not because they want more paperwork, but because they need a repeatable way to connect governance, operations, and expansion decisions. The framework becomes most valuable when the business is moving fast and the cost of being wrong rises with every shipment, listing, and local adaptation.

Measuring What Matters Quantitative vs Qualitative Risk

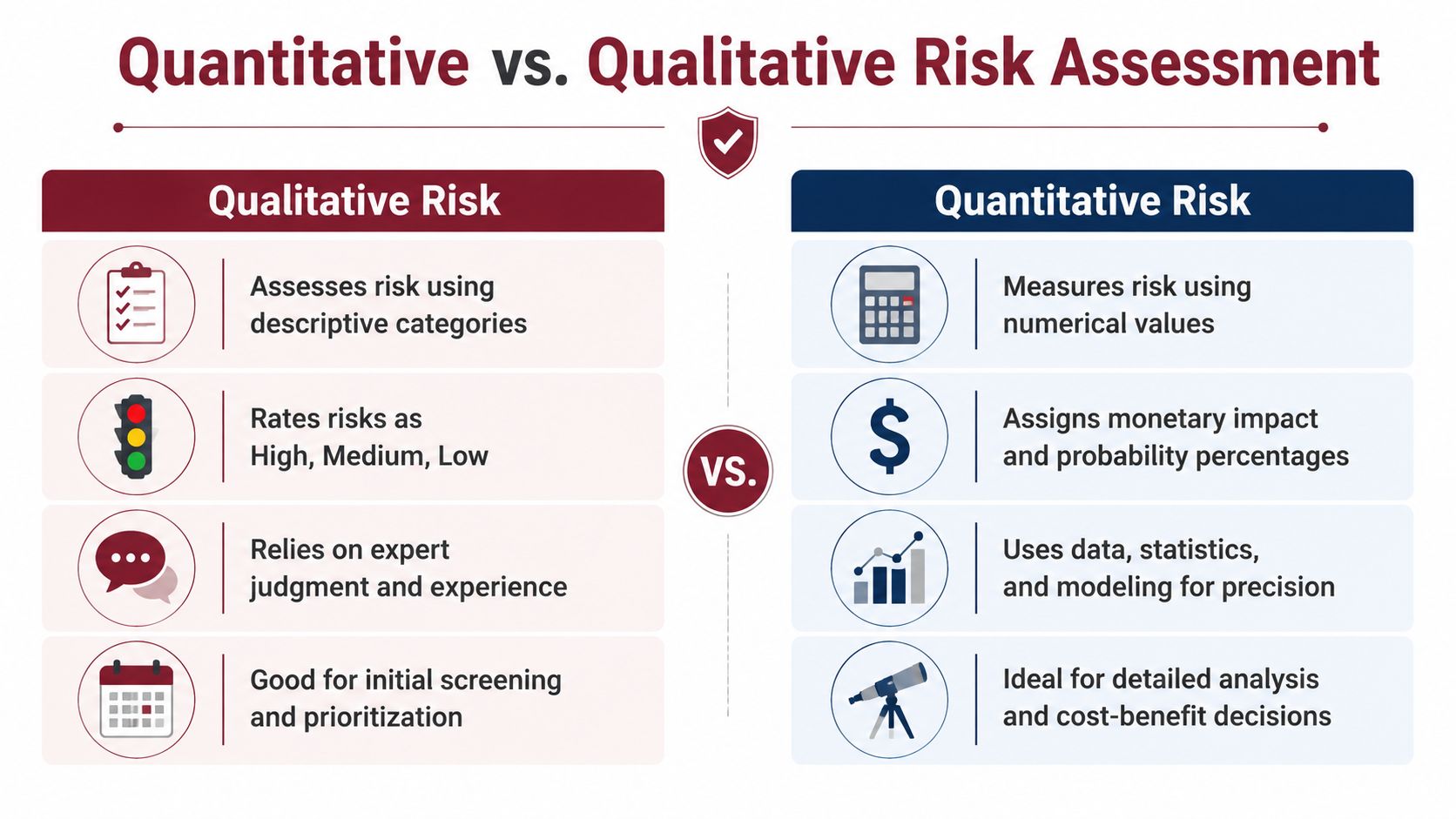

Many risk discussions break down because the language is too vague. “High risk” means one thing to a founder, something else to an operations lead, and something very different to a finance team reviewing downside exposure.

That's why the strongest risk assessment frameworks don't rely on one method alone. They blend qualitative judgement with quantitative translation.

Where qualitative scoring helps

Qualitative assessment is useful early. It lets a team map a broad risk field quickly. You can rank issues such as supplier reliability, packaging exposure, returns abuse, documentation gaps, or marketplace account vulnerability without waiting for perfect data.

That speed matters during expansion. Leaders need an initial view of where the weak points sit.

Qualitative methods are especially helpful when the brand is evaluating:

- New jurisdictions where operating history is limited

- Emerging product lines with incomplete claim validation

- Channel conflict exposure where retailer and marketplace reactions are hard to model precisely

Where qualitative scoring stops being enough

The weakness appears when leadership has to allocate capital. If one risk is rated “high” and another is also rated “high”, which one gets budget first? Which issue justifies delaying launch? Which one affects inventory planning?

That's where quantitative thinking becomes commercially useful.

Later in the decision process, this video gives a helpful visual overview of how risk methods are often approached in practice.

The better approach is translation

Technically sound frameworks convert qualitative likelihood and impact ratings into quantified financial loss, then refresh the register using KRIs so scores stay reliable as conditions change, as noted in the linked framework definition earlier.

In plain terms, that means the team starts with judgement, then translates priority risks into commercial terms. Not every issue needs a detailed model. Only the decisions that materially affect launch timing, supplier structure, compliance cost, or downside exposure.

When founders can attach a financial consequence to a control failure, the conversation changes. Risk stops sounding like internal caution and starts sounding like business reality.

A practical comparison looks like this:

| Method | Best use | Limitation |

|---|---|---|

| Qualitative | Fast screening and shared team alignment | Can become subjective and hard to prioritise |

| Quantitative | Capital allocation and mitigation decisions | Needs cleaner assumptions and stronger data |

| Blended model | Early speed plus later financial clarity | Requires discipline to keep updating inputs |

The mistake isn't using qualitative scoring. The mistake is stopping there.

Mapping Risks Specific to Hardware and Home Improvement Brands

Hardware and home improvement brands carry a risk profile that generic frameworks often miss. These products sit at the intersection of physical safety, product claims, supply chain integrity, packaging accuracy, and channel complexity. A template built for general consumer goods usually won't go deep enough.

One issue we repeatedly observe is that teams can describe their product strengths in detail but struggle to map where the actual exposure sits once the product moves across borders. They know the SKU. They know the factory. They know the margin target. But they haven't linked those variables into a live risk structure.

The categories that usually deserve direct attention

A useful framework for this sector often needs to separate risk into distinct operating categories.

- Supply chain integrity. Material changes, subcontracting, inconsistent factory controls, and incomplete import documentation can create exposure long before a customer sees the product.

- Product safety and liability. Hardware products live closer to injury, installation error, misuse, and claim scrutiny than many general merchandise categories.

- Regulatory fit. Testing evidence, packaging statements, instructional wording, and product claims may need local adaptation by market.

- Channel conflict. A product can be compliant and still commercially unstable if pricing, reseller behaviour, or marketplace discounting undermines the wider network.

- After-sales strain. Returns, spare part expectations, warranty interpretation, and customer support burden can differ sharply across regions.

Supply chain risk is usually underestimated

For many brands, the highest exposure doesn't begin in the marketplace. It begins upstream.

Australian hardware firms lost an average of $1.2M annually due to supply chain risk failures linked to inadequate risk frameworks, with 73% of losses tied to non-compliance with AU import standards, according to Australian Bureau of Statistics 2025 data referenced in the verified material.

That matters even when the expansion market is offshore. If the inbound compliance logic into Australia is weak, it often points to broader control weaknesses in supplier verification, documentation discipline, and specification management. Brands preparing to sell on Amazon in a controlled way often discover that marketplace readiness is inseparable from supply chain discipline.

A generic framework misses category-specific realities

A recent marketplace review revealed a familiar pattern. The brand had documented business risks at a high level, but the framework didn't isolate category-specific failure points. There was no separate treatment for component substitutions, no trigger for updated test evidence after packaging edits, and no escalation path when local marketplace content created claims that the compliance file didn't support.

That kind of gap doesn't look dramatic on paper. In-market, it creates friction across listing approvals, customer trust, and downstream liability.

A hardware risk register should read like an operator built it, not like legal filed it.

Founders don't need a longer framework. They need a sharper one. The stronger model names the actual breakpoints that affect hardware and home improvement brands, then links each one to ownership, evidence, and a response threshold.

Navigating Cross-Border Compliance With a Dynamic Framework

The wrong way to expand is to build one master risk document in Australia and assume it can be stretched across every market. That approach feels efficient. It usually creates blind spots.

A better model is a dynamic, jurisdiction-aware risk assessment framework. The central logic stays consistent, but each market gets its own module for labelling, testing expectations, liability settings, product restrictions, platform standards, and documentation thresholds.

The core framework stays central

The base structure should remain stable across the business. Risk categories, scoring logic, review cadence, decision thresholds, and reporting ownership shouldn't change every time you enter a new country. That consistency matters because leadership needs one language for risk.

What changes is the market module attached to it.

For example, the framework may keep the same product safety category in every region. But the evidence required to clear that category in the US may differ from what's needed in the UK or Canada. The treatment plan also differs. One market may require revised packaging language. Another may demand a different documentation set. Another may force a change in who can act as importer or compliance contact.

What the modular model looks like

A practical structure often includes:

- Central risk logic with common scoring rules, ownership, and reporting lines

- Jurisdiction modules covering local legal and marketplace requirements

- Trigger events such as packaging revisions, supplier changes, product claim updates, or new platform enforcement rules

- Decision thresholds that tell the team when to proceed, pause, re-test, or restrict channel entry

Businesses entering new regions often need this tied tightly to their compliance documentation process, because fragmented files are one of the fastest ways for a sound product to become a difficult one.

Dynamic frameworks work because conditions move

Australia's national climate-risk guidance makes a framework operationally useful only when it combines physical-risk scenarios with transition-risk assumptions and ties both to decision thresholds for assets, supply chains, and capital allocation. It also points to the need to test multiple time horizons rather than relying on one static current-state score. The same operating principle applies in cross-border expansion. A framework only works when it responds to changing conditions rather than preserving an old assumption.

There's also direct evidence that structured frameworks improve outcomes. A 2023 report showed that 68% of Australian hardware manufacturers using a structured risk assessment framework reduced workplace incidents by 42% and saw a 35% decline in compliance failures related to product safety and sourcing.

Static compliance creates false confidence

A static framework gives management the feeling that risk has been handled. A dynamic framework shows whether the controls still match the market you're entering now.

That distinction matters. Founders don't lose control because they ignored risk entirely. They lose control because the framework they trusted stopped reflecting reality.

Building Your Commercially Resilient Risk Framework

A risk assessment framework only becomes valuable when it's embedded into normal commercial decisions. If it lives outside product development, sourcing, market entry, and channel planning, it won't shape outcomes when pressure rises.

The businesses that handle expansion well usually make three changes. They assign real ownership. They connect the framework to major decisions. They review it often enough that it stays useful.

Ownership has to be explicit

Risk frameworks decay when everyone assumes someone else is watching them. Legal thinks operations owns supplier changes. Operations thinks commercial owns market-entry choices. Commercial assumes compliance will raise a flag if something is wrong.

That diffusion is where preventable issues begin.

Clear ownership usually means:

- Commercial leadership owns the decision thresholds around entering, delaying, or restricting a market

- Operations or supply chain owns evidence quality around sourcing, factories, packaging changes, and import readiness

- Compliance or technical teams own the supporting documentation and regulatory interpretation

- Finance helps translate top risks into downside exposure and mitigation trade-offs

Reviews should follow operating change

Annual reviews are tidy, but they're often too slow. Frameworks are more reliable when they're reviewed after a material change. A new supplier. A packaging adjustment. A product claim revision. A move into a different fulfilment model. A new country launch.

Review risk when the business changes, not when the calendar says it's time.

That's also where commercially focused commercial due diligence becomes useful. It forces the business to test whether the assumptions behind growth are still credible under real operating conditions.

The framework should influence action

If the framework is working, it should occasionally tell the business something inconvenient. Delay the launch. Rework the carton. Tighten the claim set. Replace the supplier. Restrict a channel. Hold inventory until evidence is complete.

That isn't a brake on growth. It's how durable growth is built.

A resilient framework doesn't eliminate uncertainty. It helps leadership decide which uncertainty is acceptable, which risk needs treatment, and which expansion path isn't commercially sound yet.

TPR Brands works with established product brands that need more than marketplace execution. The firm helps founders and commercial teams assess whether their products, channels, compliance structure, and regional operating model are aligned for controlled expansion across Australia, the US, Canada, and the UK. If you're building a stronger international growth structure around proven products, explore TPR Brands.