Sales can rise on Amazon Australia while margin steadily deteriorates underneath. Founders often blame the obvious line items first: referral fees, rising ad costs, returns, maybe a sharper wholesale cost than last year. Those things matter, but they usually aren't the primary reason profitability is slipping.

The deeper issue is ecosystem misalignment.

A brand can carry strong products, decent reviews, acceptable conversion, and still lose margin because it's operating with the wrong marketplace logic. That's especially common in Australia. Teams import assumptions from the US or UK, then wonder why the economics feel tighter, the catalogue needs more support, and paid visibility starts behaving like a tax instead of a growth lever.

One pattern we keep seeing is this: brands treat Amazon as a listing and advertising channel when it operates as a commercial environment with its own local behaviour. Search language, delivery expectations, returns friction, category maturity, and the physical realities of serving Australia all shape margin outcomes. If those pieces aren't aligned, every tactical improvement works harder for less reward.

That's why Amazon Australia expansion strategy needs to be approached as a market adaptation exercise, not a copy-paste of what worked elsewhere. The primary reason your margins are shrinking on Amazon usually isn't that Amazon suddenly became expensive. It's that your operating model hasn't adapted to the Australian version of the marketplace.

Introduction The Margin Paradox on Amazon Australia

The margin paradox is simple. Revenue looks healthy. Units are moving. The account feels active. Yet the profit line keeps tightening.

Most advice stops too early. It says margins are shrinking because fees went up or because PPC is more competitive. That explanation is convenient, but incomplete. If two brands face the same marketplace conditions and one preserves contribution margin while the other keeps leaking it, the problem isn't only the platform cost stack.

The wrong diagnosis creates the wrong fix

When founders diagnose margin pressure as a pure cost issue, they reach for tactical patches. They trim bids. They pause keywords. They push suppliers for better pricing. They tighten inventory. Sometimes those moves help, but often they just reduce visible spend while the structural problem stays in place.

The structural problem is usually a mismatch between how the brand is positioned and how the local marketplace functions.

In Australia, that mismatch shows up in practical ways:

- Imported keyword logic: Search terms from the US or UK get reused with minimal localisation, even when Australian shoppers use more pragmatic or category-specific language.

- Weak fulfilment alignment: The catalogue carries products that are operationally expensive to serve, but the pricing model still assumes healthier margin retention.

- Fragmented visibility strategy: Sponsored ads, listing copy, backend terms, and catalogue structure don't reinforce each other, so the brand pays more to maintain the same discoverability.

- Assortment sprawl: Too many SKUs are listed without a clear view of which ones can carry the commercial burden of the marketplace.

Practical rule: If your only explanation for shrinking margin is “Amazon fees”, you're probably measuring expenses more closely than market fit.

Margin pressure is usually a lagging indicator

By the time founders notice profit compression, the underlying issue has often been building for months. Search intent was misread. Conversion assumptions were borrowed from another region. Bulky or low-ticket products were allowed to absorb too much delivery and ad pressure. Listings were technically live but not commercially localised.

That's why The Primary Reason Your Margins Are Shrinking on Amazon rarely sits in one dashboard column. It sits in the interaction between fulfilment, localisation, assortment discipline, and paid visibility.

Amazon Australia still rewards strong operators. It just punishes generic playbooks faster than many brands expect.

The Anatomy of Margin Compression in Australia

Australia creates a specific kind of pressure on marketplace businesses. It isn't just Amazon. It's what Amazon sits inside: a geographically dispersed country, structurally mature ecommerce behaviour, and a marketplace that scaled fast enough to reset customer expectations before many brands built systems to support those expectations.

Amazon's local growth matters here. According to reporting on Amazon Australia's rapid scaling, Australian customers had access to more than 60 million products by 2019, and Amazon opened its first Australian fulfilment centre in September 2018. That combination matters because broader assortment and stronger fulfilment infrastructure change what buyers expect from the marketplace and what sellers need to fund to compete.

Fast marketplace growth changed the commercial baseline

A younger marketplace can look forgiving from the outside. Founders assume there's more room, lighter competition, and lower operational pressure than the US or UK. That's only partly true.

Australia didn't stay in a soft early-stage marketplace condition for long. A rapidly expanding product range and fulfilment footprint changed the baseline. Buyers learned to expect broad selection and more reliable delivery. Once those expectations settle in, sellers don't compete only on product quality. They compete on speed, price discipline, listing relevance, and trust signals across the whole offer.

That's where pricing power starts to weaken.

A strong product can still win, but it often wins with less room for error. If your listing under-converts, you pay for visibility. If your fulfilment setup is clumsy, you absorb the cost. If your competitors move faster on localisation, your traffic becomes more expensive to hold.

Geography doesn't care about your margin target

One issue we repeatedly observe is that brands model Amazon Australia as if the market's physical shape won't materially affect unit economics. It does.

Australia is logistically heavy. Distance matters. So does SKU shape, returnability, replenishment timing, and whether the product can carry fulfilment drag without forcing a pricing compromise. Hardware, home improvement, storage products, household goods, and practical consumer items often feel this more sharply because they can be bulky, awkward, or low-ticket relative to delivery burden.

That turns a catalogue problem into a margin problem.

Here's where operators usually get caught:

| Commercial area | What founders often assume | What actually happens |

|---|---|---|

| Catalogue expansion | More SKUs create more sales opportunities | More SKUs can create more low-margin complexity |

| Delivery expectations | Buyers will tolerate friction in exchange for selection | Buyers often default to the offer that feels easiest and fastest |

| Price positioning | Small pricing moves protect gross margin | Small price moves can reduce conversion and increase ad dependency |

| Returns handling | Returns are a customer service issue | Returns often reshape profitability at SKU level |

The pressure isn't theoretical. It shows up as products that sell but don't contribute enough.

Ecommerce maturity raised the floor on service expectations

Australia Post reported that 2023 online purchases reached 9% of total retail spend, with parcel volumes remaining structurally strong in the local market, as noted in this discussion of Australian ecommerce fulfilment conditions. That matters because Amazon sellers aren't operating in a market where online shopping is experimental or occasional. They're serving customers who are already conditioned to compare convenience, delivery reliability, and total purchase confidence.

Sellers often talk about fees as if fees are the margin problem. In practice, the margin problem is what sellers must spend to meet the market standard those fees sit inside.

This is why generic Amazon fees in Australia analysis often misses the point if it stays at the account level. Margin compression in Australia is usually cumulative. Referral fees matter. Fulfilment matters. Returns matter. Sponsored visibility matters. But serious damage happens when all of them converge on SKUs that were never structured to absorb that pressure in the first place.

The brands that struggle most usually share the same pattern

Not every catalogue is equally exposed. The products that tend to suffer most have some combination of these characteristics:

- Bulky physical profile: They cost more to move and create more fulfilment sensitivity.

- Low perceived differentiation: Buyers compare on price and convenience, not brand depth.

- Weak local search alignment: Traffic has to be bought because discovery isn't naturally strong.

- Slow stock movement: Storage and ad inefficiency linger for longer.

- Shallow margin buffer: There isn't enough room to absorb marketplace friction.

The lesson is blunt. Shrinking margin on Amazon Australia usually isn't the result of a single rising cost. It's the result of operating in a market with mature buyer expectations and demanding physical economics, while using a commercial model that was built for another environment.

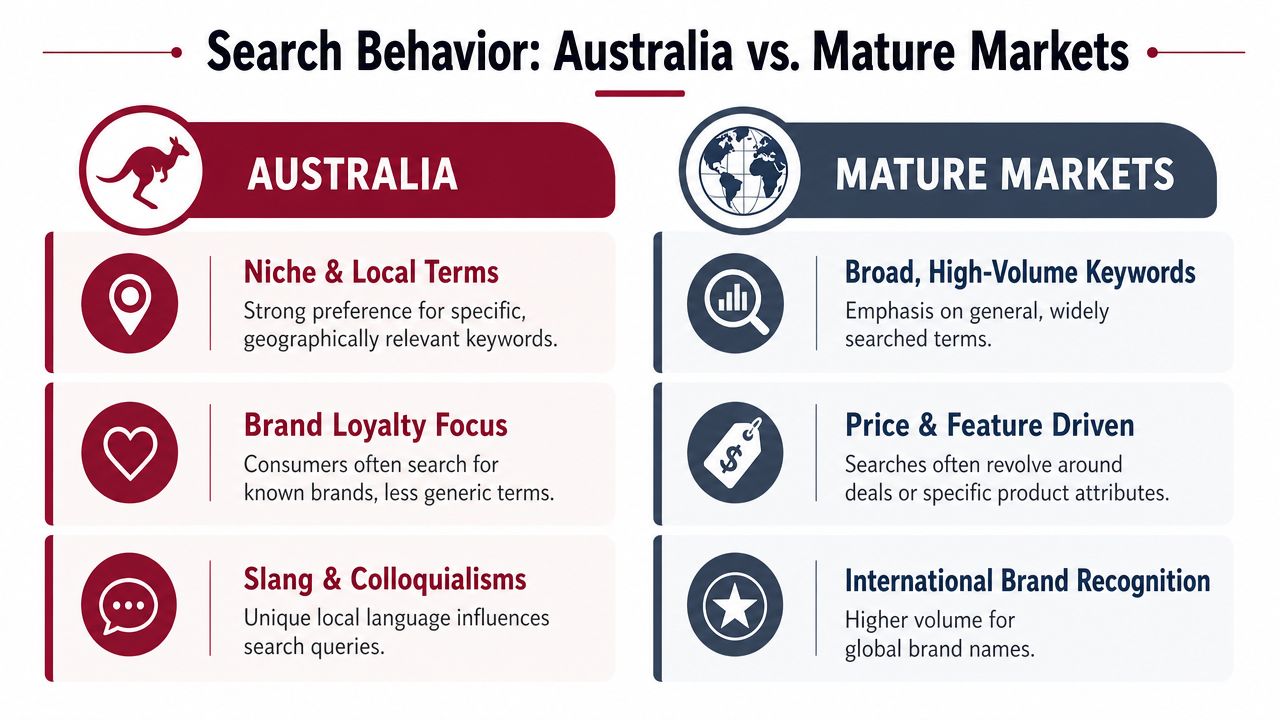

The Search Behaviour Gap Between AU and Mature Markets

The margin story gets more interesting when you look at search behaviour. It is through search behaviour that many international brands subtly lose efficiency before they even realise there's a problem.

A listing can be well written and still be wrong for the market. Not because the product is wrong, but because the language of discovery is wrong. In Australia, buyers often search with a more practical lens. They want the thing that solves the job. That sounds obvious, but the gap appears in how products are described, which terms feel natural, and what kind of intent sits behind the search.

What we see across practical product categories

In consumer electronics, home organisation, household tools, and lifestyle accessories, brands often import keyword structures from larger markets. The result is familiar: branded emphasis where local brand equity is still weak, feature language that feels slightly off, and listings that technically match the product but don't match the customer's search habit.

A connected device brand might lead heavily with ecosystem language and model naming because that works in a mature branded category elsewhere. In Australia, the shopper may search more directly for the use case, the compatibility issue, or the problem being solved.

A home storage product might arrive with polished US terminology, while local shoppers are using simpler, more functional wording. A wellness accessory might be listed with broad category language, while buyers are searching with highly specific practical intent.

The difference sounds small. Commercially, it isn't. If your relevance is weaker, paid traffic has to compensate.

Local language affects profit, not just ranking

This isn't only about spelling variations such as “organisation” versus “organization”, although that matters. It's also about the shape of intent.

Australian shoppers often compare more cautiously in categories where trust isn't already established. That means your listing needs to communicate utility quickly and cleanly. If the copy is over-branded, too abstract, or borrowed from another region's sales logic, conversion weakens. Once conversion weakens, margin gets hit from two directions: ad efficiency softens, and the listing needs more support to hold position.

As covered earlier, Australia is already a high-expectation ecommerce market. The fulfilment environment adds pressure because brands often absorb extra cost to protect conversion in categories with awkward unit economics. That context makes search relevance even more important, especially for practical products where buyers compare several similar options before choosing.

For founders working through marketplace localisation across regions, this is usually the moment the underlying issue becomes visible. The customer in Australia isn't just a translated version of the customer elsewhere. They browse differently, compare differently, and often reward a different balance of clarity, familiarity, and practical confidence.

A weak keyword strategy doesn't only lower discoverability. It forces the entire commercial system to work harder to produce the same sale.

Three common signs the search layer is misaligned

- You're visible, but the wrong searches are doing the work. Ads drive traffic, but organic discovery doesn't strengthen in a stable way.

- The listing sounds polished, but not local. It reads like centralised brand copy rather than market-native commerce language.

- Your best-selling SKUs don't match your most heavily supported SKUs. Spend is compensating for poor natural alignment.

When that happens, founders usually think the ad account is inefficient. Sometimes it is. But often the ad account is just revealing that the discovery language underneath hasn't been localised properly.

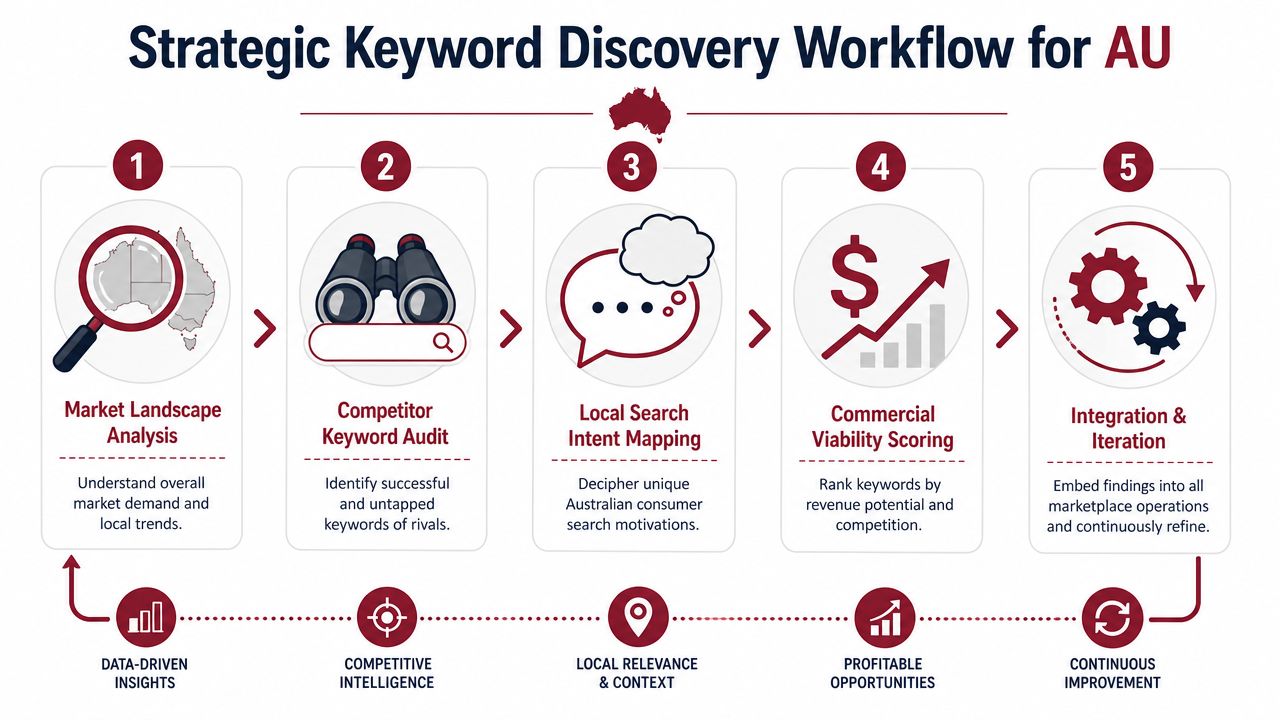

A Commercially Aware Keyword Discovery Workflow for AU

Keyword discovery in Australia shouldn't start inside a tool. It should start by questioning your assumptions about the market.

If the team begins with a spreadsheet exported from another region, the outcome is usually a localised version of the wrong answer. Stronger operators start with commercial intent. They ask how Australians describe the product, how the category is mentally organised, and which terms signal browsing versus buying.

Start with the catalogue, not the keyword tool

The first pass should happen SKU by SKU. Not every product deserves the same discovery strategy. Some products are search-native and easy to categorise. Others need educational framing or clearer utility language. Some attract broad discovery but poor economics. Others have narrower demand but better commercial resilience.

A useful workflow starts by sorting the catalogue into commercial groups:

- Margin carriers: Products that can tolerate ad support and fulfilment pressure.

- Traffic products: Products that attract attention but may not carry enough contribution margin on their own.

- Range support items: Products that strengthen the catalogue but shouldn't absorb aggressive spend.

- Misfit SKUs: Products that may belong on the marketplace but not in a serious growth plan.

That sort changes the quality of keyword discovery. You stop asking, “What terms get searched?” and start asking, “Which search opportunities are worth winning?”

Build seed language from how Australians buy

A practical seed list should come from four places at once.

First, take the product's plain-English use case. Not the brand story. Not the internal product name. The practical job it does.

Second, strip out imported terminology that sounds natural in the US or UK but less natural locally. This is common in organisation, accessories, connected devices, and household categories.

Third, map product attributes that matter at the point of comparison. Size, fit, compatibility, application, material, room type, installation method, and problem solved often matter more than polished category language.

Fourth, review how competing listings frame similar offers in Australia. Don't just lift terms. Look at how they organise meaning.

A strong local seed list usually includes a mix of:

- Functional terms: what the product does

- Attribute terms: what shape, size, material, or use condition matters

- Problem terms: what inconvenience or task the buyer wants solved

- Compatibility terms: what product, room, device, or environment it works with

- Category shortcuts: the plain language a buyer uses when they don't know the formal name

Field note: The best Australian keyword sets often sound less “marketing polished” and more practically useful.

A short visual summary helps when teams are aligning discovery with wider catalogue strategy.

Audit competitors as ecosystems

Most keyword research treats competitors as ranking pages. That's too narrow.

Look at them as marketplace ecosystems. How do they title products? Which product attributes are repeated across the catalogue? What kind of benefit language appears in images? Do sponsored placements align with listing language, or are they disconnected? Does the brand look locally adapted or globally templated?

This matters because keyword performance is rarely generated by copy alone. It emerges from the full listing environment.

A useful competitor review asks questions like these:

| Review area | What to look for |

|---|---|

| Title structure | Which product terms appear early, and which are delayed |

| Image language | Whether the visual story matches practical local use |

| Variation logic | Whether variations support discovery or create confusion |

| Review themes | Which use cases buyers repeatedly mention |

| Sponsored presence | Whether the same phrases keep appearing in paid placements |

When several competitors succeed with similar framing, there's usually a local logic behind it. When they all sound imported, there may be white space for a better adapted offer.

Validate with tools, then score commercially

Tools are useful later. They validate phrasing, reveal adjacent terms, and help compare variants. But they shouldn't decide the initial strategy.

Once the seed set is built, score keywords through a commercial lens:

Relevance to the exact ASIN

If the term lands traffic but mismatches the offer, it will create expensive noise.Intent quality

Some terms indicate problem awareness. Others indicate comparison or near-purchase behaviour.Margin compatibility

A keyword can be attractive and still be wrong if it forces support levels the SKU can't sustain.Local naturalness

If the phrase feels imported, conversion often tells you before reporting does.Catalogue role

The same keyword may be valuable for one SKU and distracting for another.

This is why a commercially aware workflow outperforms a purely technical one. It treats keyword discovery as a profitability decision, not a metadata exercise.

Translating Keyword Insights into Profitable Strategy

Keyword insight only becomes valuable when it changes operating decisions. Many brands do the discovery work, then lose the benefit because the insights never make it into the parts of the account that shape visibility and margin.

That disconnect is common. Backend search terms say one thing. Listing copy says another. PPC campaigns pursue a broader or different vocabulary again. The catalogue ends up competing against itself.

Backend data should reinforce, not improvise

If Australian keyword insight is real, it needs to appear in the backend, not just the ad account. That means backend search terms, title structure, bullets, attributes, and catalogue data should all reflect the same local discovery logic.

This sounds administrative, but it's commercial. Weak catalogue integrity creates margin leakage because the account spends money rediscovering relevance that clean data should already support.

A recent marketplace review pattern keeps appearing across hardware, household, and lifestyle ranges: the listing front end is partially localised, but backend fields still reflect imported naming logic. That creates a split signal. Amazon can index the product, but the account isn't giving the marketplace one coherent version of what the product is, how it should be found, and which use cases matter most.

PPC architecture has to follow market behaviour

Campaign structure should reflect how the market searches, not how the team likes to organise campaigns internally.

For many Australian accounts, a useful architecture separates search behaviour into layers such as brand, category, problem-solution, and competitor intent. But the weighting matters. In categories where local brand recognition is still developing, overspending on branded coverage can create a false sense of efficiency while the account underinvests in the practical discovery terms that grow reach.

That's where why Amazon ads spend without producing enough profit becomes a commercial question rather than a media-buying question. If your campaign architecture is disconnected from local search behaviour, the account buys traffic expensively, defends visibility inefficiently, and struggles to build lasting organic support.

A better structure usually includes:

- Brand defence campaigns: Important, but tightly controlled where brand demand is still modest.

- Category capture campaigns: Built around the plain-language terms local buyers use.

- Problem and application campaigns: Especially valuable for practical goods where buyers search by need.

- Competitor and comparison campaigns: Useful selectively, not as a default growth engine.

- Discovery campaigns: Designed to learn, then feed validated terms into cleaner manual structures.

Don't ask whether a keyword converts. Ask whether it converts at a contribution level that justifies keeping it.

Unit economics must sit at ASIN level

This is the point most founders miss. A keyword can work. A product can convert. Sales can rise. And the ASIN can still be commercially weak.

According to guidance on modelling Amazon seller fees and profit impact, the practical method is to model landed cost, referral fee, FBA or fulfilment cost, storage, and ad spend at the ASIN level, then test whether a 1 to 2% conversion-rate lift can offset fee drag on contribution margin. The same guidance notes that sellers who monitor this data weekly are the ones most likely to preserve profitability.

That's the discipline that separates activity from performance.

A workable decision table looks like this:

| If the ASIN shows this pattern | The likely issue | The commercial response |

|---|---|---|

| Good traffic, weak conversion | Listing or search intent mismatch | Tighten local language before scaling spend |

| Good conversion, poor margin | Fee and fulfilment drag too heavy | Reprice, repackage, or reduce support |

| Strong branded sales, weak category reach | Overdependence on existing demand | Expand practical non-brand discovery carefully |

| Stable ad sales, weak total contribution | Paid visibility is masking poor economics | Reassess whether the SKU belongs in scale plans |

What stronger brands do differently

They don't treat localisation, catalogue management, and paid search as separate tasks. They run them as one system.

They know which SKUs deserve aggressive visibility and which only deserve protective presence. They adapt campaign language to the market instead of forcing imported keyword sets. They use backend fields to reinforce relevance, not as an afterthought. And they keep reviewing unit economics often enough to catch deterioration before revenue growth hides it.

That's how keyword work protects margin. Not by increasing traffic in isolation, but by making every layer of marketplace presence more coherent.

Conclusion Building a Scalable and Margin-Aware AU Presence

Shrinking margin on Amazon Australia usually looks like a cost problem first. That's why so many brands chase the wrong fix.

They lower bids, trim budgets, pressure suppliers, and hope the account settles. Sometimes it stabilises briefly. But if the underlying marketplace strategy is out of step with Australian conditions, the pressure returns in another form. Conversion weakens. Visibility gets more expensive. Fulfilment drag keeps biting. The catalogue carries products that create sales without creating enough contribution.

That's why the reason your margins are shrinking on Amazon isn't usually hidden inside one fee line or one advertising report. It sits in the interaction between market maturity, geographic reality, and local search behaviour.

Australia demands adaptation. It's a geographically complex market with mature online expectations and a marketplace environment that scaled quickly enough to change customer standards fast. Brands that enter with imported assumptions often discover that the economics are tighter than expected, not because Amazon is unworkable, but because the operating model wasn't local enough.

The stronger response is more disciplined than dramatic.

What a healthier Australian marketplace presence looks like

A margin-aware Amazon Australia strategy usually has four characteristics:

- The catalogue is selective: Not every SKU is asked to scale. Products earn their role.

- Search language is local: Discovery reflects how Australian buyers describe and compare products.

- Paid media supports the right products: Ad structure follows commercial logic, not just platform convention.

- Unit economics are watched closely: ASIN-level profitability decides where to expand, defend, or pull back.

The brands that scale well in Australia usually stop treating the marketplace as a sales outlet and start treating it as an ecosystem that needs local commercial alignment.

That shift matters beyond Amazon. Once a brand learns to localise language, refine assortment, and model contribution properly, it becomes better prepared for broader international marketplace expansion as well. The discipline transfers.

Marketplace growth isn't a listing exercise. It's an ecosystem transition. Strong catalogues don't automatically become strong marketplace businesses, and rising sales don't automatically mean healthy expansion. The brands that build resilient margin are the ones that understand how local behaviour, fulfilment structure, and commercial positioning fit together.

If your margins are tightening, the answer usually isn't to spend less. It's to align better.

TPR Brands helps established product companies turn strong catalogues into commercially coherent marketplace ecosystems across Australia and international regions. If you're working through Amazon margin pressure, localisation challenges, or broader cross-market expansion decisions, TPR Brands is built for founder and operator conversations that go deeper than listings, ads, or surface-level channel management.