Amazon product discoverability affects certain categories far more than many brands realise.

Some products sell because customers already know exactly what they want. Others sell because the surrounding environment helps customers suddenly recognise a problem they had stopped noticing.

That distinction matters enormously on Amazon. Because certain product ecosystems depend heavily on contextual discovery, visual merchandising, adjacent problem-solving, and behavioural expansion.

And marketplaces do not naturally recreate those conditions well.

One pattern we continue seeing is brands with real offline traction entering Amazon as if they’re extending retail distribution, when they are entering a different commercial system with different rules.

The product may be proven. The category may be mature. The brand may already be trusted by buyers, distributors, and store networks. Yet the Amazon result still looks weak.

That disconnect is why so many otherwise successful retail products struggle once they enter Amazon. It’s a channel architecture question. In many cases, the product isn’t failing. The operating model is.

Retail Environments Create Contextual Discovery

Retail environments naturally help connected household systems behave like ecosystems.

Customers walk through aisles, compare adjacent products, recognise frustrations visually, and often discover solutions they were not intentionally searching for.

One stupidly simple moment in my kitchen captured this surprisingly well.

A spaghetti packet fell out of the pantry and exploded across the floor.

Mildly annoying? Absolutely.

But the interesting part came afterwards.

While looking through organisational ecosystems recently, I suddenly found myself mentally reorganising the entire pantry.

Not just the spaghetti.

Everything.

Spices. Containers. Shelves. Wraps. Turntables.

Storage systems I didn’t even know I wanted five minutes earlier.

At one point I was almost salivating over pantry organisation.

“I must get a container for the spaghetti… wait… look at that lazy susan for the pantry.”

That may actually be one of the most interesting parts of behavioural ecosystems.

The friction already existed. It had existed for years.

It had simply become normal.

The ecosystem didn’t create the frustration. It reactivated awareness around it.

And once that awareness starts, behavioural expansion can accelerate surprisingly quickly across adjacent categories.

That behavioural expansion is one of the most commercially interesting aspects of modular product ecosystems.

Behavioural Ecosystems Often Lose Momentum on Amazon

Amazon is exceptional at helping customers find products they already know they want.

But behavioural ecosystems often depend on something completely different. They depend on adjacent discovery.

A customer searching for a spice organiser may never naturally discover:

- pantry systems

- fridge organisation

- modular turntables

- drawer systems

- cabinet organisation

- under-sink ecosystems

Even though those products are behaviourally connected.

That is where ecosystem leakage begins. Retail environments naturally support this type of expansion far more effectively through:

- contextual discovery

- physical adjacency

- visual merchandising

- behavioural inspiration

Amazon often separates products that were originally designed to work together psychologically.

Anyone who has walked through IKEA has experienced this behavioural effect in real time.

You may enter looking for one shelf.

An hour later, you’re mentally redesigning the living room, replacing storage systems, buying lighting, reorganising wardrobes, and suddenly convinced your entire house needs solving.

The physical environment creates behavioural expansion naturally.

Online, that effect becomes much harder to recreate unless the ecosystem itself is intentionally engineered for discovery.

A strong organisational ecosystem may still contain excellent products, strong reviews, and healthy demand, while simultaneously losing behavioural expansion momentum because customers are only entering isolated parts of the ecosystem instead of discovering the broader system naturally.

That behavioural expansion is one of the most commercially interesting aspects of modular product ecosystems.

The Offline Winner’s Paradox on Amazon

A founder will often say some version of the same thing: we sell strongly through retail, trade, or distribution, so why is Amazon so underwhelming? The assumption behind that question is understandable. If a product already has market acceptance, Amazon should become another demand capture point.

It doesn’t work that way.

Amazon has to be treated as a separate channel architecture. Seller guidance is clear on the operational basics: offline distribution strength doesn’t transfer unless you engineer search relevance, Prime-competitive fulfilment, and product-page conversion together, with exact-match keyword coverage, localised images and copy, and FBA or a Prime-equivalent fulfilment path to avoid losing the Buy Box on speed alone, as outlined in SellerLogic’s Amazon selling analysis.

Proven offline doesn’t mean visible online

In physical retail, products can win through placement, staff recommendation, packaging presence, distributor relationships, and habitual replenishment. On Amazon, none of those advantages matter unless they translate into search visibility and conversion on the product page.

A hardware or household SKU that performs well in Walmart, Lowe’s , or independent trade channels may have earned that success through in-store context. The customer can compare weight, finish, fit, or perceived quality in person. On Amazon, that same SKU has to earn the click without a shelf, explain itself without a staff member, and convert without a sales rep.

Practical rule: If the product depends on in-store explanation to justify its price or quality, Amazon will expose that weakness quickly.

That’s why a strong offline catalogue can still look oddly fragile online. The issue usually isn’t demand in the broad sense. It’s that demand on Amazon is filtered through ranking, fulfilment speed, and page-level persuasion.

A related issue sits underneath this. Many strong products are introduced to Amazon with the same assumptions that weakened them online in the first place. Teams port packaging language, hero images, and channel positioning directly across without adapting for marketplace behaviour. That’s also why so many otherwise capable brands run into the same wall described in why great products fail to become great brands online.

The real tension founders need to address

The offline winner’s paradox is simple. A product can be commercially validated and still be structurally misaligned with Amazon.

That matters because the fix isn’t “do more Amazon”. The fix is to decide whether the brand is willing to build a marketplace-native version of its commercial model. Until that happens, offline strength keeps creating false confidence, and Amazon keeps producing disappointing evidence.

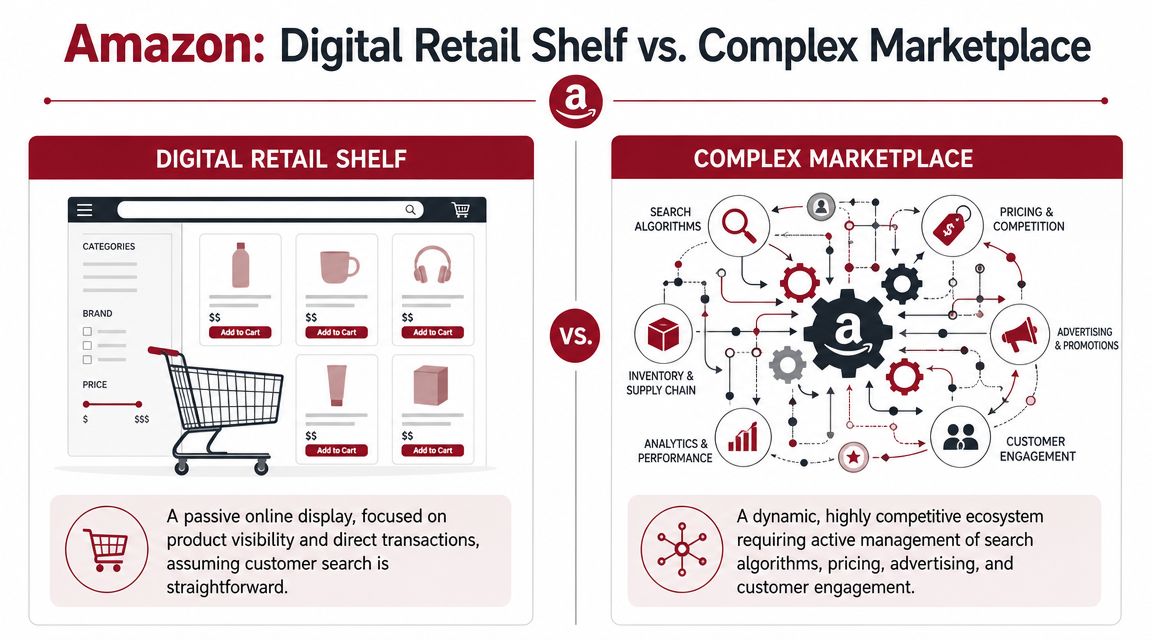

Why Amazon Is Not a Digital Retail Shelf

The easiest way to misunderstand Amazon is to treat it like a digital shelf. That framing suggests a fairly simple job: upload the catalogue, present the brand well, and capture incremental sales. In practice, Amazon behaves less like a shelf and more like a live commercial battleground.

Amazon’s own data states that over 60% of sales in its store come from independent sellers, which means brands are entering an environment where multiple sellers can compete on the same product page, altering pricing, visibility, and control from the outset, as noted on Amazon’s seller statistics page.

Shelf logic versus marketplace logic

Retail shelf logic rewards distribution access. Marketplace logic rewards buyability.

That distinction is more than semantics. In traditional retail, a brand works to secure placement, manage relationships, control merchandising standards, and support sell-through. On Amazon, those advantages are diluted because the listing is only one part of the equation. The offer, fulfilment method, seller performance, pricing discipline, content quality, and algorithmic relevance all affect whether the customer sees and buys the product.

A founder who is used to winning through brand presence can find this very frustrating. The same product page can become a shared asset. The same ASIN can host competition. The same branded item can slide into price comparison behaviour faster than expected.

In some cases, the brand itself is not even controlling the strongest customer experience anymore.

We’ve repeatedly seen established brands with multiple sellers competing on the same listings, creating inconsistent pricing, slower fulfilment, fragmented inventory quality, and uneven customer experiences.

A product that once felt premium in retail can suddenly appear unstable online simply because:

- one seller is Fulfilled by Merchant with slower shipping

- another is discounting aggressively

- another barely maintains inventory

- and poor review management starts damaging trust over time

The frustrating part is that the product itself often isn’t the real issue.

The marketplace structure surrounding it is.

Why control feels weaker on Amazon

One issue we repeatedly observe is that established brands assume brand equity will carry more weight on Amazon than it does. It helps, but it doesn’t govern the environment.

Amazon is closer to a contested distribution system than a branded showroom. That’s why Amazon isn’t a sales channel, it’s a distribution channel is the more useful strategic frame. Once a founder sees the platform that way, a lot of otherwise confusing behaviour starts making sense.

Consider the contrast below.

| Environment | What drives performance | What weakens performance |

|---|---|---|

| Traditional retail | Placement, rep relationships, merchandising, distributor support | Poor in-store visibility, weak retailer support, bad shelf position |

| Amazon marketplace | Search ranking, offer competitiveness, fulfilment speed, listing conversion | Shared listing pressure, slower delivery, weak indexing, fragmented pricing |

Amazon doesn’t ask whether a product is respected in the trade. It asks whether the offer is competitive right now, on this page, for this search.

This is the strategic mistake behind many weak launches. The brand hasn’t entered a digital shelf. It has entered a marketplace with different physics.

Four Commercial Disconnects That Erode Growth

When offline leaders struggle on Amazon, the pattern usually isn’t random. The failure tends to show up across a small set of commercial disconnects that compound each other.

Amazon sits inside a much larger competitive system. A 2025 marketplace roundup reported 9.7 million sellers worldwide, and that 57% of Amazon sellers reported profit margins above 10%, reinforcing that success depends on tight control of marketplace economics rather than simple distribution access, according to Analyzer’s Amazon statistics roundup.

Behavioural disconnect

Offline discovery and Amazon discovery are not the same commercial event.

In-store, buyers often encounter products passively. They notice packaging. They compare finishes. They ask staff. They purchase because the product is present at the right moment. Amazon compresses all of that into search, thumbnail judgement, and page conversion. If the SKU isn’t aligned to actual search behaviour, it can be commercially invisible despite strong offline sell-through.

This is especially common with products named for trade familiarity or shelf logic rather than customer search language. The brand knows what the item is. The buyer types something else.

Logistical disconnect

Founders often underestimate how much fulfilment structure affects perceived competitiveness.

A product can be correctly priced and well presented, then still lose because the delivery promise is weaker than nearby alternatives. If a competitor is Prime-competitive and your offer isn’t, the difference isn’t cosmetic. It affects click confidence, Buy Box position, and conversion quality. On Amazon, logistics aren’t downstream from marketing. They’re part of the product.

Operational observation: In marketplace reviews, fulfilment friction often looks like a demand problem until you compare the offer side by side with faster competitors.

Commercial disconnect

Offline channel success often masks fragmented pricing and margin leakage.

A brand may have grown through distributors, resellers, trade accounts, and retail partners with pricing that made sense in each environment. Amazon exposes every inconsistency. The result is often a product page where the brand is no longer selling on value, but reacting to marketplace tension it didn’t fully control.

That matters because Amazon competition is immediate and visible. Even where the brand owns the listing, it may not control the commercial narrative if unauthorised or poorly managed sellers are shaping price expectations in real time. This is one reason why your product isn’t selling on Amazon even though it should be is often a pricing architecture problem disguised as a content problem.

Data disconnect

Retail reporting and marketplace reporting answer different questions.

Offline, teams often think in terms of account growth, wholesale movement, repeat orders, and store penetration. Amazon forces a more granular view. Each ASIN has its own economics, its own visibility profile, and its own operational liabilities. A catalogue can look healthy in aggregate while several core SKUs are structurally weak at the unit level.

Here are four signs that this disconnect is already costing you:

- Strong brand, weak ASINs: Individual listings get traffic but don’t convert consistently.

- Good revenue, poor control: Sales exist, but margin quality and seller discipline are unstable.

- Catalogue depth, poor discoverability: Many SKUs are live, but only a small subset is visible.

- Retail confidence, slow reaction speed: Teams assume the product should work and delay structural fixes.

Why these disconnects compound

These gaps rarely appear one at a time. A non-search-native SKU often also has weak content. A weak content asset often sits inside a fragmented price environment. A fragmented offer often also lacks fulfilment competitiveness. Once those layers stack up, Amazon starts producing misleading signals.

The founder then sees mediocre performance and assumes the channel may be weak for the brand. In many cases, the channel isn’t weak. The operating model is misbuilt.

Adopting a Marketplace-Native Commercial Model

The brands that recover from this don’t usually do it by tweaking the listing in isolation. They change the way the business thinks about Amazon.

That means moving from a retail-extension mindset to a marketplace-native commercial model. The difference is substantial. Instead of treating Amazon as a place to mirror the existing channel, the brand treats it as a separate operating environment with its own compliance demands, margin logic, fulfilment requirements, and performance cadence.

Seller guidance for Amazon operators stresses that pre-launch work matters: validate ASIN eligibility, compliance, and profitability after all costs, including landed cost, referral and FBA fees, and return rates, because buyability depends on listing health and compliance more than offline brand recognition, as explained in Seller Assistant’s review of why brands fail on Amazon.

What a stronger model looks like

A marketplace-native model usually includes three shifts.

First, the brand stops evaluating Amazon at catalogue level and starts evaluating it at SKU and ASIN level. Some products deserve the channel. Some don’t. Some need repackaging, assortment simplification, or a different fulfilment structure before they’re commercially viable.

Second, the business builds a channel-specific P&L. That sounds obvious, but plenty of teams still approach Amazon margin using assumptions borrowed from wholesale or distributor economics. Amazon exposes every soft assumption.

Third, the brand designs around buyability, not just presence. That includes seller control, fulfilment path, content architecture, and the practical question of whether the offer deserves to win.

What doesn’t work

These approaches usually fail:

- Uploading the full catalogue immediately: More listings rarely fix weak channel fit.

- Using retail assets unchanged: Shelf packaging and trade language often underperform in search-led environments.

- Treating fees as an afterthought: Amazon economics need to be validated before inventory commitment.

- Letting channel conflict remain unresolved: If pricing and seller control are unstable, the listing quality won’t save the model.

The path to Amazon performance is often less about optimisation and more about re-architecting how the channel is run.

For brands making that shift, how to expand your product to Amazon without losing control is the right operating question. TPR Brands is one option in that category of support, particularly for brands that need help with marketplace transition, account structure, and controlled channel expansion rather than isolated tactical fixes.

A Prioritised Action Plan for Marketplace Realignment

Founders don’t need another generic Amazon checklist. They need an order of operations. If the sequence is wrong, teams often spend money on traffic before fixing the reasons traffic won’t convert.

The more useful approach is diagnostic first, corrective second.

Start with what the SKU is actually saying

Before changing campaigns or adding more content, inspect the ASIN as if the product has never existed in retail. What does the title communicate to a search-led buyer? Do the images explain the product without a store environment? Does the variation structure make sense, or does it create confusion? Is the page answering the buyer’s core hesitation quickly?

Many strong retail SKUs fail on Amazon because they were built for shelf presence rather than keywords. The more strategic question is how to re-engineer a proven offline SKU for Amazon without diluting brand equity, using search term alignment, content localisation, and assortment simplification, as discussed in this Australian marketplace video analysis.

Use a marketplace health triage, not a task list

The first pass should look like this:

| Area to Investigate | Negative Indicator (What to Look For) | First Corrective Action |

|---|---|---|

| Search relevance | Listing language reflects internal product naming more than customer search intent | Rework titles, bullets, and attributes around search-native wording |

| Fulfilment structure | Offer is slower or less competitive than adjacent alternatives | Review FBA or Prime-competitive fulfilment options |

| Seller control | Price inconsistency or multiple sellers weaken the commercial position | Audit seller landscape and reset channel governance |

| Product page clarity | Buyers can reach the page but key value points remain unclear | Rebuild imagery and copy around immediate buyer questions |

| Assortment logic | Too many variants or poorly grouped options create friction | Simplify range architecture for Amazon behaviour |

| Compliance and eligibility | Suppression, restrictions, or unresolved ASIN issues slow launch quality | Validate listing health and compliance before scaling spend |

Then act in this order

-

Fix channel foundations

Resolve compliance, seller control, fulfilment structure, and listing health first. If those are unstable, the rest becomes expensive noise. -

Rebuild discovery assets

Localise language for AU search behaviour. Tighten titles, attributes, and images around intent, not internal naming conventions. -

Reduce commercial leakage

Review pricing discipline, variation complexity, and assortment sprawl. Amazon punishes catalogue mess more quickly than retail does. -

Escalate structural issues early

If the problem involves multi-market rollout, reseller conflict, or channel redesign, bring in an operator who can look at the full ecosystem rather than just the Amazon account.

A lot of Amazon underperformance is diagnosed too late because teams treat it as a marketing issue after it has already become a commercial systems issue.

Beyond a Single Channel: From Realignment to Expansion

Once a founder sees Amazon clearly, a broader lesson usually follows. Marketplace expansion isn’t a listing exercise. It’s an ecosystem transition.

That matters beyond Amazon AU. The same product will behave differently across the US, Canada, the UK, and other regions because search language, fulfilment expectations, assortment norms, and seller pressure vary by market. What becomes visible during international expansion is whether the brand has built a coherent marketplace model or merely assembled channel fragments.

One pattern we continue seeing across multiple marketplace ecosystems is that brands with strong products often don’t need reinvention. They need commercial alignment. They need the catalogue narrowed where necessary, fulfilment tightened, channel conflict resolved, and market-specific positioning built with intention.

When that work is done properly, Amazon stops looking like an anomaly. It starts functioning as evidence that the brand can translate across environments without losing margin, control, or clarity.

That is the bigger opportunity. Fixing Amazon is useful. Building a marketplace-native operating model that can travel is far more valuable.

If you’re assessing whether your Amazon underperformance is a tactical issue or a structural one, TPR Brands works with established product brands on marketplace realignment, controlled expansion, and cross-border channel strategy. The conversation is usually most useful when the product is already proven, but the marketplace model isn’t yet working the way it should.