Most advice about Amazon treats it like a demand tap. List the product, turn on ads, let the marketplace do the work.

That’s fine… until you realize you don’t actually control what’s happening on your own listings.

Over the past week, I analyzed six established product brands across Australia, the US, Canada, and the UK.

On the surface, every one of them looked like they were “doing Amazon.” Products live. Sales happening. Reviews building.

Underneath… it was a different story.

- Multiple sellers competing on the same listings.

- Pricing drifting between markets.

- Brand presentation inconsistent depending on who touched the listing last.

Not one of them had full Amazon listing control.

And the most dangerous part?

On the surface, all of them looked fine.

What We Found Across 6 Brands on Amazon

That view is too shallow for any founder who cares about brand value.

Amazon is not just a channel. It is an operating environment with its own incentives, its own ranking logic, its own tolerance for seller overlap, and its own control over customer access. If you enter that environment without a plan for ownership, permissions, pricing, and enforcement, the platform starts making brand decisions for you. It influences who appears on your listing, what customers see first, how low the market price falls, and how much of the customer relationship you retain.

This is how control quietly shifts from the brand owner to the marketplace itself. The risk is not only lost margin. It is the slow transfer of authority from the brand owner to the marketplace.

For established hardware, home improvement, household, and consumer product brands, this matters even more. These categories rely on trust, specification accuracy, consistency, and channel discipline. A weak Amazon setup doesn’t stay isolated to Amazon. It spills into retail relationships, distributor expectations, and international expansion.

Why Amazon Is More Than Just a Sales Channel

Amazon often gets discussed as if it sits beside wholesale, retail, and DTC as one more place to sell stock. That framing misses the true trade-off.

The dangerous part isn’t failure.

It’s when it looks like it’s working… while control is quietly slipping underneath.

A retailer buys products. A marketplace shapes behavior.

When founders call Amazon “just another channel”, they usually mean one of two things. They either expect incremental revenue without reworking their operating model, or they assume the product’s existing brand equity will carry across unchanged. In practice, neither assumption holds for long if control is loose.

Amazon rewards availability, not brand intent

Amazon’s systems are built to maximise conversion, fulfilment reliability, and price competitiveness. That sounds harmless until it collides with the way strong brands are built.

Brands care about:

- Positioning discipline. The right claims, imagery, hierarchy, and product context.

- Channel consistency. Not letting one outlet destabilize every other customer relationship.

- Margin protection. Preserving enough gross profit to keep product quality, support, and innovation intact.

- Customer experience. Making sure the post-purchase experience matches the promise.

Amazon cares about the listing that converts, the seller that fulfils, and the offer that wins.

Those priorities overlap at times. They are not the same thing.

The real asset at risk is authority

A founder can tolerate some ad inefficiency. They can tolerate a learning curve. What they cannot afford to ignore is authority leakage.

When multiple sellers touch the same listing, when imagery changes without brand oversight, when pricing falls below what retail partners can live with, the market stops treating the brand owner as the final authority. Customers stop knowing who the “real” seller is. Retailers stop trusting the brand’s channel discipline. Internal teams start making defensive decisions instead of strategic ones.

Amazon can produce sales volume while quietly reducing control over the conditions that made the brand valuable in the first place. I see this far more often than most founders expect.

That is why experienced operators don’t ask only, “Can we sell on Amazon?” They ask, “Under what structure do we preserve control while using Amazon profitably?”

Sales growth without control is often borrowed growth

A business can look healthier in the short term while becoming weaker underneath. Amazon is one of the clearest examples.

Revenue can rise while:

- Price integrity slips

- Retail partners complain

- Unauthorized sellers appear

- Support costs increase

- Brand presentation fragments

- Customer ownership stays with the platform

A founder who understands that dynamic starts treating Amazon less like a catalogue upload task and more like a strategic governance issue.

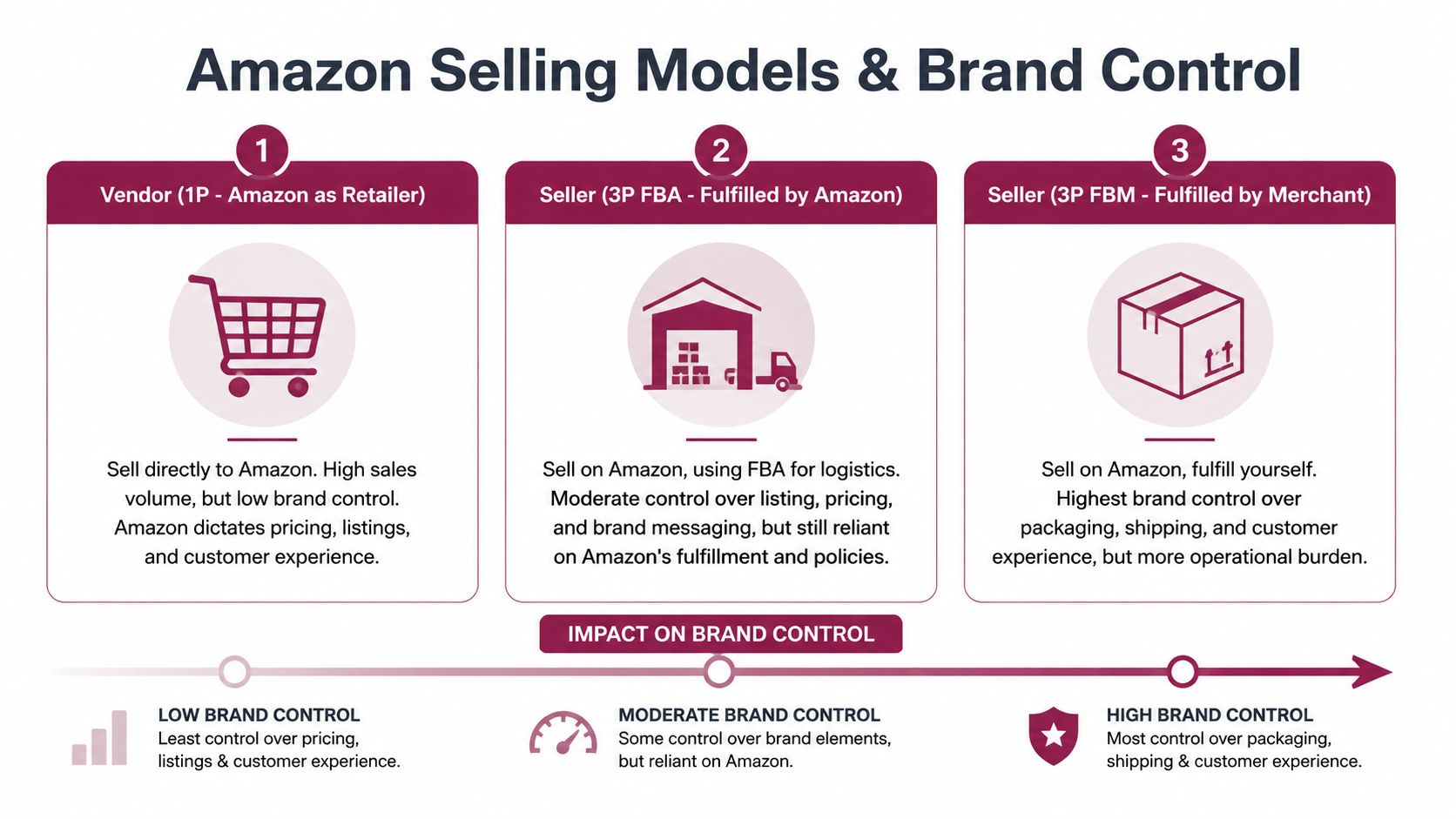

The Three Faces of Amazon: How Your Selling Model Defines Control

Most brands don’t lose control on Amazon because they made one dramatic mistake. They lose it because they chose a selling model that didn’t match their real goals.

The platform gives you several routes in. They are not equivalent. Each one changes who controls price, inventory decisions, presentation, fulfilment experience, and the speed at which problems spread.

1P means Amazon is the retailer

In a 1P model, you sell wholesale to Amazon through Vendor Central. Amazon becomes the retailer of record.

This can look attractive to established manufacturers. It feels familiar. Amazon places purchase orders, takes inventory risk at its level, and the relationship resembles large-scale retail supply.

The cost is control.

Amazon has greater influence over retail pricing, promotion timing, listing treatment, and how the customer experiences the offer. If the platform decides to discount aggressively, your objections may not carry much weight. If it changes operational priorities, your catalogue can feel that change before your team has time to react.

1P can make sense when volume and operational simplicity matter more than tight control. It is usually a poor fit for brands that need disciplined pricing architecture or that are already managing sensitive retail relationships.

3P with FBA gives more control, but not full independence

In 3P through Seller Central using Fulfilled by Amazon, the brand or appointed seller owns the marketplace account while Amazon handles warehousing and delivery.

For many brands, this is the middle ground. You generally retain more control over listing content, offer management, and promotional planning than in 1P. You also gain access to tools that support stronger brand presentation when the account structure is set up correctly.

But this isn’t autonomy. It is partial control inside Amazon’s infrastructure.

You still rely on Amazon’s fulfilment rules, storage logic, fee structure, and policy environment. If inbound constraints tighten or fee economics change, the account feels it quickly. If multiple sellers enter the listing, FBA does not solve the governance problem on its own.

3P with FBM offers the most direct control

In 3P fulfilled by merchant, you sell through Amazon but manage fulfilment yourself or through your own logistics partner.

This model gives the brand more direct influence over packaging, dispatch rules, stock handling, and some aspects of customer experience. It can work well for bulky, complex, regulated, or margin-sensitive products where FBA creates more friction than value.

The trade-off is operational burden. You need fulfilment discipline, service performance, and systems that can hold up under marketplace expectations. Many brands like the control but underestimate the process maturity required.

Decision test: If your team cannot maintain fast fulfilment, clear catalogue ownership, and disciplined seller permissions, the highest-control model can still produce low-control outcomes.

Hybrid models often create the messiest results

A lot of brands drift into a hybrid setup. Amazon buys some products as 1P. The brand runs some ASINs as 3P. A distributor lists a few lines. Another reseller joins later.

Hybrid isn’t automatically wrong. It becomes dangerous when no one has documented authority over who sells what, where, and under which rules.

That is usually the point where listing confusion, pricing disputes, and internal blame begin.

Amazon Selling Models Brand Control Comparison

| Control Factor | 1P (Vendor Central) | 3P (Seller Central) |

|---|---|---|

| Retail pricing influence | Lower | Higher |

| Listing control | Lower to moderate | Moderate to higher |

| Inventory ownership on marketplace side | Amazon | Brand or authorised seller |

| Customer experience control | Lower | Higher, especially with FBM |

| Operational burden | Lower | Higher |

| Ability to centralise seller permissions | Limited | Stronger if governed properly |

A useful way to think about the choice is this: the more convenience you hand to Amazon, the more strategic authority you usually surrender with it.

If you’re dealing with multiple sellers on your Amazon listing, this is usually where it starts to go wrong. If reseller sprawl is already showing up, what multiple sellers on your Amazon listing really means is usually not “healthy demand”. It often means your control model was never clearly established.

How Brands Lose Amazon Listing Control

Amazon rarely weakens a brand in one dramatic moment. The more common pattern is slower and more dangerous. A product starts working, demand builds, and the listing becomes attractive to sellers who care more about short-term turnover than the brand behind it.

At that point, the ASIN stops functioning like a controlled commercial asset. It becomes open territory.

How erosion usually starts

The sequence is predictable, especially in categories where a strong listing signals proven demand.

-

A listing gains traction

Reviews accumulate, conversion improves, and the product starts ranking for commercially useful search terms. -

New sellers attach to the ASIN

Some are authorized. Some are grey-market operators, liquidation buyers, or resellers sourcing through channels the brand never approved. -

Price becomes the fastest way to win

Sellers cut price because it is easier than improving content, service, or stock position. -

The customer experience splits

Packaging quality, fulfilment speed, returns handling, and post-purchase support vary by seller, even though the shopper sees one listing. -

The brand absorbs the reputational hit

Customers do not separate seller behavior from brand ownership. If the experience is poor, the brand takes the blame.

Founders often misread this as a marketplace irritation. It is a channel control failure.

Why this gets expensive fast

Once unauthorized sellers cluster around a successful ASIN, Amazon starts rewarding whoever can stay in stock, move quickly, and compete on price. That can look healthy in a dashboard. It is often corrosive in the broader business.

The first problem is margin. The second is authority.

A 2021 analysis from Gartner on third-party marketplace expansion found that unauthorised and unmanaged sellers create pricing inconsistency, weaker partner confidence, and higher enforcement costs across digital channels, especially for established consumer brands operating through multiple routes to market. Those effects are not limited to Amazon. They show up in wholesale relationships, distributor conversations, and internal forecasting.

That is the strategic cost many brands underestimate. They entered Amazon to add revenue. They ended up creating a public market that trains customers and trade partners to question whether the brand controls its own pricing, presentation, and seller network.

If ownership and authority over the listing are still unclear, the bigger problem usually sits upstream. Who actually owns your Amazon listing and why that matters more than you think is often the question that determines whether seller sprawl can be fixed at all.

The damage spreads outside Amazon

The commercial fallout rarely stays inside one marketplace account.

- Margins tighten. Price competition resets expectations and makes premium positioning harder to defend.

- Retail partners push back. Stores and distributors lose trust when marketplace pricing undercuts them without warning.

- Brand signals get muddied. Mixed seller standards create inconsistent delivery, packaging, and service outcomes.

- Teams get pulled off growth work. Sales, customer service, and channel managers end up firefighting listing issues and reseller disputes.

One unstable ASIN can create channel conflict well beyond that product page.

Established hardware, appliance, and household brands often get caught out. Their economics often depend on controlled distribution, service reliability, warranty confidence, and consistent price architecture. Amazon can support that model, but only if the brand governs who sells, how the offer appears, and what happens when someone breaks the rules.

The Buy Box is a symptom, not the strategy

Teams can spend months chasing Buy Box share while ignoring the underlying structural issue. If five sellers are competing on an ASIN that should have had one controlled route to market, winning the Buy Box for a week does not solve much.

The core questions are harder and more valuable. Who is authorized to sell? Which entities are allowed on which ASINs? What pricing and fulfilment rules apply? What proof of supply is acceptable? What enforcement follows when those terms are breached?

Brands that answer those questions early protect equity. Brands that avoid them usually watch Amazon answer on their behalf.

How to Protect Amazon Listing Control

Brands lose control on Amazon long before they see a counterfeiter or a hijacked listing. They lose it when they treat protection as a support function instead of a market-entry decision.

A controlled Amazon presence starts with ownership, authority, and enforceable process. If those pieces are weak, the catalogue will drift, seller behavior will set the rules, and the brand will spend time correcting avoidable damage instead of building demand.

The first layer is Amazon Brand Registry. It matters because it gives the trademark owner recognized authority inside Amazon’s system. That changes how quickly a brand can act on listing misuse, content disputes, and IP complaints.

Brand Registry gives you standing

Founders sometimes file Brand Registry late because it looks administrative. That is a mistake.

Amazon describes Brand Registry as the gateway to tools for searching and reporting suspected infringement, protecting product detail pages, and giving brands greater influence over branded listings. Amazon also positions A+ Content and Brand Stores as part of that same ownership layer, which matters because content quality and control are connected inside the platform, not separate workstreams. You can see that across Amazon’s own documentation for Brand Registry, A+ Content, and Transparency.

The practical point is simple. Registry moves a brand from asking for help to operating with recognized rights.

Separate presentation control from enforcement control

These tools do different jobs, and strong operators treat them that way.

Presentation controls

Presentation controls shape how the offer is understood.

- A+ Content gives brands more room to explain use cases, compatibility, materials, and product differences.

- Brand Store creates a cleaner path across the range, which matters when customers need comparison before purchase.

- Content governance keeps titles, bullets, images, and modules aligned across ASINs instead of being edited piecemeal by different parties.

For hardware, appliance, and household products, that work affects more than conversion. It reduces misinterpretation, lowers avoidable returns, and protects the product from being reframed by whoever touched the listing last.

Enforcement controls

Enforcement controls deal with misuse after rules are broken.

- Report a Violation gives brands a formal path to file IP and listing complaints.

- Project Zero can help eligible brands remove counterfeits faster.

- Transparency adds item-level codes that help verify authentic units in categories where diversion or counterfeit risk is high.

I do not advise brands to enrol in every protection program by default. The right stack depends on margin, counterfeit exposure, reseller behaviour, and how expensive one compromised ASIN becomes across the wider channel.

Practical rule: If the plan is “we’ll sort it out when it appears,” the brand has no control system. It has an escalation backlog.

The harder work happens outside Amazon

Amazon’s tools are only one layer. They do not solve weak distribution logic, blurred ownership, or internal disagreement about who has authority to approve changes.

A defensible setup usually includes:

- Authorised seller terms that state who can sell, on which ASINs, and in which marketplace

- Central asset control for images, copy, comparison charts, and packaging claims

- Price governance across Amazon, retail, and distributor channels

- Documented enforcement steps so the business can act without weeks of internal debate

- Clear account ownership by market so international expansion does not create overlapping authority

Before scaling, founders should answer a basic but frequently ignored question: who actually owns your Amazon listing and why it matters more than you think.

That question becomes more important as the business enters new regions. One practical model is to centralise official listings, catalogue assets, and channel governance through a single operating structure across markets. TPR Brands works in that category for established product brands expanding internationally.

What usually fails

Three patterns show up repeatedly.

The first is informal reseller management. Verbal expectations collapse once an ASIN starts producing volume.

The second is using better creative to compensate for weak governance. Better content can improve conversion, but it does not remove unauthorized sellers or fix broken authority.

The third is waiting until a listing is crowded before acting. By then, evidence is messier, enforcement takes longer, and every decision carries channel consequences.

Managing Amazon Listing Control Across Global Markets

International expansion is where Amazon stops behaving like a sales channel and starts exposing every weak decision in your operating model.

A product that performs well in Australia can still fail in the US, UK, or Canada for reasons that have nothing to do with demand. The usual problem is not traffic. It is loss of control across compliance, catalogue structure, fulfilment, and local seller authority, all at the same time.

That matters more for established hardware and consumer brands because international Amazon growth can add revenue while gradually reducing brand value. If each market develops its own version of your claims, packaging standards, service levels, and pricing logic, scale starts to work against you.

Compliance breaks momentum before marketing can help

For hardware and home improvement brands, market entry often stalls at the product level. Australian standards do not automatically satisfy US, UK, or EU requirements. A listing can look ready internally and still run into customs reviews, restricted product classification, missing documentation, or claim issues once the product enters a new marketplace.

I have seen founders treat this as an admin task and pay for that assumption later. Reviews cannot fix a blocked ASIN. Ad spend cannot solve a compliance hold. If the documentation, testing, packaging language, warnings, or certifications were built for the home market only, the launch plan is already weaker than it looks.

This is a control issue, not just a regulatory one. If the business does not know which claims are approved for each country, local teams and resellers fill the gap themselves.

Cross-border catalogue drift is expensive

The next problem is fragmentation.

Once multiple marketplaces are live, small inconsistencies spread fast. One team changes title structure. Another updates images for local conversion. A distributor adds bundles. Someone copies a claim from one market into another where it should not appear. None of these decisions looks serious in isolation. Together they create a catalogue that no one owns.

The commercial cost shows up in several places:

- Customers see different versions of the same product across markets

- Local teams make changes that create compliance or policy risk elsewhere

- Variation structures stop matching, which weakens reporting and ad efficiency

- Distributors and agencies start acting as de facto listing owners

- The brand loses a reliable global source of truth

Once that happens, international growth becomes slower and more political. Teams argue over whose version is correct instead of protecting the asset.

Logistics changes how the brand is judged

Cross-border fulfilment decisions shape customer perception more than many founders expect.

Stock-outs invite third-party sellers into the gap. Long delivery windows reduce conversion and raise support load. Packaging that survives domestic retail may not survive a different fulfilment chain. The customer does not separate those failures into operations, channel, and marketplace issues. They assign the whole experience to the brand.

That is the strategic trade-off. Expanding into another Amazon marketplace can increase reach, but if service levels are unstable, the business is buying short-term sales with long-term brand dilution.

A better entry plan asks narrower questions first:

- Which SKUs are ready for this market

- Which claims, warnings, and product details need to change before launch

- Who approves listing changes across every marketplace

- Which seller accounts are authorized by region

- What stock, service, and returns model protects review quality

The right answer is usually selective expansion, not broad expansion.

Scale after the control model is proven

Founders often feel pressure to replicate home-market success quickly. The better move is to treat each new Amazon marketplace as a control test. Launch the products that can clear local requirements, hold their margin after marketplace and logistics costs, and stay under central catalogue authority.

That is why the sequence matters. Entering new markets without a defined operating model gives Amazon, local partners, and channel friction more influence over the brand than the brand has over itself. A more disciplined approach is to set market, catalogue, compliance, and seller governance before launch. This guide on Amazon expansion into new markets is a useful reference for that planning.

International Amazon growth is not one repeatable playbook copied across countries. It is a series of market-specific control decisions, and each weak decision reduces the brand’s ability to protect price, presentation, and trust at scale.

When to Scale Amazon Without Losing Control

Amazon scale is only valuable if the brand keeps authority while it grows.

For established hardware and consumer brands, that is the decision. Not whether Amazon can drive volume. It can. The question is whether that volume comes with terms that weaken pricing control, channel relationships, catalogue accuracy, and customer access over time.

I have seen brands mistake Amazon growth for brand growth. They are not the same. A business can post strong marketplace revenue while losing control of the assets that support margin and enterprise value.

Dependency changes your bargaining position

Once Amazon becomes a large share of online revenue, internal decisions start bending around the platform. Teams tolerate fee increases, policy changes, listing suppressions, and fulfilment requirements they would have challenged earlier, because the commercial exposure is too high.

That dependence is well documented. The ACCC’s 2023 Digital Platform Services Inquiry report examined how large platforms can impose changes that business users have limited ability to resist, especially when those platforms control access to demand: ACCC Digital Platform Services Inquiry 2023-24 Interim Report No. 6.

Founders need to stay clear-eyed. A marketplace that produces meaningful revenue can still reduce strategic flexibility. If one account suspension, reimbursement dispute, or policy revision can disrupt the quarter, Amazon is no longer just a channel. It is setting operating conditions for the business.

A healthier model uses Amazon, but does not organise the whole business around it

Strong brands define Amazon’s role before they pursue scale. That usually means setting limits.

- What share of total online revenue can sit on Amazon before concentration risk becomes unacceptable?

- Which SKUs support the brand on Amazon, and which should stay in retail, distribution, or DTC?

- How much price visibility and channel conflict can key retail partners tolerate?

- Who owns catalogue decisions, and who can approve changes that affect claims, bundles, or positioning?

- What customer data, remarketing access, and repeat-purchase economics are lost when Amazon takes the transaction?

Those are portfolio questions, not marketplace questions. Founders who answer them late often discover that Amazon has already trained the organization to prioritize short-term sell-through over channel quality.

Retail partners notice that drift quickly. If Amazon becomes the reference price, or if marketplace listings undercut the in-store story, trust drops. Rebuilding that trust usually costs more than the incremental Amazon revenue that caused the problem.

Scale only after the economics and governance are proven

The wrong moment to expand is when the business needs Amazon to solve a growth problem. That is when brands accept weak margins, broad discounting, patchy seller controls, and operational shortcuts they would reject in any other channel.

The right moment is less exciting and far more effective. Scale after the account structure is settled, authorized seller rules are enforced, listing ownership is clear, and the unit economics still work after fees, freight, returns, compliance costs, and support overhead.

A practical test is simple. If growth on Amazon would force the business to compromise price discipline, retailer relationships, or catalogue control, the business is not ready to scale. If Amazon can add revenue without taking strategic control, then expansion makes sense.

That is the principle behind this article’s title. Brands do not lose control on Amazon in one dramatic event. They give it away in a series of small decisions that look commercially reasonable in isolation.

What is Amazon listing control?

Amazon listing control is the ability to manage who sells your products, how listings appear, and how pricing and brand presentation are enforced.

Why does listing control matter?

It protects pricing discipline, retailer relationships, customer trust, and brand consistency.

Can multiple sellers damage a brand on Amazon?

Yes. Poor seller governance often causes pricing drift, inconsistent customer experience, and weaker marketplace authority.

How do brands regain Amazon control?

Through Brand Registry, seller governance, authorized reseller rules, and centralized listing ownership.

Most brands don’t have an Amazon demand problem. They have an Amazon control problem.

If your listings, pricing, sellers, and market structure aren’t tightly governed, growth usually makes the problem worse—not better.

TPR Brands helps established product brands build stronger Amazon control systems across sellers, markets, and channels before scale creates expensive problems.

It’s worth taking a proper look at what’s really happening underneath.