A founder knows the feeling. The product works in retail. Customers already buy it. Distributors understand it. The margin model makes sense off Amazon. Then the Amazon launch goes live and the result is flat traffic, weak sell-through, rising ad spend, and a growing suspicion that the platform is somehow “not for your category”.

Usually, that diagnosis is too shallow.

When brands search for why your product isn't selling on amazon (even though it should be), they're often pushed toward tactical fixes first. Rework the title. Add more keywords. Increase PPC. Improve A+ content. Those things matter, but they rarely explain the full commercial failure of a proven product.

What often sits underneath poor performance is something more structural. The product may be sound, but the marketplace ecosystem around it isn't coherent. The offer may not fit the category economics. The pricing may not survive the channel. The localisation may be weak. The fulfilment setup may undermine trust. The category may look attractive in theory while being poor in practice. For brands already exploring online selling across multiple channels, that distinction matters. Amazon is not just another storefront. It's a tightly ranked, highly comparative environment where fragmented decisions show up quickly.

The Operator's Dilemma When Strong Products Fail Online

A common pattern looks like this. A brand enters Amazon with confidence because the product has already proven itself elsewhere. It may have solid wholesale demand, retail movement, or strong reorder behaviour through existing stockists. On paper, the logic is clean. If customers buy it in-store, they should buy it on Amazon.

Then the marketplace says otherwise.

When a good product enters the wrong ecosystem

One pattern we continue seeing is that founders assume Amazon evaluates products the way traditional channels do. It doesn't. Retail buyers often reward category fit, brand history, packaging quality, and broader range credibility. Amazon evaluates the immediate offer. It asks whether the listing is visible, whether the offer is competitive, whether fulfilment is trusted, and whether the product can convert faster than competing alternatives.

That gap creates false confidence.

A product can be excellent and still underperform because Amazon doesn't rank excellence in the abstract. It ranks marketplace readiness. If the offer lacks enough review depth, if incumbents already dominate the first page, if pricing leaves no room to compete, or if your catalogue arrives without a clear assortment strategy, the platform won't give the product much room to prove itself.

Strong products fail online when operators mistake existing demand for automatic marketplace fit.

The wrong question usually gets asked first

Founders often begin with the wrong diagnostic question. They ask what's wrong with the listing. In many cases, the better question is what's wrong with the product's position inside this specific marketplace ecosystem.

That sounds subtle, but it changes how you respond.

A weak listing can be fixed. A weak ecosystem position is more complicated. It may mean the category is already crowded. It may mean your product architecture is too broad and undifferentiated. It may mean the offer looks expensive once Amazon fees, freight, GST, and local expectations are layered in. It may mean your offline success came from sales support, merchandising, or channel trust that doesn't transfer into a cold digital shelf.

What experienced operators look for first

Before changing copy or spending more on ads, step back and assess the commercial shape of the problem.

| Founder's first assumption | Operator's first question |

|---|---|

| The listing needs better keywords | Is the product visible in a category worth entering? |

| Ads are too weak | Is paid traffic covering for a structural demand problem? |

| The product page needs better images | Does the offer actually deserve the click at this price point? |

| Customers don't understand the product | Is the assortment coherent enough for Amazon discovery? |

That's the core tension. A product can be right for the brand and wrong for the marketplace, at least in its current form. Once you accept that, the diagnosis gets sharper and the decisions get better.

Beyond Listings Diagnosing The Five Frictions of Marketplace Drag

Most underperforming Amazon products don't have one problem. They have one dominant problem and several smaller ones feeding it. Treating everything as a listing issue hides the actual source of drag.

A more useful operating model is to diagnose the business through five frictions.

Visibility friction

This is the most misunderstood friction because teams reduce it to keywords. Visibility is broader than search term inclusion. It's about whether the product can earn discovery in a marketplace that is already dense and comparative.

Helium 10 estimated that Amazon had 9.7 million total sellers globally and 1.9 million active sellers in 2025, which helps explain why even strong products can disappear into marketplace crowding. In that environment, more sellers chasing the same demand usually leads to heavier price competition and higher ad costs, not better conversion, as noted in Helium 10's review of Amazon seller volume.

If your category is crowded, visibility friction won't be solved by adding a few backend terms.

Conversion friction

Conversion friction shows up after the click. The traffic arrives, but shoppers don't move. Sometimes that's about images or copy. Often it's about a wider mismatch between what the customer expects on Amazon and what your offer communicates.

Premium consumer brands run into this frequently. In retail, a premium story can be carried by packaging, shelf placement, and store environment. On Amazon, the product page has to carry more of the persuasion burden. If the page doesn't explain value quickly, the shopper compares price and leaves.

A recent review of Amazon listing control issues makes this point clearly. If the catalogue, content, and offer structure aren't tightly managed, conversion becomes inconsistent even when the product itself is sound.

Commercial friction

Commercial friction is where a lot of Amazon strategies collapse. The product might sell, but not in a way that makes commercial sense.

This happens when fees, inbound freight, discounting pressure, and ad dependency combine to turn revenue into poor contribution. Many brands confuse top-line movement with channel health. They keep pushing traffic into a SKU that was never structurally viable at Amazon price expectations.

What works better is modelling the product as an Amazon offer before scaling it. Can it remain competitive without constant promotional support. Does the pack size make sense. Can fulfilment be handled without creating margin stress. Those questions should be answered before the ad budget goes up.

A useful way to think about the five frictions is this:

- Visibility friction means shoppers never meaningfully discover the offer.

- Conversion friction means the page attracts interest but fails to close.

- Commercial friction means sales happen, but the channel degrades margin.

- Compliance friction means the platform itself limits what you can list or scale.

- Channel friction means Amazon performance is damaged by broader distribution conflict.

The video below gives a practical overview of how marketplace drag builds across a launch.

Compliance friction and channel friction

Compliance friction is rarely visible in early planning decks, but it can halt growth fast. A category approval issue, invoice gap, local returns weakness, or performance threshold problem can turn a launch into a stop-start operation. This is not a marketing issue. It's an operational gate.

Channel friction is different. It appears when the Amazon offer conflicts with your wider commercial structure. Distributors may undercut. Range coherence may break. Pack architecture built for retail may not suit Amazon. A catalogue designed for broad trade coverage can become messy and unrankable online.

Practical rule: if you can't identify the dominant friction, you'll keep spending money on the wrong fix.

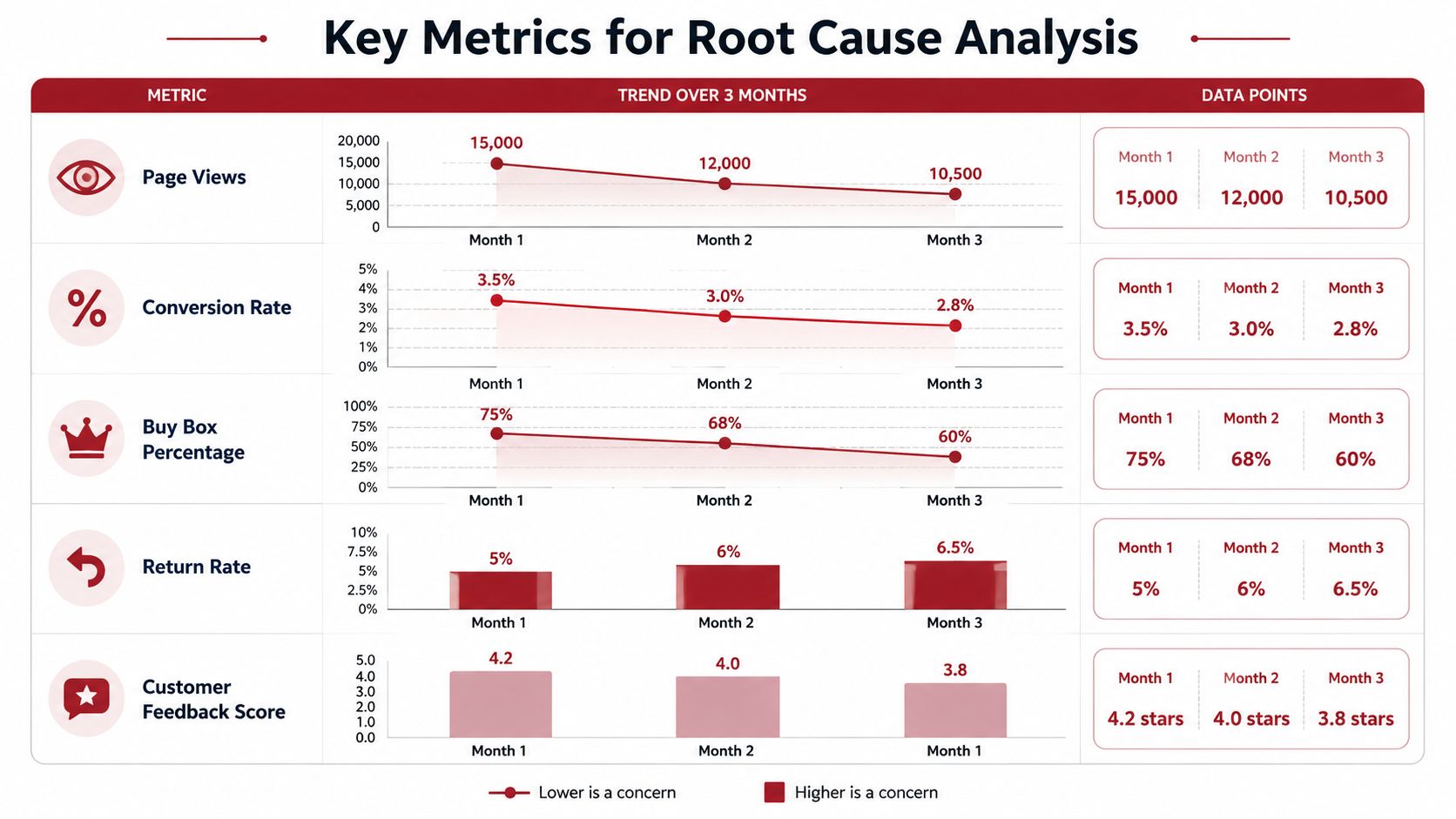

Reading the Signals Key Metrics for Root Cause Analysis

Marketplace underperformance leaves clues. The problem is that many teams read those clues in isolation. They look at traffic, then conversion, then ad spend, then buy box status, each in separate reports. Operators read them as a chain.

Amazon seller guidance notes that the platform has over 600 million different products sold, which means visibility is fragmented and category size alone doesn't guarantee meaningful sales. In oversupplied niches, high sales volume can sit alongside stagnant or falling prices, which is a warning sign that demand may already be fully met, as discussed in Amazon seller guidance on offer competitiveness.

Read patterns, not single metrics

A low conversion rate on its own doesn't tell you much. Neither does low traffic. What matters is the relationship between the signals.

Here's a practical diagnostic table founders can use:

| Signal pattern | Likely issue | What it usually means |

|---|---|---|

| Impressions present, click-through weak | Conversion friction | The search appearance is not compelling enough to earn the click |

| Click-through healthy, conversion weak | Offer or page friction | The product page, pricing, trust signals, or reviews aren't closing the sale |

| Paid traffic running, sessions still thin | Visibility friction | Ads may be compensating for weak organic discoverability in a crowded category |

| Buy Box unstable | Commercial or operational friction | Price, fulfilment, or seller setup is weakening competitiveness |

| Returns or negative feedback rising | Reputation friction | Expectations and delivered experience are diverging |

The point isn't to memorise metrics. It's to identify the bottleneck that controls the rest.

What experienced operators notice quickly

Across connected devices and premium household categories, one issue we repeatedly observe is that teams overreact to the metric they understand best. Performance marketers focus on traffic. Brand teams focus on imagery. Sales leaders focus on price. Operations focus on stock availability.

Amazon doesn't care which department owns the issue. It aggregates the result.

If sessions are acceptable but conversion is soft, examine the page from the shopper's point of view. Does the main image immediately clarify the product. Does the title communicate the right use case. Does the first screen justify the price relative to alternatives. Is the range too complex for quick comparison. These are commercial questions, not cosmetic ones.

A listing can look polished and still perform badly if the offer structure is wrong.

Metrics that matter more than teams admit

Some metrics carry more diagnostic value than brands give them credit for.

- Buy Box percentage: This often reveals whether the offer is competitive. If the buy box is inconsistent, your traffic quality won't matter much.

- Session trend by ASIN: This shows whether demand is concentrating around a few products while the rest of the catalogue drifts.

- Conversion by variation or pack format: Useful for spotting whether the issue is product-market fit or the wrong presentation.

- Returns and feedback themes: These expose hidden expectation gaps that marketing language can conceal.

- Organic versus paid dependency: If sales rely too heavily on paid support, the product may be commercially fragile.

Many brands discover that the problem isn't “Amazon performance” in the abstract. Instead, it's a specific chain reaction. Weak click-through leads to expensive traffic. Expensive traffic pressures pricing. Pricing pressure hurts margin. Margin pressure limits inventory confidence. Then stock and ranking become unstable.

That's also why a lot of products sell on Amazon and still disappoint the business. The revenue exists, but the economics deteriorate underneath. The article on why some Amazon products make less money than founders expect speaks directly to that pattern.

Use metrics to eliminate bad assumptions

The cleanest operator move is to remove explanations one by one.

If traffic is low, don't assume the page is weak. If click-through is healthy, don't assume the category has enough depth. If conversion is decent, don't assume the SKU deserves more ad spend. Each metric should narrow the field.

The best marketplace teams don't ask, “How do we improve everything?” They ask, “Which friction is limiting this ASIN right now?”

Localisation is Non-Negotiable Marketplace Nuances Across Regions

A founder sees strong sell-through in the US, launches the same SKU in Australia, keeps the same images, adapts the copy, and expects the economics to follow. Then sales stall. The usual fixes start. More PPC, more keyword edits, more listing changes. However, the underlying problem often sits higher up. The product has entered a different marketplace system, with different demand depth, different trust signals, and different operating constraints.

The same product behaves differently in different ecosystems

International expansion exposes a mistake that is easy to miss from head office. Amazon is not one market with different domains. Each region has its own commercial shape.

A product that works cleanly in the US can struggle in Australia even with a competent listing. A range that feels focused in the UK can look too broad in a smaller marketplace. A premium wellness item that earns trust quickly in one region may need more proof, clearer claims discipline, or a different pack structure somewhere else.

Australia is a good example. Weak sales are often blamed on pricing or PPC, but the structural question comes first. Is the category deep enough on Amazon.com.au to support momentum for this SKU. SellerLogic's review of why products stall on Amazon notes that some products face a thinner local demand pool than founders expect, which matters even more in a smaller marketplace like Australia.

Australia introduces operational friction earlier

For Australian brands, operational constraints show up earlier in the cycle. Restricted categories, brand gating, local returns expectations, tax treatment, and freight economics can all affect whether an offer is commercially workable before the listing has had a fair chance to perform.

Helium 10's summary of Amazon approval requirements outlines that sellers may need invoices, good account health, and other approval inputs before they can fully participate in certain categories. In practice, that means discoverability can stay constrained even when demand exists, because the seller cannot yet meet the conditions required to trade properly in that category.

This changes the launch logic. The question is not only whether shoppers will like the product. The question is whether the offer is fully tradable in the local version of Amazon. Can the business support local returns. Is the documentation ready before stock lands. Does the category gate delay ranking momentum. Does the margin still hold after local freight, GST, and marketplace fees are applied.

Localisation is commercial, not cosmetic

Localisation is often treated as wording. On Amazon, it is a market-fit decision.

It covers the offer itself. Pack architecture. Fulfilment model. Range depth. Review transfer limits. Price psychology. The level of explanation local shoppers need before they trust the product.

A premium home organisation product might convert quickly in one region because shoppers already understand the use case and the premium benchmark. In another, the same item may need a tighter assortment, clearer visual education, or a different pack format before the unit economics make sense.

That is why marketplace localisation across regions is a market-fit exercise, not a translation task.

The product enters a new region with your pricing logic, fulfilment structure, proof system, and catalogue decisions attached to it.

From Diagnosis to Action Prioritising Strategic Experiments

A founder sees a good product stall on Amazon and assumes the fix is more motion. New images. More ads. Extra keywords. In practice, that often makes diagnosis harder, because several variables change at once and no one can tell which problem moved.

The better approach is narrower. Once the main friction is clear, run experiments that test one commercial assumption at a time. The goal is to find the constraint that is holding the offer back, then decide whether it can be fixed profitably.

Match the experiment to the friction

Each experiment should match the type of drag you are seeing.

If visibility is weak, start by testing market access and search fit. Check whether the product sits in a category with enough shopper activity to support ranking. Check whether the search terms reflect how people in Australia shop, rather than how the brand describes the product internally. Also check whether the ASIN is being suppressed by stronger substitutes, a poor category path, or a low-relevance offer.

If conversion is weak, test trust and value communication. Main image, title structure, pack logic, pricing presentation, and review context all shape the first purchase decision. The useful question is whether the offer becomes easier to buy without stripping out the reason someone would pay a premium.

If margin is the problem, creative work will not rescue the SKU. Test offer design instead. A bundle, multi-pack, variant reduction, or a tighter entry range can change the economics enough to make the product viable in-channel.

Some tests should not happen yet. If stock keeps dropping in and out, or FBA setup is unstable, conversion testing will produce unreliable conclusions. Fix operating instability first.

A practical prioritisation sequence

Priority should follow commercial risk, not internal enthusiasm.

Remove hard blockers first

Compliance issues, gating, stock instability, and fulfilment setup can cap performance before demand has a chance to show up.Test the offer before scaling traffic

Sending more clicks to a weak offer usually burns budget and muddies the signal.Pressure-test unit economics early

If the SKU only works when freight is favourable, ad costs stay low, and returns remain minimal, the offer is too fragile for aggressive expansion.Prove one repeatable win before widening the catalogue

A single stable ASIN gives clearer operating evidence than five partial launches with conflicting results.

Ask questions that change the decision

Weak experiments usually start with weak framing. Teams ask whether they need more ads or better bullets when the core decision sits higher up the chain.

Ask whether the category is structurally rejecting the product at its current price and format. Ask whether a different pack architecture would improve both conversion and contribution margin. Ask whether the issue is low trust, low demand, low discoverability, or a product that does not fit Amazon's economics in that market.

That last point matters in Australia. Some products can win on Amazon.com.au, but only with a restrained range, a tighter price ladder, or a slower investment pace than the brand planned. Other products should not be pushed hard until there is evidence that the category has enough depth to support sustained sales.

Good marketplace operators accept that some experiments produce a harder answer than expected. The result may be that the listing needs work. It may also be that the SKU needs a different format, a different fulfilment model, or less capital.

Decision test: if the experiment succeeds, does it improve revenue quality, margin quality, or confidence in the next strategic move? If not, it is probably the wrong experiment.

Building a Cohesive Marketplace Ecosystem

The strongest Amazon businesses don't win because they have one well-written listing. They win because the whole marketplace system is coherent.

The product fits the category. The price makes sense in-channel. Fulfilment supports trust. The range is organised for discovery. Compliance isn't blocking scale. Localisation reflects actual market behaviour. Reviews, offer structure, and margin discipline reinforce each other instead of fighting each other.

That's why “selling on Amazon” is too narrow a goal for an established brand.

A serious brand needs to build a marketplace ecosystem that can hold together under competition, regional variation, and channel pressure. That becomes even more important when expansion moves across Australia, North America, the UK, or Asia. Each market exposes different weaknesses. Each one also rewards operators who can see the structural issue before they waste money treating the symptom.

Founders who recognise that distinction usually make better decisions. They stop chasing isolated fixes and start building a system that can carry the brand properly. That's where stronger long-term growth comes from.

If you're evaluating why a proven product is stalling on Amazon, or you're planning marketplace expansion into Australia, the US, Canada, the UK, Japan, or broader international channels, TPR Brands works with established product companies on the structural side of growth. That includes positioning, localisation, channel fit, compliance awareness, and marketplace ecosystem design so expansion is commercially coherent rather than just technically live.