Most founders ask the wrong question about product liability insurance. They ask what it costs.

The sharper question is what it enables.

One pattern we continue seeing is brands investing heavily in product, packaging, freight and channel outreach, then treating insurance as an administrative task to handle once a retailer, distributor or marketplace asks for it. That sequencing is backwards. By the time a major channel partner asks for proof of cover, they're not really asking whether you bought a policy. They're asking whether your business is organised enough to sit inside their commercial ecosystem without exporting unmanaged risk into it.

That distinction matters when you're trying to enter premium retail, secure distributor confidence, or expand into international marketplaces where trust is built long before the first purchase order lands.

Rethinking Product Liability Insurance as a Commercial Asset

A lot of businesses still view product liability insurance as a sunk cost. That's understandable, but commercially limiting.

For a scaling brand, the policy is often doing three jobs at once. It protects the business when something goes wrong, it signals operational maturity to buyers, and it removes friction from channel entry. When those three functions are aligned, insurance stops looking like overhead and starts behaving like infrastructure.

Why the defensive view is too narrow

In Australia, product safety isn't an abstract issue sitting somewhere in legal theory. Product Safety Australia records product-related incidents at a national scale, and the Australian Consumer Law, within the Competition and Consumer Act 2010, has applied nationally since 1 January 2011. It gives consumers rights to compensation for losses caused by unsafe goods, which means product liability exposure sits inside a statutory regime that has been active for more than a decade, as outlined in this overview of the state of product liability insurance in Australia.

That changes the commercial framing. You're not buying cover for a hypothetical edge case. You're operating inside a market where unsafe goods can trigger formal claims, regulatory attention, and channel disruption.

Practical rule: If a retailer, distributor or marketplace has to trust your product before they trust your growth plan, your insurance is part of the sales conversation.

Where expansion plans usually stall

A recent marketplace review revealed a familiar pattern. Brands often prepare listings, pricing files, creative assets and freight models, but the insurance document set doesn't match the demands of the next channel. The policy may be too narrow, the geography may be unclear, or the business hasn't organised supporting compliance material well enough to satisfy a serious buyer.

That's when momentum slows. Not because demand isn't there, but because the commercial foundation isn't ready.

This is also why insurance shouldn't be separated from broader brand protection work. A business that's serious about entering stronger channels usually needs insurance, documented compliance and IP discipline working together. The same founder thinking that protects product exposure should also inform intellectual property protection for expanding brands.

What stronger operators do differently

Better operators don't wait for a buyer to expose a gap. They structure cover early, review partner requirements before outreach, and treat the certificate of currency as one of several trust documents used to enable access.

That's the commercial shift. Insurance isn't just there to defend margin after an incident. It helps create the conditions for growth before the first incident ever happens.

Understanding Your Core Coverage and Its Gaps

The most useful way to understand product liability insurance is to stop thinking about it as factory-only protection.

Claims don't arise only because something was manufactured badly. They also arise because the product was designed poorly, described inadequately, or supplied with weak instructions. That matters for importers, distributors and brand owners who assume the manufacturer carries all the risk. Often, they don't carry all of it.

The three liability pathways founders need to watch

Australian market participants should treat cover as activated by defects in design, manufacture, or warnings and instructions, and distributors and importers can face exposure even when they didn't make the product, as noted in this discussion of insurance coverage for product liability risks.

That creates three practical pathways.

- Design defects: The issue sits in the product concept itself. A connected device may overheat because the design tolerances were poor. A household item may create foreseeable misuse risk because the form factor encourages the wrong handling.

- Manufacturing defects: The design may be sound, but a batch is assembled incorrectly, contaminated, or produced outside specification.

- Warning and instruction failures: The product may work as intended, but the packaging, insert, or on-product labelling doesn't explain safe use clearly enough.

For scaling brands, the third category is usually underestimated.

Why packaging and instructions matter more than people think

Across multiple marketplace ecosystems, one issue we repeatedly observe is that brands treat packaging as a marketing surface first and a risk-control document second. That can be expensive thinking.

If a consumer electronics accessory requires charging limits, environmental warnings or age guidance, those details aren't optional polish. They're part of the liability profile. The same is true for home organisation products, battery-based goods, wellness items and tools with obvious or foreseeable misuse patterns.

Weak labelling, missing warnings and inadequate instructions can open the same liability pathway as a physical defect.

That's why underwriters and serious retail buyers tend to care about traceability records, inserts, carton labelling and document control. Those materials tell them whether the brand understands where liability begins.

What the policy usually won't solve

Founders also need to be clear about the gaps.

A product liability policy is generally built around third-party bodily injury or property damage arising from a product sold, supplied or distributed into the market. It isn't a blanket answer to every commercial loss that follows a product problem.

Typical blind spots often include:

- Recall costs: Don't assume recall expenses sit automatically inside the policy.

- Channel disruption: Lost ranging, paused marketplace listings and buyer hesitation can outlast the insured event.

- Reputational damage: The policy may fund defence and covered liabilities, but it won't restore retailer confidence on its own.

- Internal operational cost: Reworking stock, retraining teams and fixing supplier controls often sit outside the cover question.

The practical lesson is simple. Product liability insurance matters, but it only works properly when founders understand both the insured event and the uninsured aftermath.

Meeting the Demands of Retailers and Marketplaces

Why do retail buyers and marketplace teams ask for your product liability certificate before they seriously discuss ranging, onboarding or cross-border expansion?

Because they are screening for supplier maturity, not just insurable risk.

If a retailer puts your product on shelf, or a marketplace lets you sell into its customer base, that channel carries exposure it did not create. The buyer's job is to reduce avoidable problems inside that channel. Insurance is one of the fastest ways they separate brands that are set up for scale from brands that may become expensive to manage later.

What buyers are really checking

Founders often treat insurance requests as procurement admin. That misses the commercial point. A buyer usually reads the policy documents as part of a broader question: can this supplier operate inside a serious retail environment without creating claims, delays, indemnity disputes or internal escalation?

The exact limit required will vary by channel, product category and market. In Australia, many larger retailers and distributors commonly expect product liability cover at a level that is meaningful enough to respond to a serious bodily injury or property damage claim. What matters in practice is less the number in isolation and more whether your policy matches the risk profile of the goods, the territories where they are sold and the counterparties asking to be protected.

A clean certificate of currency can signal several useful things at once:

- the business has gone through underwriting

- the declared products are consistent with the official catalogue

- the insured territories are not an afterthought

- documents can be produced quickly during vendor onboarding

- the brand is less likely to create uninsured disputes if a claim reaches the channel

That last point carries weight.

Retailers and marketplace operators do not want to discover, after an incident, that the supplier bought a low-cost policy built for a narrower product set or a single domestic market. I have seen promising listings stall at that point. The issue was not product demand. The issue was that the paperwork made the business look underprepared.

Insurance is part of your sales case

For scaling brands, product liability insurance should be configured as a market-access document.

It helps get procurement comfortable. It also shortens avoidable back-and-forth with legal, compliance and platform teams. That matters when a buyer is comparing several suppliers with similar pricing and product quality. The brand that can send clear policy evidence, confirm additional insured requirements if needed, and answer territory questions without confusion is easier to approve.

That is why the cheapest policy is often the most expensive commercial decision. A policy that saves a small premium but fails a retailer review can cost a ranging window, a seasonal launch, or a marketplace expansion cycle that takes months to reopen.

The questions worth asking before the buyer does

A better internal review sounds like this:

| Commercial question | Why the channel cares |

|---|---|

| Does the policy describe the products we actually sell today? | Buyers want the insured risk to match the live catalogue, not an old version of it |

| Do the covered territories match our sales plan? | A policy that works domestically may create friction once stock moves through overseas channels |

| Can we issue clean evidence of cover fast? | Procurement teams slow down when documents are inconsistent or incomplete |

| Do key counterparties need to be noted in the policy structure? | Some retailers, distributors and marketplaces ask for specific contractual treatment |

| Does the insurance sit alongside testing, traceability and brand protection records? | Buyers assess the full operating system, not the certificate in isolation |

For marketplace-led brands, this discipline often overlaps with platform readiness work such as Amazon Brand Registry requirements in Australia. Strong channels back suppliers that look organised across insurance, compliance and brand control, because those signals usually travel together.

Navigating Product Liability Across International Markets

Will your current policy still help the sale close once a US retailer, a UK distributor, or a cross-border marketplace asks legal to review it?

International expansion exposes a point many founders only discover mid-onboarding. Product liability insurance is not interpreted the same way across markets, and that matters long before any claim exists. The commercial question is whether your cover will satisfy procurement, legal and compliance teams in the market you want to enter.

The comparison that matters

In Australia, product liability is often arranged together with public liability, and many businesses treat that structure as normal. For domestic trading, it often is. For international growth, the issue is whether that policy format, territorial scope and wording line up with how overseas counterparties assess supplier risk.

That mismatch shows up in practical ways. A buyer may ask for local wording. A marketplace may want proof that the policy responds in the jurisdiction where the product is sold. A distributor may want additional insured treatment or a contract review before they accept your documents. None of those requests means your insurance is poor. They do mean your policy has to work commercially in that specific market, not just exist on paper.

Here is the high-level view founders should keep in front of them.

Global product liability insurance at a glance

| Factor | USA | Canada | United Kingdom | Australia |

|---|---|---|---|---|

| Legal culture | Claim activity and litigation pressure can be heavier in many categories | Provincial and federal considerations can complicate execution | Consumer protection expectations are established and documentation standards are strict | Statutory consumer protections under the ACL shape exposure |

| Buyer expectations | Large retailers and marketplaces often review wording, limits and certificates closely | Distributors may want local clarity on coverage and claims handling | Compliance records and policy consistency matter heavily | Combined public and product liability is common |

| Policy fit for exporters | Usually needs careful review before entry | Cross-border wording and supply chain structure matter | UK-facing documentation should match contracts and operating reality | Local brokers often structure cover around Australian trading conditions |

| Practical founder issue | Broad global assumptions often fail at procurement review | Territorial mismatch can delay onboarding | Poor instructions and inconsistent documents create friction quickly | Brands often underestimate how directly insurance affects channel access |

Why this changes your expansion sequence

I have seen international launches stall for reasons that looked commercial but proved structural. The retailer said legal had questions. The distributor said the insurance wording did not match the contract. The marketplace paused approval because the certificate did not clearly support the territory or operating model.

In each case, the brand had expanded catalogue availability before it had configured its risk position for the new market.

This gets sharper when fulfilment models change. Local warehousing, importer of record arrangements, white-label distribution, or post-sale service partners can shift where liability sits and who expects to be protected. A policy that worked well for domestic sales may need different territorial language, contract alignment, or insurer approval once stock and responsibility move across borders. That is why insurance review belongs inside broader supply chain risk management for international expansion, not as a document chase after commercial terms are agreed.

International expansion usually slows because documents, responsibilities and local expectations do not line up at the same time.

What good looks like

Strong operators review liability market by market before entering the channel. They check whether the policy matches the product category, countries of sale, distribution model, and contractual commitments in that market. They also prepare evidence of cover that a buyer or marketplace can use without having to interpret vague wording.

The commercial advantage is speed. If your insurance already fits the territory and the channel structure, procurement moves faster, legal asks fewer questions, and new market entry becomes easier to execute. “Covered somewhere” is a weak standard. “Accepted by the counterparties that control access” is the one that supports scale.

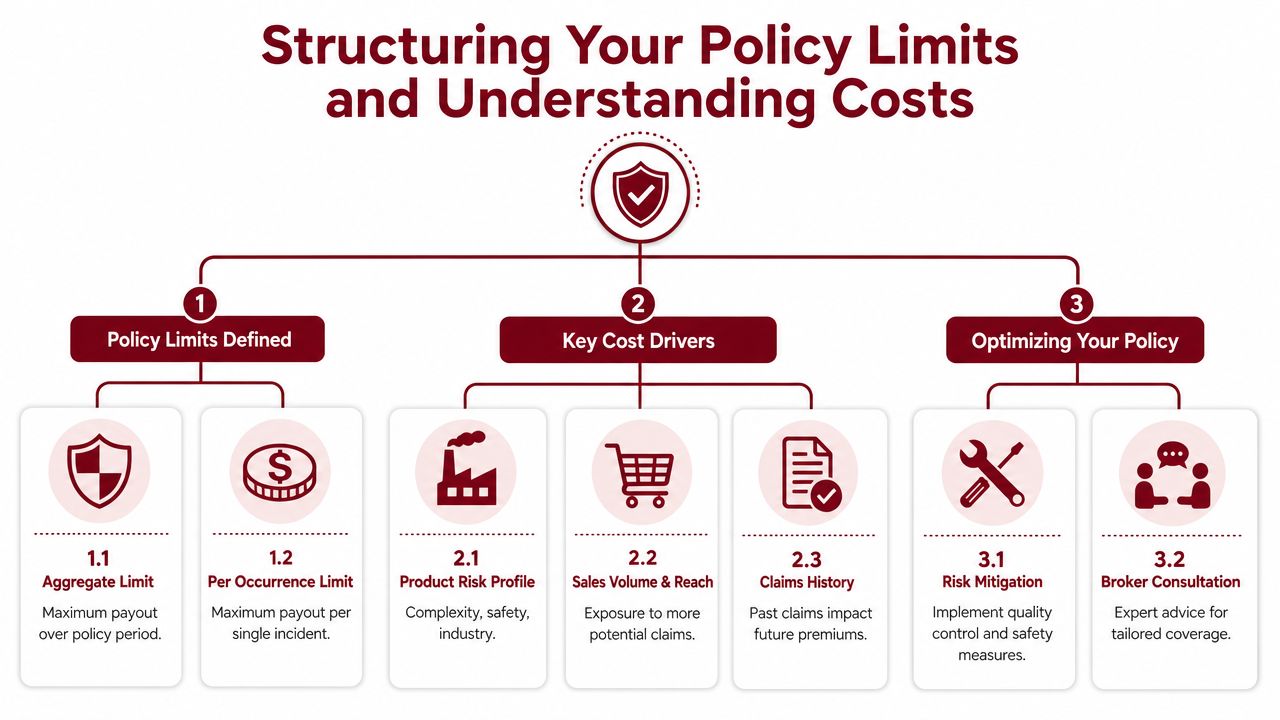

Structuring Your Policy Limits and Understanding Costs

Most founders don't need a lecture on insurance theory. They need a sensible framework for deciding how much cover is enough and why insurers price one business differently from another.

The key point is that limits and premiums aren't arbitrary. Underwriters look at exposure in a fairly commercial way. What do you sell, how much do you sell, where does it go, and where do you sit in the chain if something fails?

The two limit questions that actually matter

Industry guidance commonly references a minimum limit of about AUD 1 million per occurrence as a baseline, with AUD 5 million or more often recommended for higher-hazard or higher-volume product lines. That same guidance notes that premiums are driven by product risk profile, sales volume and the insured's role in the chain of distribution, as explained in this guide to product liability insurance limits and pricing.

Founders should separate two ideas:

- Per occurrence limit means the maximum available for a single incident or claim event.

- Annual aggregate limit means the maximum the policy will pay across the policy period.

A business selling a simple hand tool and a business selling battery-based consumer electronics may both hold cover, but the conversation around adequate limits won't be the same. Hazard profile changes the severity outlook. Sales volume changes the frequency outlook. Geographic reach changes how widely one issue can spread.

For a visual summary, this short video is a useful companion to the policy-structure discussion below.

What pushes premiums up or down

Underwriters usually respond to a mix of commercial facts and control signals.

| Cost driver | What the insurer is really assessing |

|---|---|

| Product risk profile | How severe a failure could be if the product malfunctions or is misused |

| Sales volume | How many units are in the market and how widely exposure is distributed |

| Supply-chain role | Whether you manufacture, import, distribute or simply private-label |

| Product complexity | How many failure points sit inside the design, materials or instructions |

A brand selling low-complexity household products usually presents a different risk picture from a brand selling products with batteries, moving parts or detailed usage instructions. That doesn't mean one is safe and the other is uninsurable. It means the underwriting conversation changes.

The founder mistake to avoid

The common mistake is choosing limits by instinct, or by copying what another brand says it has.

Commercial lens: The right limit is the one that matches your product risk, your channel ambitions and your ability to absorb a serious claim without destabilising the business.

A better process is to decide limits against the channels you want next, the countries you plan to serve, and the consequences of one claim spreading across multiple units or multiple retail partners.

Operational Controls That Strengthen Insurability

If you want better insurance outcomes, buying more cover isn't always the strongest move.

Operational discipline often matters more.

Product liability insurance does not automatically cover product recalls, and for Australian brands this matters because buyers increasingly expect evidence of traceability, compliance and incident-prevention controls before listing products. Stronger documentation, QC and recall planning can be more decisive than premium size in shaping both underwriting appetite and loss severity, as outlined in this explanation of what product liability insurance may not cover.

The documents that carry real weight

Underwriters and channel partners both respond to proof. Not promises.

The most persuasive file usually includes:

- Quality control records: Batch checks, inspection routines, supplier standards and non-conformance handling.

- Testing evidence: Internal and third-party validation that the product performs as represented.

- Traceability systems: The ability to identify where stock came from, where it went, and which units may be affected by a problem.

- Recall planning: A documented process for withdrawal, notification and containment if an issue appears in market.

- Warning and instruction controls: Version-controlled packaging, inserts and manuals that show the brand manages safety communication deliberately.

For product businesses operating across multiple channels, these controls aren't just technical paperwork. They support commercial confidence.

Why mature brands get better traction

One issue we repeatedly observe is that brands negotiate insurance like a price-only purchase while overlooking the operating habits that shape the quote in the first place.

A founder might push hard on premium, but if the business can't produce testing records, supplier qualification documents or stable warning-label controls, the insurer sees a management problem. So does a retailer.

Operations and growth stop being separate conversations. Better quality systems can improve underwriter confidence, reduce onboarding friction with buyers, and make a future claim easier to defend. That same discipline sits close to broader quality assurance standards for scaling product brands.

The policy is only one part of insurability. The rest sits in the way the business designs, documents and controls the product before it reaches the customer.

What works and what doesn't

What works is boring, repeatable control. Clean documentation, supplier oversight, current instructions, incident logs and a realistic recall process.

What doesn't work is relying on the existence of a policy to compensate for weak operating discipline. Insurers can price risk. They can't fix a disorganised product business.

A Founder's Checklist for Managing Coverage

Founders get the best value from product liability insurance when they manage it as a live commercial asset, not an annual renewal chore.

That means treating the policy, supporting documents and channel requirements as part of the same operating system. If one of those elements drifts out of date, the business usually discovers it at the worst possible moment, during a buyer review, a renewal negotiation or an incident.

The checklist serious brands actually use

- Review channel requirements annually: Retailers, distributors and marketplaces often have their own insurance expectations. Check them before renewal, not after a contract lands.

- Keep product descriptions accurate: Make sure the insurer understands what you sell, how it works and where it is distributed.

- Match policy geography to trading reality: If you're entering new countries or servicing new channels, confirm the policy still fits the actual footprint.

- Maintain a central documentation file: Store testing reports, QC records, artwork approvals, instructions, supplier files and incident logs in one accessible location.

- Track product changes carefully: New materials, new components, revised instructions or a factory move can all change the risk profile.

- Prepare for recall scenarios: Even if recall isn't automatically covered, your response capability still affects insurer confidence and buyer confidence.

- Brief internal teams: Operations, sales, customer service and compliance teams should know what to escalate and how quickly.

- Use a broker conversation properly: Don't turn the renewal meeting into a price-only discussion. Use it to test whether the policy still supports your growth plan.

The founder mindset that changes everything

The businesses that handle this well don't separate insurance from expansion strategy. They treat cover as part of market readiness.

That changes how decisions get made. Product development teams think harder about warnings and instructions. Commercial teams ask for buyer requirements earlier. Operations teams keep traceability cleaner because they know it supports both insurability and retailer trust.

Good coverage isn't static. It should evolve as the catalogue, channel mix and international footprint change.

The practical takeaway

If your brand is moving into larger retailers, cross-border distribution or premium marketplace ecosystems, product liability insurance belongs on the front end of planning.

Not because it looks responsible. Because it removes friction, supports credibility and helps serious channel partners say yes faster.

TPR Brands works with established product companies that need more than channel access alone. If you're preparing for international marketplace expansion, retailer onboarding, or a tighter commercial structure around product risk, TPR Brands helps brands build the operational and marketplace foundations that make growth credible across Australia, the US, Canada and the UK.