For many established Australian brands, Canada looks like the logical next step after domestic success. The market feels familiar, English-speaking, commercially stable, and easier to approach than a full US expansion.

That assumption causes expensive mistakes.

Canadian expansion through Amazon is not simply a smaller version of the US market. Brands quickly encounter different compliance standards, bilingual packaging requirements, regional buying behaviour, freight realities, and pricing pressures that can significantly affect profitability.

A capable Amazon agency should help brands do more than launch listings. The real job is building a profitable market-entry system that protects pricing, supports localisation, and creates long-term channel control across Amazon, retail, and direct-to-consumer sales.

For Australian brands with proven products, Canada can become an effective North American expansion market — but only when the operational structure is built correctly from the beginning.

Why Canada Is Not a Smaller US Market

Understanding the Canadian Market Opportunity

A Sydney brand can look well prepared on paper, then hit Canada and discover the offer does not travel cleanly. The hero SKU is right. The Amazon listing is live. Early traffic comes in. Then conversion splits by province, Quebec is harder than expected, and the positioning that felt clear in Australia suddenly reads as vague or too premium for the wrong audience.

That is a market-entry problem, not a traffic problem.

Founders often approach Canada with a US-adjacent mindset. That is one of the fastest ways to waste margin.

Canada has enough familiarity to create false confidence, but the commercial logic is different.

Regional behaviour shows up earlier, national scale is harder to earn, and Quebec alone can change packaging, creative, and channel decisions.

The first serious comparison is Canada versus your current Australian operating model. Australian brands are often used to selling into a relatively concentrated retail structure with a more unified national story. Canada asks for sharper segmentation. British Columbia can respond well to premium, outdoor, and lifestyle-led positioning. Ontario usually rewards clearer mainstream value communication. Quebec requires preparation at the brand level, not just a translation pass at the end.

A capable amazon agency should assess demand by region, margin structure, and adoption curve. Search volume matters, but it is only one input. The better question is whether the brand can earn repeat purchase and hold its pricing once freight, fulfilment, returns, and local competition start pressing on contribution margin.

Common Expansion Mistakes Australian Brands Make

What founders usually get wrong

The first mistake is assuming product-market fit survives the flight.

I have seen Australian household, wellness, and hardware brands arrive in Canada with a product that clearly works, but the buying trigger is off. The problem is rarely the core item. It is the framing. The Australian version of the story can rely on local familiarity, retailer credibility, or lifestyle cues that do not mean much in Toronto or Montreal. That forces changes in packaging hierarchy, listing copy, offer structure, and sometimes the hero variant itself.

The second mistake is reading Amazon demand without enough channel context. A product can convert on marketplace search because the need is obvious and the category is under-merchandised. That does not automatically mean the brand is ready for broader retail, distributor conversations, or sustained repeat purchase. Amazon can prove there is transaction potential. It does not prove the brand has translated.

The test is simple. Do Canadian customers understand the offer quickly, trust it enough to buy without heavy discounting, and come back at a margin that still works?

Where the Opportunity Sits

Canada is attractive for established Australian brands because it offers a controlled North American entry point. That does not mean easy. It means legible. The market is large enough to matter, developed enough to support premium positioning in the right categories, and structured enough to show whether your brand can travel before you absorb the full cost and complexity of a broad US rollout.

That is why disciplined operators use Canada to build capability, not just revenue.

Marketplace scale is part of the case, but the bigger opportunity sits in the quality of the test. Amazon Canada can tell you which regions adopt first, which claims create trust, whether your ASP holds, and how much localisation the brand really needs. Those are expensive lessons to learn in the US at full burn.

If you are already evaluating Amazon Canada as a deliberate expansion channel, tighten the questions before you commit inventory:

- Which provinces are likely to adopt first

- Does the category need bilingual packaging to scale nationally

- Will Amazon be a discovery channel, a core revenue channel, or both

- Can the margin survive freight, customs, local fulfilment, and returns

- Does the brand story still make sense when stripped of Australian context

Underserved does not always look empty

Founders often look for low competition and miss the better signal. In Canada, good openings are often found in categories where competitors exist but execute poorly.

That can mean weak creative, generic copy, poor bundle logic, thin review depth, or seasonality that has been handled with a US template instead of a Canadian one. Snow, heating cycles, outdoor use patterns, and regional climate differences affect real buying behaviour in ways many imported brands underestimate. The shelf may look occupied. The position can still be available.

Canada rewards brands with a clear commercial point of view. Clear relevance beats loud branding.

Navigating Canadian Regulatory and Customs Compliance

Packaging and Compliance Issues That Delay Launches

A brand can have clean creative, strong reviews in Australia, and a product that should travel well. Then the first Canadian shipment gets held because the importer setup is wrong, the classification is loose, or the packaging cannot support French requirements. That is how otherwise capable brands lose six months.

Canadian compliance shapes the entry model earlier than many Australian teams expect. We have seen Australian brands lose entire seasonal windows because packaging approvals, tariff classifications, or bilingual compliance work started too late. In most cases, the issue was not product quality. The issue was sequencing operational decisions after inventory planning had already begun.

It affects whether Amazon can launch on time, whether retail buyers will take the range seriously, and whether the unit economics still work after relabelling, brokerage, and storage.

Compliance is a Commercial Decision Made Early

I have seen brands treat Canada like a lighter version of the US. That assumption causes avoidable rework. Canada has its own product rules, tax settings, import processes, and language obligations. Quebec makes the mistake obvious, but the problem usually starts well before Quebec.

For wellness, beauty, pet, household, and hardware products, legal review should happen before inventory is booked. Claims, warnings, directions, ingredients, pack hierarchy, inserts, and carton labels all need review at the same time. If that work starts after the first purchase order, the launch plan is already under pressure.

A capable amazon agency should be able to work with customs brokers, regulatory advisers, and packaging teams. An agency that only wants to discuss ranking factors and ad structure is arriving after the strategic decisions have already been made.

Bilingual packaging changes the economics

French on pack is not a finishing touch. It changes the production plan.

It can reduce front-of-pack space, increase design complexity, lengthen approvals, and push up print costs if the existing format is already crowded. Products that rely on education are affected most. Supplements, technical household items, pet health products, and goods with safety instructions often need more than a simple translation pass. They need the whole communication hierarchy rebuilt so the pack still sells while meeting local requirements.

That is why channel sequencing matters. Some brands should open with Amazon and a narrower SKU mix while the national packaging system is being rebuilt. Others should delay the launch and fix the packaging architecture first. The right answer depends on margin, category risk, and how exposed the brand is to retail scrutiny.

Tip: If the team cannot explain who approves claims, who signs off on translation, and when the final print file is locked, inventory should not leave Australia.

Why Landed Cost Errors Become Expensive

Border friction usually appears in the P&L before it appears in Seller Central.

Australian founders often budget for freight and add a buffer. That is not enough. The landed cost model needs to include tariff treatment, brokerage, GST or HST exposure where relevant, local drayage, storage, returns handling, and the carrying cost of stock sitting in transit across the Pacific. Amazon then adds another layer of cost pressure through referral fees, FBA charges, and return exposure. Teams should model that early with a clear view of Amazon fee structures and fulfilment cost drivers.

A good customs broker does more than lodge documents. They help confirm tariff classification, review commercial invoices, catch origin errors, and flag missing product information before goods depart. That support is particularly useful for brands shipping mixed cartons, products with regulated claims, or ranges that were originally built for Australia rather than North America.

Delayed clearance creates second-order problems. Launch dates slip. Advertising gets turned on before stock is live. Review velocity slows. Retail buyers lose confidence if inbound timing keeps changing.

| Decision area | Weak approach | Better approach |

|---|---|---|

| Product classification | Assume the closest code is good enough | Confirm classification before the first commercial shipment |

| Packaging | Add French after the artwork is approved | Build bilingual hierarchy into the packaging system from the start |

| Import setup | Decide importer and tax responsibilities late | Set broker, importer, and tax ownership before launch |

| Channel rollout | Push Amazon, DTC, and retail live together | Sequence channels according to compliance readiness |

As noted earlier, marketplace infrastructure only helps after the regulatory basics are controlled. The same lesson applies across cross-border expansion. Brands that treat compliance casually spend more on rework, hold more dead stock, and lose negotiating power with every delayed launch.

For that reason, many brands benefit from running a local compliance workstream in parallel with channel setup. That can sit internally or with external legal and broker relationships. TPR Brands works with established consumer brands on market adaptation, compliance, and channel entry across Australia, Canada, the US, and the UK.

A useful primer for teams reviewing the broader import and listing process sits below.

What to lock down before inventory moves

- Claims review: On-pack language and listing copy need to match what the product can legally support in Canada.

- Instruction sets: Assembly, usage, safety, and care directions often create more translation and formatting work than expected.

- Broker review: Customs documents should be checked before departure, not while the goods are waiting at the border.

- Returns design: Reverse logistics needs an early decision because cross-Pacific returns can destroy contribution margin on lower-priced SKUs.

Brands that handle this work early do not enter the market slower. They enter with fewer avoidable costs and far more control.

Building a Profitable Channel and Pricing Architecture

Why Pricing Architecture Fails During Expansion

The fastest way to damage an Australian brand in Canada is to confuse market entry with channel presence. Being available is not the same as being profitable.

Amazon.ca can be a strong discovery engine. It can also become a margin trap if pricing, fulfilment, and wholesale strategy are built in the wrong order. The question is not whether Amazon belongs in the mix. The question is what role it should play.

Define Channel Role Before Platform Execution

Established brands entering Canada usually have four broad paths:

- Amazon first for discovery and early demand reading.

- DTC first if the brand already converts well through education, bundles, or community.

- Retail first where the category depends on physical presence and buyer trust.

- Hybrid entry where Amazon, DTC, and selected wholesale accounts support different jobs.

Most founders default to Amazon because it feels measurable. That is fair, but it often produces sloppy pricing architecture. If Amazon becomes the reference price before landed cost, retail margin requirements, and promo tolerance are mapped, every later channel conversation gets harder.

Build the Canadian P&L before setting the shelf price

Do not start with a desired retail price and reverse-engineer hope into the model.

Start with landed cost. Then test channel-specific economics. That means you model:

- Freight and inbound handling

- Customs and broker costs

- Marketplace or retailer fees

- Storage and fulfilment

- Returns and damaged stock

- Promo assumptions

- Working capital pressure from slower turns

The discipline here matters because even strong operators can lose margin through small, repeated misses. An extra packaging change, an underestimated return rate, or a retailer-funded promo can turn a healthy-looking launch into a channel you keep feeding without real profit.

For teams that want a sharper sense of fee pressure inside marketplace economics, this breakdown of Amazon fee structures and how they affect margin planning is useful context.

A practical way to decide channel order

Use this framework instead of chasing every channel at once.

| Channel | Best use | Main risk | When it works |

|---|---|---|---|

| Amazon.ca | Discovery, search capture, early review generation | Price anchoring and fee drag | The product solves a clear problem and can survive marketplace economics |

| DTC | Higher margin, richer education, bundle control | Traffic cost and slower trust-building | The brand story is strong enough to convert off-marketplace |

| Retail | Visibility and category legitimacy | Margin compression and chargebacks | The product fits existing retail buying behaviour |

| Distributor | Faster local reach | Less control over positioning | The brand needs on-the-ground sales coverage quickly |

Key takeaway: Amazon should typically sit inside the architecture, not become the architecture.

What works and what does not

What works is sequencing.

Launch on Amazon when you need efficient discovery, use DTC to capture more profitable repeat behaviour where the category allows it, and add wholesale when operational control is stable enough to support it. This protects pricing integrity because each channel has a defined purpose.

What does not work is setting one national price because it “feels clean” while ignoring the economics underneath. Canadian expansion often exposes brands that never built channel-specific contribution analysis in Australia because domestic complexity was easier to absorb.

There is useful marketplace evidence for why operators pay close attention to loyalty mechanics once a channel is established. Verified data shows that Amazon Prime in Australia reached over 2 million members by 2024, and Prime households spent 2.5 times more annually than non-Prime households, AUD 1,800 versus AUD 720, according to the verified summary citing Vocal’s Amazon timeline page. The lesson is not “copy Prime logic into Canada.” It is that channel economics improve when fulfilment, loyalty, and repeat purchase are designed together.

Margin protection rules for founders

- Do not underprice to force velocity: Early volume at the wrong price teaches the market the wrong value.

- Do not promise retail parity before modelling promos: Retailers and marketplaces create different cost realities.

- Do not ignore return economics: In bulky or fragile categories, returns can rewrite the channel decision.

- Do not treat Amazon ads as separate from pricing: If your ad spend is compensating for weak economics, the problem is structural.

A serious amazon agency earns its keep here by telling you when not to launch a product in a channel yet. That is often more valuable than optimising a listing that never had enough margin to begin with.

Localising Your Brand Beyond the Label

Most Australian brands stop localisation at translation. That is not enough.

Canadian buyers do not buy because the pack includes French. They buy because the brand feels relevant in their context. The label gets you legal access. Localisation earns trust.

Translation Alone Does Not Build Trust

A founder may have a product with strong domestic proof, polished creative, and clear category credibility. Then they put the same imagery, same references, and same product hierarchy into Canada and wonder why conversion stalls. The issue is rarely that the product is bad. It is that the brand is still speaking from home.

Seasonality is one obvious example. Australian creative often leans into brightness, outdoor ease, and summer-adjacent visual cues. In Canada, purchase intent can be shaped by winter routines, indoor use cases, cold-weather durability, or region-specific lifestyle patterns. If your listing and brand assets do not reflect that, the product can look imported in the wrong way.

The brand has to feel native enough to be trusted

Localisation usually needs work across four layers:

- Message hierarchy: What problem do Canadian buyers think they are solving first

- Creative cues: Do images, copy, and context look like they belong in-market

- Offer structure: Should you lead with singles, bundles, trial packs, or seasonal variants

- Partnerships: Who gives the brand local credibility when buyers see it for the first time

The partnership layer matters more than many founders expect. A Canadian distributor, retail rep group, local photographer, or category-specific creator can provide market intelligence that performance data alone will miss. They often know which claims trigger trust, which ones sound generic, and which parts of the offer need simplification.

Tip: If your launch assets still make sense only because the customer “gets the Australian reference”, they are not localised.

What bad localisation looks like

Bad localization is often subtle.

It shows up in product titles that technically describe the item but miss how Canadians search. It appears in comparison charts that highlight features local buyers do not prioritise. It appears in campaign timing that ignores local shopping rhythms. It also appears in reviews, where buyers signal confusion rather than dissatisfaction.

A strategic marketplace partner should be able to challenge your brand presentation, not just execute your existing assets. If the agency uploads what worked in Australia, it is acting like a listing service, not a strategic partner.

Positioning choices that travel better

The brands that adapt well often do three things:

First, they simplify their promise. International expansion is not the moment to become more clever in messaging.

Second, they choose proof carefully. Social proof that works in Australia may not carry the same weight in Canada. Retail placement, expert endorsements, installer trust, or use-case demonstration may land better than generic popularity claims.

Third, they localise without erasing the origin story. Australian provenance can still be an asset, especially in categories tied to quality, durability, outdoor performance, or formulation standards. But it should support the sale, not force the customer to decode it.

Localisation is where many brands either become export products or start becoming global brands. There is a difference. Export products ship. Global brands translate meaning.

Designing a Resilient Cross-Pacific Logistics Strategy

How Logistics Problems Quietly Destroy Margin

An Australian brand can get the first four decisions right in Canada and still lose the launch on freight, stock placement, and returns. I have seen brands spend months refining positioning and compliance, then hand the whole outcome to a shipping plan built for domestic replenishment. Canada punishes that mistake quickly.

The problem is not getting one container or one air shipment across the Pacific. The problem is building an operating model that still works when customs takes longer than expected, Amazon changes receiving times, a retailer asks for fill-in stock, or winter weather slows final-mile delivery.

The fulfilment model shapes margin and customer experience

Australian brands usually start with three options.

The first is direct shipping from Australia. That can work for low-volume market testing or high-margin products with patient buyers. It usually fails once delivery expectations rise, return requests increase, or customer acquisition costs assume a local service standard.

The second is a Canadian 3PL. That gives the brand a base inside the market, better control over DTC orders, retail replenishment, and local returns. It also creates a management job. Inventory reconciliation, service-level monitoring, carton configuration, and inbound booking discipline all start to matter a lot more.

The third is FBA for Amazon orders. That improves delivery speed and often helps conversion. It also concentrates too much power in one channel if every unit sits inside Amazon’s network.

That concentration risk gets missed all the time. Brands assume Canada works like a smaller version of the US, so they let Amazon become the whole operating system. Then a wholesale opportunity appears, DTC starts gaining traction, or returns require local inspection, and there is no inventory flexibility left.

A blended model usually gives established brands better control

For most established Australian brands, the practical answer is a split structure.

Use FBA for Amazon demand where Prime speed affects conversion. Use a Canadian 3PL for DTC, retail support, and returns processing. Keep direct-from-Australia fulfilment for edge cases, oversized products, or controlled early testing, not as the core customer promise.

Each node has a distinct role:

- FBA supports marketplace speed and service expectations.

- Canadian 3PL supports channel flexibility and cleaner reverse logistics.

- Origin inventory discipline protects cash and reduces expensive panic replenishment.

Teams building that model usually benefit from a clearer logistics strategy for multi-market brand expansion before they start allocating stock.

Inventory mistakes are rarely isolated

Founders talk about stockouts because they are visible. The more expensive mistake is often stock that arrives in the wrong place, at the wrong time, with too much cash tied up in it.

Canada stretches the replenishment cycle. In practice, this usually becomes visible when brands underestimate how difficult it is to correct inventory mistakes across the Pacific. A forecasting error that feels manageable domestically can take months to unwind once freight, customs clearance, and regional stock allocation are involved.

Transit times are longer. Recovery options are fewer. Forecasting errors take longer to fix. If demand runs ahead of plan, the solution is not a quick domestic transfer. If demand runs behind plan, aged inventory starts eroding margin while storage fees and discount pressure build.

That changes how inventory should be set up from day one. Safety stock belongs to the channel with the highest service expectation. Buffer stock belongs where it can be reallocated. Launch quantities should reflect the cost of being wrong, not just the ambition of the sales target.

Cross-Pacific planning has to account for seasonality and geography

Canada adds another layer that Australian teams often underestimate. The market is national, but operations are not uniform. Delivery performance into Ontario is not the same as Western Canada. Winter disruption is real. French-language packaging or inserts can affect where and when inventory is usable. A single inbound plan for the whole country often looks efficient on paper and creates friction in practice.

This matters more in categories with installation complexity, breakage risk, or sizing confusion. In those categories, every logistics decision touches support costs, review quality, and repeat purchase rates.

Returns Strategy Needs Early Planning

A weak returns path tells Canadian customers the brand is still operating like an exporter rather than a market participant.

Returns need a local destination, clear customer instructions, and a predefined decision tree. Can the unit be restocked? Does it need inspection? Is refurbishment economic in Canada, or is disposal cheaper? Those choices should be made before launch, not after the first spike in return requests.

Returns data is operational intelligence. It shows where packaging failed, where product education was unclear, and where channel fit was overestimated. Brands that treat reverse logistics as a side process usually end up paying for the same mistake three times. Once in freight, once in refund cost, and once in damaged trust.

A resilient logistics system is not elegant. It is prepared. It assumes delays will happen, stock will need to move, and customers will judge the brand by how quickly problems get resolved.

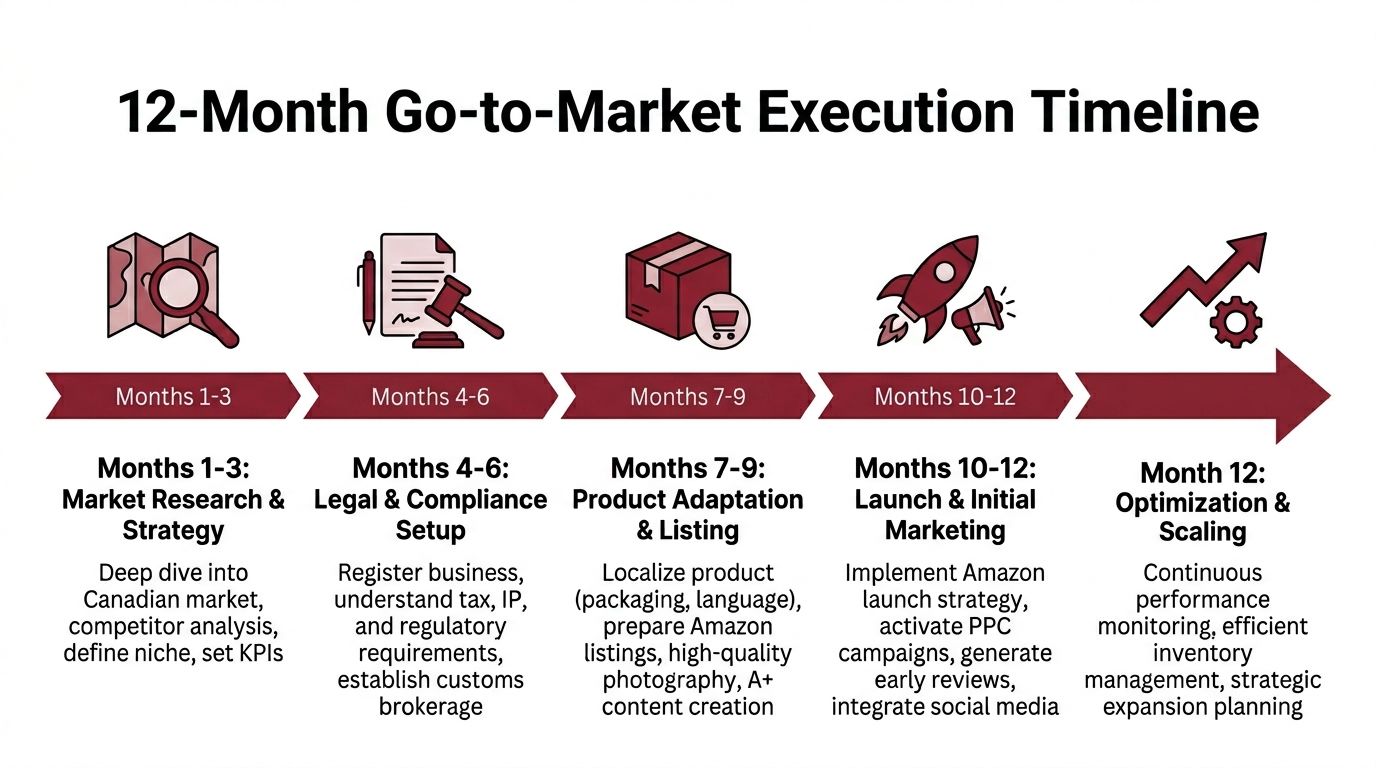

The 12-Month Go-to-Market Execution Timeline

An Australian brand lands its first Canadian inventory, turns on Amazon ads, and sees early sales in Ontario. Two weeks later, the problems start. Packaging approved for one channel does not hold up in another. Quebec is still unresolved. Margin looks healthy until landed costs, returns, and marketplace fees are counted properly. The issue is rarely effort. It is sequence.

Canada rewards brands that stage entry in the right order. Brands that treat it like a lighter version of the US usually spend the first year correcting decisions they made in the first quarter.

Months 1 to 3

Start by testing market fit in commercial terms.

Look at demand by province, channel role, and customer context, not just national search volume or broad category growth. A product that sells cleanly in Australia can still struggle in Canada if the value proposition depends on education, climate assumptions, or claims language that needs revision. This is also the phase to review importer structure, packaging implications, and whether Quebec belongs in phase one.

The first decision is blunt. Are you entering Canada with the current product, or with an adapted version that fits the market?

That choice affects everything that follows.

Months 4 to 6

Build the operating model before the launch calendar starts dictating decisions.

Set the pricing architecture, tax treatment, brokerage setup, bilingual packaging path, and channel hierarchy. Decide whether Amazon is the lead channel, a validation channel, or one part of a wider launch across DTC and retail. Brands that avoid this choice in the name of flexibility usually end up with channel conflict, inconsistent pricing, and margin pressure that was built in from day one.

This is also where experienced teams cut SKUs. The full Australian range rarely deserves a full Canadian launch. Fewer SKUs usually means cleaner forecasting, fewer compliance variables, and better working capital control.

Months 7 to 9

Prepare assets that match the Canadian buyer, not the Australian head office view of the buyer.

That means listings, imagery, A+ content, inserts, and wholesale material built for Canadian expectations and channel economics. If Amazon is part of the entry plan, listing language, review generation, ad structure, and pack claims need to align early. If retail is part of the plan, buyers need a margin story and a market story, not a recycled export deck.

Partner selection belongs here too. Translators, 3PLs, creators, rep groups, and photographers all shape how local the brand feels once the product is live.

Months 10 to 12

Launch with a narrow set of proof points.

Track contribution margin by channel, review quality, return reasons, customer support themes, and forecast accuracy. Those measures show whether the model works in Canada or whether sales are masking structural problems. Early traction can be misleading if it comes from discounting, uneven ad efficiency, or inventory that only sells in one region.

I have seen brands mistake a strong first 30 days for market validation, then discover the economics only worked because they undercounted localisation costs or delayed channel-specific packaging decisions. First-year discipline matters more than launch-week momentum.

Profit usually comes from sequencing. It rarely comes from trying to prove every hypothesis at once.

Ongoing from month 12

Scale after the system holds under pressure.

Expand range, inventory depth, or channel exposure only when the economics stay intact, the compliance process is repeatable, and the supply chain can absorb variability without creating service problems. Canada is large enough to punish rushed scale and nuanced enough to reward patient scale.

A useful way to govern year one is to review decisions in four buckets:

- Market signals: Which segments, provinces, and use cases are showing real adoption

- Economic signals: Which channels preserve contribution margin after all costs are included

- Operational signals: Where stock flow, service levels, or returns are creating avoidable friction

- Brand signals: Whether customers are building trust, not just completing a first purchase

A serious amazon agency should help leadership interpret those signals and decide what to change next. Reporting alone is not strategy.

Why Established Brands Work With an Amazon Expansion Partner

Most established brands do not fail in Canada because demand is weak. They struggle because too many operational decisions happen in isolation.

Marketplace setup, packaging compliance, landed cost planning, channel sequencing, and logistics design all affect each other. When those decisions are made separately, brands often create avoidable margin pressure long before scale begins.

An experienced Amazon expansion partner helps leadership evaluate the full commercial system before inventory moves. That includes market positioning, fulfilment structure, pricing architecture, localisation requirements, and long-term channel strategy across Amazon, retail, and direct channels.

For Australian brands entering Canada, the objective is not simply to launch products. The objective is to build a scalable North American operating model that protects brand value while creating profitable growth.

Frequently Asked Questions About Expanding into Canada Through Amazon

Conclusion Turning a Great Product Into a Global Brand

Is Canada a good first international market for Australian brands?

Canada can be an effective first North American expansion market because it offers strong consumer purchasing power, a developed ecommerce environment, and lower operational complexity than a full US rollout. However, brands still need to manage bilingual packaging, logistics, and regional market differences carefully.

Do Australian products need French packaging in Canada?

Many categories sold nationally in Canada require bilingual English and French packaging, particularly when products enter Quebec or include regulated claims, instructions, or safety information.

Should brands launch on Amazon Canada or retail first?

That depends on the category, margin structure, and customer buying behaviour. Many established brands use Amazon Canada first to validate demand and refine localisation before expanding into wholesale or retail channels.

If your brand is preparing for Canadian expansion, the biggest risks usually appear before the first sale happens. Pricing structure, compliance preparation, localisation, logistics planning, and channel sequencing all determine Amazon becomes a profitable growth engine or an expensive operational problem.

TPR Brands helps established Australian brands expand into Canada through structured Amazon growth strategy, localisation planning, market-entry architecture, and multi-channel expansion support across Amazon, retail, and direct channels.

For brands ready to scale internationally, Canada can become more than a test market. It can become the foundation for sustainable North American growth.