A founder asks a fair question. “We're live in the market. The listings are translated, the pricing is converted, and the marketplace account is active. Why isn't the product moving?”

Usually, the answer isn't creative quality alone, and it isn't just traffic. The product is available, but it doesn't feel local. Buyers sense distance long before they articulate it. They see it in delivery promises, in category placement, in how the product is merchandised, and in whether the marketplace itself treats the listing as native to the ecosystem or as an import that happens to be visible.

That's the core tension behind Marketplace Localisation: Why Some Products Feel “Closer” Than Others. Closeness isn't only about language, and it isn't only about geography. In practice, it's an operational and ecosystem construct. Some products feel nearby because the entire marketplace experience tells the customer, “this fits how people buy here.” Others stay oddly distant even when they're technically purchasable.

When 'Live' in a Market Is Not the Same as Being 'Local'

Why does a product go live on a marketplace, meet the launch checklist, and still feel foreign to the customer?

We see this pattern repeatedly in international marketplace accounts. The title is translated, the bullets are readable, the price is converted, and the listing is technically available. Head office reads that as market entry. The local customer reads it very differently.

What they assess, often in seconds, is whether the offer behaves like something that belongs in that market. They look for delivery confidence, familiar category placement, clear attributes, credible seller signals, and the small cues that suggest the product is supported locally rather than merely shipped across borders. If those signals are weak, performance slows before the brand has enough data to diagnose why.

Availability is not enough

A visible listing can still sit outside the market's commercial centre of gravity. Marketplaces rank and recommend products that fit local buying behaviour, local service expectations, and the platform's own operating logic. A product can be purchasable and still feel out of place.

That is the core gap many founders miss.

In marketplace-heavy markets such as Australia, buyers are trained by the strongest operators on the platform. They compare your offer against the best local standard they see every day. The comparison is not only about price or creative quality. It is about whether the product looks easy to buy, easy to receive, and easy to trust.

Practical rule: Customers judge the operational shape of the offer, not just the product itself.

A listing with long delivery windows, inconsistent attributes, imported sizing logic, or weak stock confidence signals distance. The customer may never describe the issue as localisation. They move to the option that feels lower risk.

The hidden gap founders underestimate

Founders often place localisation inside the content workstream. The operational reality is broader. Localisation includes fulfilment confidence, taxonomy alignment, review readiness, returns logic, customer support expectations, and whether the listing can compete cleanly inside local search and filtering rules.

This is why translated content often fails to convert. The words have been adapted. The offer has not.

For brands working on a more serious product localisation strategy, this is usually where the core work begins. A product feels closer when the marketplace ecosystem treats it as native, and when the customer sees enough local proof to buy without hesitation.

Deconstructing 'Closeness' in Fragmented Ecosystems

Many brands still talk about “going global on marketplaces” as though they're entering one channel with several country settings. That framing causes expensive mistakes. Across multiple marketplace ecosystems, what looks like one platform from head office is often a collection of very different local businesses.

The platform is global. The buying behaviour isn't

This matters acutely in APAC. According to PaymentsCMI's APAC ecommerce market data, ecommerce in Asia Pacific excluding China is projected to exceed US$1.1 trillion in 2026 and is projected to continue growing at 12% annually through 2027, reaching more than US$1.5 trillion. The same source also references a separate forecast that valued the broader Asia Pacific ecommerce market at US$4.76 trillion in 2025 and projected US$12.46 trillion by 2034.

Those headline numbers tempt brands into broad regional expansion. The structural reality is less tidy. The same APAC view shows Shopee leads Southeast Asia and Taiwan, Coupang dominates Korea, Rakuten leads Japan, and Amazon does not rank in the top three marketplaces in any of those markets. So even the most recognisable global marketplace operators still face local platform disadvantage in many regions.

That's why copying a catalogue from one market to another rarely works cleanly.

Why the same product feels different by market

The product isn't assessed in isolation. Customers assess it inside a local ecosystem with its own norms.

A hardware item sold in Australia may compete on practical delivery confidence, range clarity, and trust signals around availability. The same item in Japan may need tighter category mapping, different visual cues, and a more disciplined presentation of specifications. In Southeast Asia, platform dynamics, local merchandising styles, and fulfilment assumptions may shift again.

Here's where founders often oversimplify the problem:

| Marketplace assumption | Operational reality |

|---|---|

| One strong catalogue should travel | Each market reads the catalogue through local platform logic |

| Translation creates localisation | Translation only changes language, not buying confidence |

| Platform scale creates trust automatically | Trust is built by local relevance, fulfilment, and presentation |

| Global marketplaces behave similarly | Regional ecosystems have different leaders, standards, and expectations |

A marketplace account can be internationally active while remaining locally weak.

Fragmentation damages more than growth

One issue we repeatedly observe is that fragmentation doesn't only suppress revenue. It erodes margin quality, forecasting, and operational control. Brands start spending to force visibility in markets where the core offer hasn't been structurally adapted. Paid traffic compensates for weak local fit, but only temporarily.

A stronger way to think about expansion is this: each marketplace-country combination is a distinct commercial environment. It deserves its own operating logic, not just its own translated listing. Once founders see that, “closeness” stops sounding soft and starts sounding like what it really is. A measurable expression of ecosystem fit.

What We See When Reviewing International Marketplace Accounts

When international marketplace accounts underperform, the problem rarely sits in one obvious place. It usually shows up as a cluster of small mismatches that make the product feel harder to find, harder to understand, or harder to trust. We think of that cluster as operational drag.

Taxonomy failure looks like weak demand

The most common hidden issue is not always poor branding. Sometimes the marketplace cannot place the product properly. When taxonomy and attributes are mapped badly, discoverability falls before a customer ever sees the listing.

According to Emplicit's analysis of marketplace localisation, incorrect product taxonomy and attribute mapping can reduce organic discoverability by 40% to 60%. That's a technical failure, but to the founder it often looks like a market demand problem.

A product can be excellent and still become functionally invisible if it sits in the wrong node, uses the wrong attribute logic, or carries dimensions and specifications in a format that doesn't align with the marketplace's internal structure.

For operators working through Amazon listing control and catalogue governance, listing management stops being administrative and becomes a structural visibility issue.

Fulfilment drag changes customer perception

The second pattern is fulfilment mismatch. The listing may promise delivery from a remote warehouse into a market where customers have been trained to expect something faster, simpler, and locally resolved if anything goes wrong.

That changes how the product feels.

In account reviews across household products, consumer electronics, and home categories, this shows up in familiar ways:

- Delivery windows feel imported: The listing technically serves the market, but the promised timeline tells the customer the product is still elsewhere.

- Returns feel uncertain: Even if the policy exists, the customer senses extra friction.

- Support looks disconnected: The product page answers what the item is, but not how the local buyer will be looked after.

If the operational promise feels distant, the product itself feels distant.

Operational drag is cumulative

A miscategorised listing can suppress discovery. A weak local delivery promise can reduce click confidence. Generic visual merchandising can lower conversion once the customer lands. None of these failures needs to be dramatic on its own. Together, they create the impression that the product doesn't belong in-market yet.

That's why mature marketplace work is less about isolated optimisation and more about removing compounded friction. The product starts to feel closer when the catalogue, the category placement, the operational promise, and the customer's interpretation all point in the same direction.

Who Is Truly Responsible for Your Brand's Reputation

A dangerous mistake in marketplace expansion is assuming responsibility transfers with the work. It doesn't. A brand can outsource execution, but it cannot outsource accountability for how the brand is presented, priced, fulfilled, and trusted in-market.

That distinction matters because many external partners operate at task level. They manage listings, advertising, tickets, and reporting cycles. Those functions can be useful. They are not the same as protecting your brand's reputation across an international marketplace ecosystem.

Vendors complete tasks. Operators manage consequences

A tactical partner may improve a title, adjust bids, or refresh images. That's not unimportant. But if the underlying marketplace setup is damaging customer trust, those actions sit on top of a structural problem.

Founders often discover this too late. By then, several issues may already be in play:

- Pricing has drifted: The market sees inconsistency across channels.

- Catalogue logic has fractured: Variations, bundles, and attributes no longer support a coherent buying journey.

- Brand narrative has thinned out: The product still appears online, but the offer no longer feels premium, specialised, or locally credible.

None of that is solved by more low-level account activity.

Reputation is built through repeated market signals

Customers don't separate operational flaws from brand identity. If shipping feels uncertain, they attribute that uncertainty to the brand. If the marketplace page is badly structured, they infer something about product quality. If support expectations look vague, they hesitate.

That's why founders need a simple internal rule. The brand owner remains responsible for the commercial experience, even when another party handles day-to-day marketplace work.

A useful way to think about partner roles is this:

| Partner type | Usually manages | Usually does not own |

|---|---|---|

| Tactical marketplace vendor | Listings, media swaps, ad execution, routine reporting | Brand architecture, channel conflict, long-term ecosystem trust |

| Strategic marketplace operator | Execution plus market fit, structural risk, localisation logic, commercial cohesion | Final brand accountability, which stays with the brand owner |

The question isn't whether someone can run your marketplace account. It's whether they understand what your account is doing to the brand.

What founders need to hold internally

Even with strong external support, several decisions should remain visibly governed by the brand. Positioning, pricing boundaries, fulfilment standards, product hierarchy, and local market narrative shouldn't drift through convenience or agency habit.

The brands that protect reputation best don't become controlling for the sake of it. They become clearer about decision rights. They know which tasks can be delegated and which signals shape the long-term value of the brand in-market.

How Stronger Brands Build Fulfilment Confidence and Trust

Why does one marketplace listing feel easy to buy from, while another selling a similar product still feels foreign?

Stronger brands treat closeness as an operating outcome. Customers make that judgement from the service promise around the product, not from copy alone. If delivery looks credible, the category placement makes sense, and support feels reachable, the product starts to register as local.

Convenience is a trust signal

In marketplace operations, convenience is not a nice extra. It is part of how buyers judge legitimacy.

Price still matters. But in mature marketplace environments, shoppers also use fulfilment speed, delivery clarity, membership benefits, and platform familiarity as shorthand for risk. A listing can be competitively priced and still feel distant if the path from checkout to delivery looks uncertain.

That matters because customers rarely separate the product from the operating model behind it. If stock availability looks unreliable, delivery dates look vague, or returns appear awkward, the listing creates friction before the order is placed.

What strong brands align

Brands that build fulfilment confidence usually align three layers at the same time.

The offer has to feel buyable

A product feels closer when the operational promise matches local marketplace norms. That includes dispatch expectations, return logic, stock depth, shipping thresholds, and how clearly the customer can tell what happens after purchase.

For brands refining international fulfilment strategy, the practical question is whether the fulfilment model supports the promise the listing is making. Many international accounts fail here. The page suggests a local buying experience, but the backend still behaves like a cross-border export setup.

Customers notice that gap quickly.

The listing has to feel native

Native listings do more than read well. They reflect how the local marketplace organises choice.

That means titles follow local category logic, attributes map cleanly to how buyers filter, and product benefits appear in the order shoppers expect to compare them. A technically translated listing can still feel imported if the taxonomy is off or the specification hierarchy clashes with the way the market shops the category.

Visual presentation matters too. Strong operators review what local competitors are doing with pack shots, infographics, claims, and proof points, then adapt without stripping the brand of coherence. The goal is not cosmetic localisation. The goal is reducing hesitation at the point of comparison.

The support model has to feel reachable

Customers do not need to inspect your service setup to decide whether they trust it. They infer it from the offer in front of them.

A clear arrival window, recognisable return terms, consistent seller messaging, and visible post-purchase accountability all increase confidence. If those signals are weak, the product feels operationally far away even if it is technically available in the market.

I usually test this with four basic questions:

- Can the buyer tell when it will arrive?

- Do the listing attributes reflect local comparison behaviour?

- Does the merchandising style match the category norm in-market?

- If something goes wrong, does the customer believe resolution will be straightforward?

A short discussion on marketplace convenience and location logic is useful here:

The strongest brands build trust by making the whole ecosystem feel dependable. That is what creates closeness. Not geography on its own, and not language on its own. A product feels local when fulfilment confidence, taxonomy fit, and perceived presence all support the same commercial story.

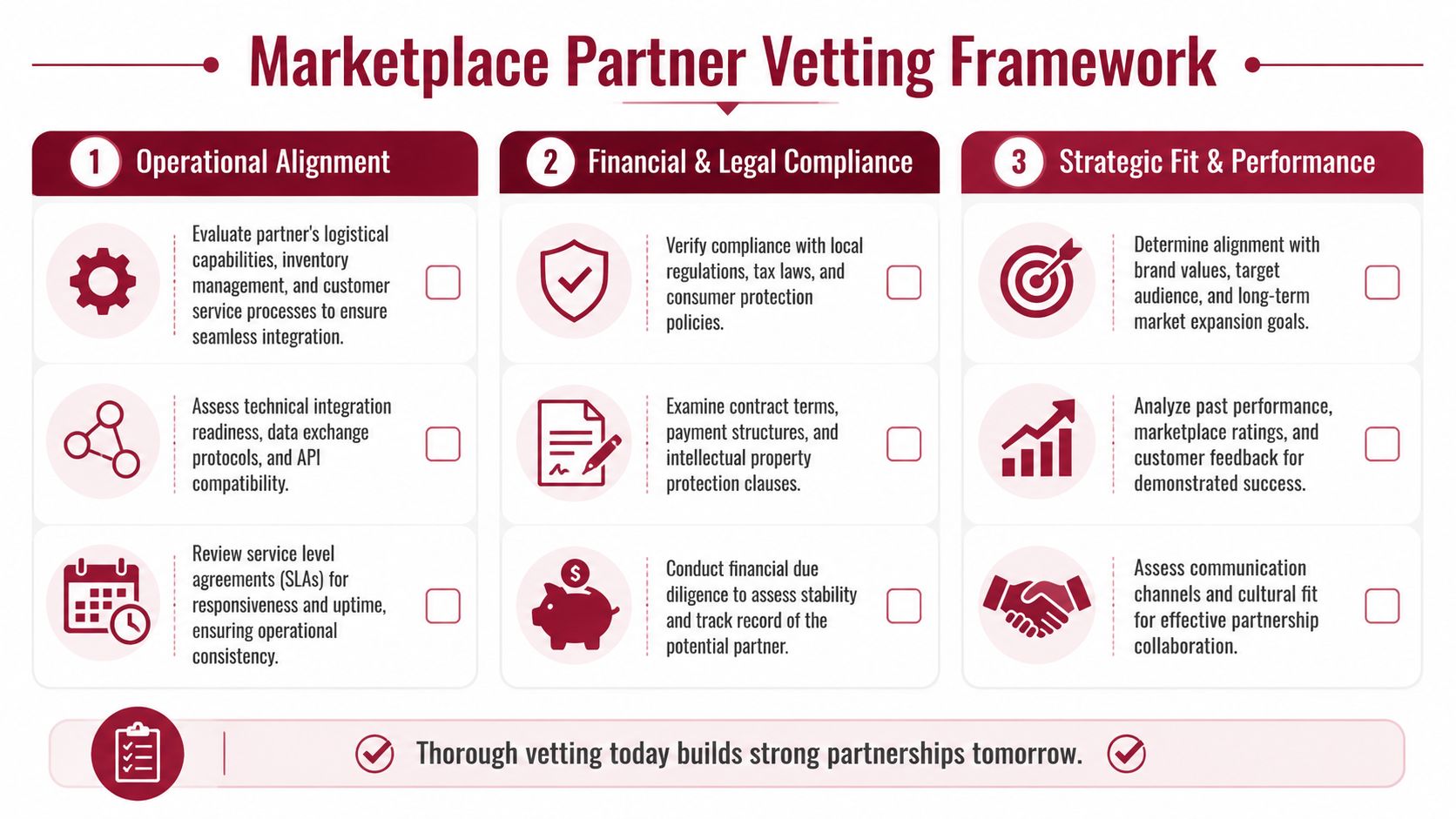

A Governance Framework for Vetting Growth Partners

Why do so many marketplace partnerships look productive in reporting and still leave the brand feeling distant to local customers?

The usual reason is simple. The partner is being assessed on activity, not on whether they can build local market credibility. Fast listing deployment, ad spend management, and SKU coverage matter, but they do not answer the harder question. Can this operator reduce the structural friction that makes a product feel imported, inconvenient, or out of step with the category?

Start with operating control

A credible partner should be able to explain how they make decisions, who approves changes, and what signals trigger adaptation by market. If they can only describe campaign execution, they are offering labour. They are not offering channel stewardship.

I look at three areas first.

Operational alignment

The operational test is whether the partner can diagnose local mismatch before it shows up as a major commercial problem.

Ask direct questions:

- How do you handle taxonomy differences between marketplaces?

- What do you do when product attributes do not map cleanly into a local category structure?

- How do you assess whether fulfilment setup is supporting conversion confidence or weakening it?

- What tells you a product is indexed and visible but still feels far away to the buyer?

A good operator can discuss content structure, inventory logic, fulfilment configuration, returns expectations, and category norms in one conversation. If those topics sit in separate silos, the brand usually gets fragmented execution.

Financial and legal control

Partnerships deteriorate when decision rights are vague. I have seen brands lose weeks undoing title changes, promotional decisions, and bundle variations that made sense to an agency but damaged positioning in-market.

Review the agreement for clear boundaries on:

- Brand control: Who can change titles, bundles, imagery, or positioning without approval?

- Data ownership: Who owns account data, content assets, search term learnings, and reporting history?

- Pricing authority: Who can change pricing, discounting, or promotional structures?

- IP and channel protection: What happens if assets are reused outside the intended scope?

These terms shape day-to-day brand coherence. They also determine how difficult recovery becomes when performance drops or the relationship ends.

Decision filter: If a partner asks for broad execution freedom but resists clear approval rules, reporting access, or ownership terms, you are being asked to accept delivery risk without proper control.

Strategic fit shows up in the questions they ask

Experienced operators do not start with a templated launch plan. They ask how the category is bought locally, what fulfilment promise the market expects, which attributes drive comparison, and where the current offer creates hesitation.

That matters because marketplace localisation is an ecosystem problem. A partner who treats every market as a content and ads workflow will miss the underlying causes of weak traction. In practice, the failure points are often classification, shipping logic, local service expectations, and inconsistent signals of local presence.

I put a lot of weight on curiosity here. If a prospective partner is not probing operational constraints, customer trust expectations, and competitor merchandising norms, they are unlikely to catch the reasons your product feels misaligned after launch.

A short founder checklist

When reviewing a potential Amazon expansion partner, use a simple checklist:

- Can they explain why a product may be live but still feel non-local?

- Do they discuss fulfilment confidence, category structure, and customer friction, or only content and ads?

- Can they explain how market differences affect merchandising, returns expectations, and offer design?

- Do they separate execution tasks from strategic brand responsibility?

- Will they work within clear rules on pricing, data access, approvals, and asset ownership?

Providers sit in different roles. Some brands rely on internal teams. Some appoint specialist operators. Some work with expansion partners such as TPR Brands when they need support across localisation, channel selection, and international market adaptation. The label matters less than the operating model. The ultimate test is whether the partner helps your brand feel credible, accountable, and commercially native in the market you are entering.

From Product Listing to Ecosystem Leadership

A product doesn't feel close because it has been uploaded into the right country account. It feels close when the marketplace, the listing, the fulfilment promise, and the customer's expectations all reinforce one another.

That's why marketplace localisation is a leadership function, not a translation task. Founders who treat expansion as a catalogue deployment project usually end up paying to correct structural mismatch later. Founders who treat it as ecosystem construction tend to build stronger trust, cleaner operations, and better long-term channel quality.

One issue the market still underestimates is that perceived locality is often driven by buying convenience more than physical distance. As discussed in guidance around marketplace location logic and convenience, brands can improve local placement by optimising fulfilment promises and pickup options, not only by adjusting geographic targeting, as noted in this discussion of real buying convenience in marketplace environments. That's a more useful operating question than “how do we look local?” The better question is “how do we reduce the friction that makes us feel far away?”

Products that feel close are rarely accidental winners. Someone has built the conditions for trust. Someone has aligned the offer with the ecosystem. Someone has decided that being present in-market isn't enough.

If your brand is already proven and you're assessing how to make marketplace expansion commercially coherent across regions, TPR Brands works with established product businesses on localisation, channel structure, and controlled international growth.