Founders usually search for top selling items on Etsy expecting a category list. Jewellery. Wall art. Wedding items. Digital downloads. That list is easy to find, and on its own it's not especially useful.

The harder question is whether Etsy is a viable channel for an established brand with existing margins, supply chain constraints, product standards, and brand equity to protect. For that audience, bestseller lists are not a buying guide. They're a demand map. If you read them properly, they show where buyers want personalisation, where gifting intent is strongest, and where niche demand is organised enough to support repeatable sales rather than one-off novelty.

Why 'Top Selling Items on Etsy' Is the Wrong Question

A lot of established brands make one of two mistakes with Etsy.

The first is dismissal. They treat it as a hobby marketplace and assume it has little relevance for serious product companies. The second is imitation. They search for top selling items on Etsy, copy the broad category list, and assume that entering the same category creates opportunity.

Both approaches miss what Etsy is good for.

Etsy signals buyer behaviour, not just product popularity

If you're running a hardware, household, lifestyle, or consumer brand, the strategic value of Etsy isn't limited to direct sales. It sits in the platform's unusually clear expression of buyer intent around identity, gifting, and customisation.

That matters because Etsy demand tends to cluster around products that are:

- Visually legible: A buyer can understand the product quickly from imagery alone.

- Emotionally specific: The item feels personal, commemorative, or gift-worthy.

- Low-risk to purchase: The buyer doesn't need to worry much about fit, sizing, or technical compatibility.

- Easy to adapt: The seller can offer names, dates, colours, materials, or minor variants without rebuilding the entire catalogue.

That combination is why broad bestseller lists can be misleading. The category name isn't the insight. The purchase logic is.

A founder looking at Etsy through a normal retail lens often asks, “What sells most?” A better question is, “What type of product behaviour does Etsy repeatedly reward?”

Etsy rarely rewards catalogue breadth in the way a mass retail marketplace does. It rewards relevance, clarity, and product-market fit within very specific buying moments.

Broad category wins don't tell you where your brand fits

One pattern we continue seeing across marketplaces is that brands overestimate the value of category labels. “Home décor” is too broad. “Personalised gift” is too broad. Even “jewellery” tells you almost nothing operationally.

What matters is the shape of demand inside the category. Which sub-niches are stable? Which products convert because they solve a known gift occasion? Which items can be produced consistently without introducing fulfilment friction or support burden?

That's why marketplace operators pay attention to how demand concentrates. In most ecosystems, value doesn't distribute evenly. A small share of subcategories, product formats, and keyword clusters absorb a disproportionate amount of demand. The same logic sits behind power law behaviour in marketplace demand.

If you're evaluating Etsy seriously, don't start with “what's top selling?”. Start with what Etsy buyers repeatedly trust, search for, and purchase with low hesitation. That's the signal worth studying, whether you intend to sell there now or use it to guide channel expansion.

Beyond Bestsellers Decoding Etsy's Real Demand Signals

“Bestseller” on Etsy is an output, not a strategy.

What founders need to understand is that Etsy doesn't publish exact sales counts at the listing level in the way many people wish it did. So the visible layer of demand has to be interpreted through marketplace signals rather than raw reported sales.

What the visible signals actually tell you

For AU-focused sellers, Etsy's “Most popular” ranking and bestseller badges operate as a demand-signal layer above exact sales counts, which Etsy doesn't disclose. Operationally, the most reliable approach is to look at category-level ranking, bestseller badge frequency, and review recency together, then validate with Marketplace Insights to separate search demand from actual sell-through in Australia, as outlined in this guide to seeing top-selling items on Etsy.

That distinction matters because not every highly searched item is commercially attractive, and not every badge reflects durable category strength. Some products catch temporary attention. Others sit inside stable buying behaviour.

The signals worth reading together

Looking at one signal in isolation creates false confidence. Reading them in combination gives you something closer to commercial reality.

| Signal | What it shows | What it misses |

|---|---|---|

| Bestseller badge | Strong visible momentum in a specific listing | Doesn't explain whether momentum is seasonal, durable, or margin-positive |

| Search ranking | Etsy is matching the product closely to shopper intent | Ranking alone doesn't prove sell-through |

| Review recency | Orders are still happening now, not just historically | Reviews lag behind sales and vary by category |

| Category concentration | Where multiple similar listings are repeatedly performing | Can still hide oversaturation |

A serious operator usually wants to know three things:

Is the demand search-led or ad-led?

Search-led demand is often more durable because buyers arrive with intent.Is the product structurally easy to buy?

Products with low decision friction tend to convert more cleanly.Can the demand be served without catalogue sprawl?

If yes, the channel may work even for brands that don't want to build a huge Etsy assortment.

Durable demand usually looks boring before it looks exciting

The highest-velocity Etsy segments are repeatedly identified as jewellery, home and living, and digital products in the source above. But the practical lesson isn't to rush into those categories blindly. It's to understand why they keep resurfacing.

They often combine a few characteristics:

- Clear use case: gift, occasion, décor, remembrance, self-expression

- Simple visual communication: buyers understand the offer instantly

- Customisable edges: names, dates, finishes, wording, files, formats

- Minimal post-purchase risk: fewer returns and fewer fit issues

That's why marketplace interpretation matters more than category copying. A strong catalogue placed into the wrong marketplace logic won't perform well. The same issue shows up across channels, especially when brands confuse product depth with ecosystem fit, which is why catalogue strategy and marketplace ecosystem design need to be treated as separate decisions.

A bestseller badge tells you where demand surfaced. It doesn't tell you whether your brand can serve that demand profitably, credibly, or at scale.

An Operator's View on Etsy's Category Maturity

One issue we repeatedly observe is that brands treat all Etsy demand as equally accessible. It isn't.

Some Etsy categories are mature in the sense that buyer demand is obvious, purchase behaviour is well established, and the leading offer formats are already standardised. Other pockets of the marketplace are less settled. Demand exists, but the offer architecture is still messy. That's where stronger operators can often enter more intelligently.

Mature categories bring demand and pressure

Personalised jewellery is the obvious example. Buyers understand it immediately. Gifting occasions are constant. The product is compact, visual, and easy to customise. The downside is equally obvious. Competition is dense, creative formats are familiar, and differentiation gets pushed into branding, materials, turnaround time, and presentation.

The same logic appears in other proven Etsy segments. Wall art converts because it photographs well and works through visual discovery. Digital products remove physical fulfilment friction. Personalised gifts sit close to known occasions, so buyer intent arrives pre-formed.

These are attractive categories. They're also unforgiving if a brand enters with no operational edge.

Less mature niches often suit established brands better

Across multiple marketplace ecosystems, we keep seeing a useful pattern. Established brands tend to perform better when they don't attack the broad headline category directly. They do better when they find a subcategory where product quality, fulfilment discipline, and controlled personalisation create a cleaner offer than what most smaller sellers can sustain.

That could mean:

- Specialised home organisation: Products that solve a real household use case and can be personalised lightly

- Accessory-led hardware: Branded add-ons, storage pieces, labelled sets, or engraved components

- Premium household gifting: Practical products reframed as commemorative or occasion-based purchases

- Pet-adjacent utility products: Functional items with a personal or decorative layer

The strongest Etsy entry point for many established brands isn't their hero SKU. It's an adapted product that fits Etsy's buying logic better than their core retail assortment does.

Why low-variance personalisation matters

In Australia, Etsy's strongest commercial opportunity isn't one single product type but high-intent, low-variance personalisation. Australian Marketplace Insights data and Etsy's own merchandising behaviour favour items that can be customised at checkout and shipped with minimal fit risk, such as jewellery, wall art, digital downloads, and personalised gifts. These categories convert through search-led discovery rather than deep assortment, allowing sellers to scale with a narrower SKU set and lower inventory complexity than apparel or size-dependent goods, as noted in this Australian Etsy category analysis.

For established brands, that's a useful filter.

A product doesn't need to become handmade theatre to work on Etsy. It needs to fit the marketplace's purchase mechanics. If a product can be personalised without introducing sizing complexity, compatibility confusion, or high return risk, it has a better chance of behaving like an Etsy-native offer.

That's why some hardware and home brands in fact have more Etsy potential than they assume. Engraved fixtures, labelled storage, customised gift sets, commemorative utility items, and accessory bundles often align more naturally with Etsy than broader, more technical SKUs.

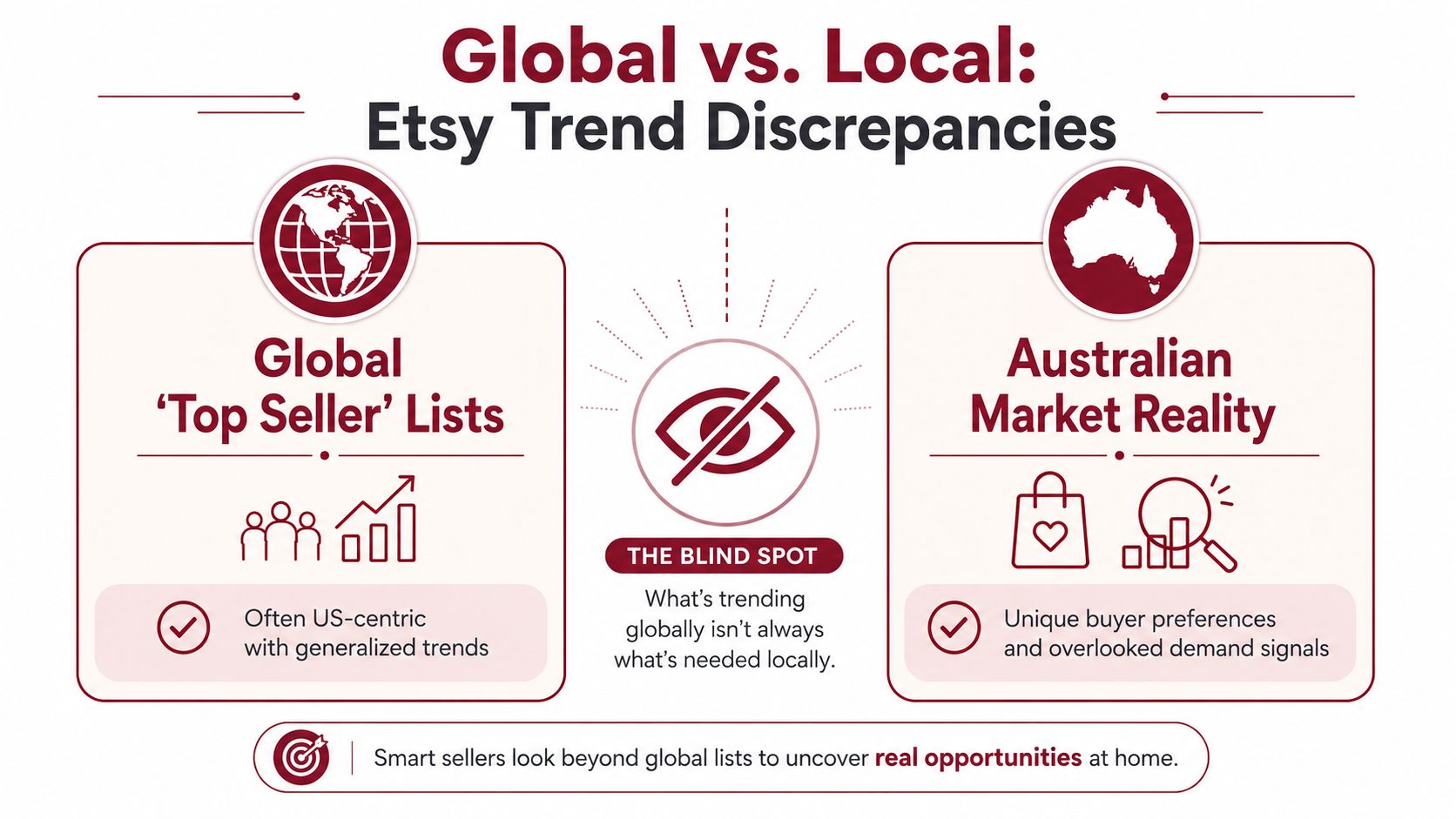

The Australian Blind Spot in Global Etsy Trend Lists

What does a global Etsy bestseller list tell an Australian brand deciding whether Etsy is a serious channel?

Usually, less than it appears.

Lists of top selling items on Etsy are often built for content reach, not channel evaluation. They flatten demand into broad labels such as jewellery, home décor, wedding products, and digital downloads. That framing is fine for hobby sellers looking for ideas. It is weak guidance for an established brand that has to protect margin, handle tax correctly, and decide whether Australia can support a repeatable operating model.

Global category lists flatten local commercial reality

The actual gap is local market context. Generic Etsy trend roundups rarely show how demand, competition, fulfilment economics, and buyer expectations change once the seller is operating from Australia. A category can look attractive at headline level and still be a poor fit after shipping times, GST treatment, return risk, and service burden are added. That matters on Etsy because demand sits in narrow, intent-heavy niches, not just in the broad category labels that show up in trend articles, as discussed in this review of Etsy selling opportunities.

A US-led list may show demand for a product family. It does not answer the harder questions. Can an Australian seller deliver it fast enough? Does the landed cost still work? Will local buyers read the offer as relevant, trustworthy, and worth the wait if the customer is offshore?

Those are operator questions, and they change the decision.

What changes when you localise the analysis

Once Etsy is treated as a market-entry question rather than a product-idea exercise, the screen becomes tighter:

| Global trend question | Australian operator question |

|---|---|

| Is this category popular? | Can we serve this category from Australia without eroding margin? |

| Are buyers searching for it? | Are Australian buyers searching for the same variant, wording, and use case? |

| Is the niche growing? | Is the niche fragmented, crowded, or awkward to fulfil locally? |

| Can we launch quickly? | Can we launch without adding tax, fulfilment, or support complexity? |

Generic advice assumes demand travels cleanly across borders. It usually does not.

I see this in marketplace expansion work repeatedly. The same product can feel local and low-risk in one market, then feel distant and uncertain in another because shipping confidence, delivery expectations, and category norms are different. The logic behind that gap is similar to what sits behind why some products feel closer than others in marketplace localisation.

A broad global trend can be commercially meaningless if the local fulfilment model, tax structure, or buyer expectation does not support it.

Australia is large enough to analyse properly

Some brands still treat Etsy in Australia as too minor to deserve structured analysis. That is the blind spot.

Buyer adoption in Australia is strong enough that Etsy should be assessed as a real channel, not dismissed on the basis of US-centric trend content. The practical implication is not that every Etsy category is attractive. It is that Australian brands need a local reading of demand, competition, and fulfilment viability before they borrow conclusions from global bestseller lists.

Once that shift happens, the question improves. The issue is no longer whether Etsy has popular products. The issue is which demand pockets an Australian brand can serve credibly, profitably, and at a service level that matches buyer expectations.

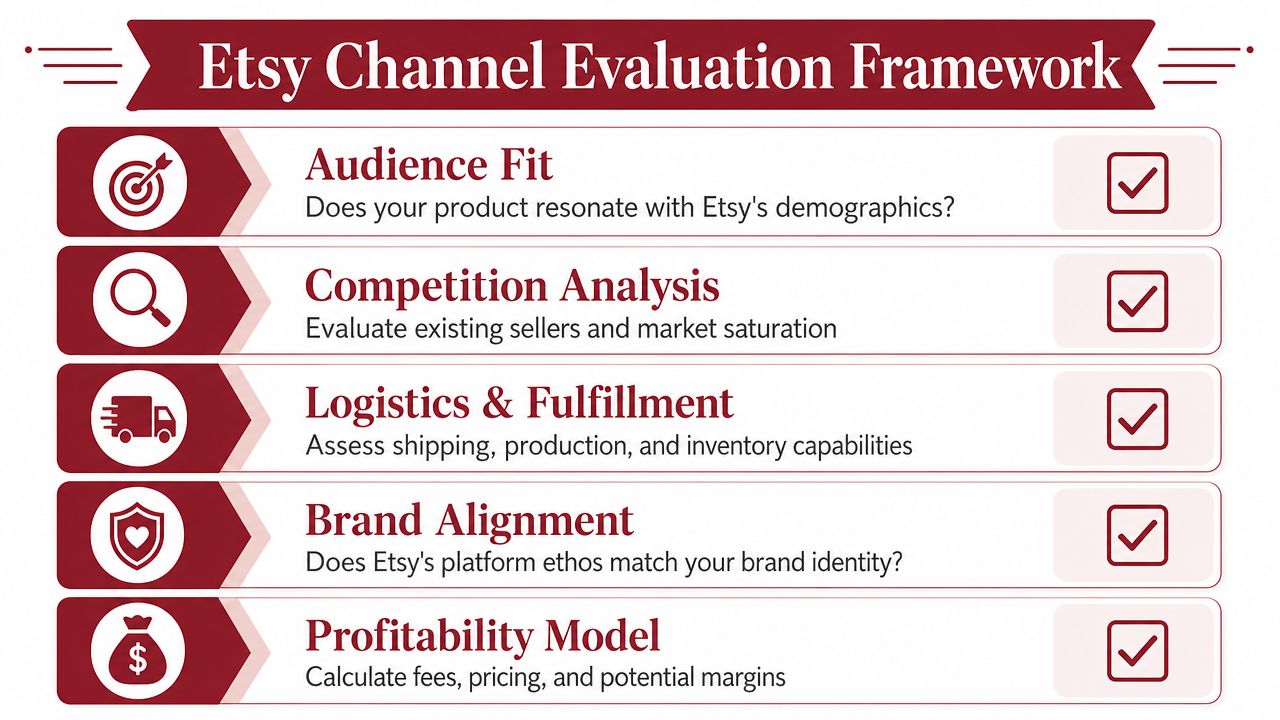

A Framework for Evaluating Etsy as a Brand Channel

What should an established brand test before treating Etsy as a viable channel in Australia?

The answer is not product popularity alone. Etsy works best when demand pattern, fulfilment model, and brand role line up at the same time. That is a tighter filter than the usual marketplace shortlist, and it is why many capable brands still misread the channel.

For Australian operators, the practical question is straightforward. Can this marketplace support profitable, low-friction entry for a specific slice of the catalogue, or will it force the business into expensive exceptions?

Product-to-ecosystem fit

A good retail product is not automatically a good Etsy product. I have seen technically sound items underperform because the purchase logic was wrong for the environment. Buyers on Etsy often decide fast, compare visually, and respond to occasion, story, and specificity more than broad assortment depth.

The first screen is behavioural fit. Assess whether the product naturally supports one or more of these signals:

- Giftability: The item maps to a clear occasion, recipient, or emotional use case.

- Personalisation potential: The buyer can shape the product without creating avoidable fulfilment risk.

- Visual clarity: The listing can communicate value quickly through images.

- Search alignment: Buyers are likely to search for the product in plain, consumer language.

If a product needs heavy education, long-form technical comparison, or sales assistance before conversion, Etsy is usually a weak first channel for it.

Operational readiness

Established brands often miscalculate margin.

A product that ships efficiently through retail, wholesale, or distributor channels can become awkward once it moves into one-unit orders, custom inputs, and buyer messaging. The issue is not complexity in theory. The issue is whether the operating model absorbs that complexity without eroding contribution.

A realistic readiness check covers four points:

- Small-order pick and pack

- Variant accuracy at order level

- Fast handling of personalisation inputs

- Consistent packaging at low unit volume

Teams built around case flow and replenishment often underestimate the service burden here.

Here's a useful discussion point on channel design and fulfilment assumptions:

Brand cohesion and commercial viability

Etsy should have a defined job inside the channel mix. Without that, the assortment drifts. Brands start uploading leftovers, copying retail range architecture, or chasing volume in offers that do not suit the platform.

A stronger approach is to test whether Etsy can hold a distinct commercial role, such as discovery, gifting, limited-run variants, or controlled personalisation. That keeps channel conflict lower and gives the team a clearer margin model.

| Evaluation area | Strong sign | Warning sign |

|---|---|---|

| Brand alignment | Etsy assortment feels additive and distinct | Listings dilute premium positioning |

| Range structure | Focused offer with clear purchase logic | Too many SKUs copied from retail |

| Margin logic | Unit economics still work after fulfilment complexity | High-touch orders destroy contribution |

| Channel role | Etsy serves discovery, gifting, or personalised demand | Etsy becomes a dumping ground for excess stock |

A simple rule helps here. If Etsy only works when you weaken pricing discipline, accept operational friction, or blur the brand, the channel is failing the test.

This is also why marketplace assessment should be framed as channel design, not just ecommerce expansion. The unit of sale changes. Buyer expectations change. Fulfilment economics change. That broader distinction sits at the centre of why marketplaces often operate more like distribution channels than pure sales channels.

Adapting Your Product for an Ecosystem Entry

If you decide Etsy is worth testing, the next mistake is to upload your existing catalogue and hope the marketplace sorts itself out.

It won't.

Etsy rewards adapted offers, not untouched retail transplants. That's especially true for established brands with products designed for broader retail environments rather than niche discovery and gifting behaviour.

What adaptation usually looks like

For a hardware or household brand, entry often works better through selective reformulation of the offer:

- Gift-led bundles: Combine a core item with an accessory, presentation upgrade, or occasion-led use case.

- Personalised variants: Add engraving, labelling, naming, or commemorative detail where it can be operationally controlled.

- Accessory-first entry: Launch with add-ons or complementary pieces that carry less technical risk than the core product.

- Marketplace-specific packaging: Present the item in a way that fits Etsy's visual and gifting expectations without distorting the main brand.

This is not about pretending to be a craft seller. It's about recognising that every marketplace has its own purchase grammar.

What usually doesn't work

The weakest Etsy launches from established brands tend to look familiar.

They copy wholesale assortment structure. They bring in products with too many decision variables. They force technical products into a marketplace built around emotional and visual buying cues. Or they try to compete on breadth when the channel rewards focus.

A narrower launch usually performs better because it allows the brand to answer a more precise question: Which part of our product DNA belongs in this ecosystem?

That's the strategic value of studying top selling items on Etsy properly. Not to copy them, but to identify the conditions under which demand becomes predictable, serviceable, and brand-compatible.

If that alignment exists, Etsy can become more than a side channel. It can serve as a useful entry point into personalised demand, gifting-led commerce, and localised international marketplace expansion. If that alignment doesn't exist, the right decision may be to learn from the marketplace without forcing a launch.

TPR Brands helps established product companies assess exactly that kind of channel decision. If your team is weighing Etsy, Amazon, retail marketplaces, or international expansion more broadly, TPR Brands brings operator-led guidance around localisation, channel fit, fulfilment structure, and brand-safe growth.