Most advice on entering the Australian construction channel still starts in the wrong place. It starts with product fit, distributor access, retail pull-through, and price architecture. Those matter, but they don't tell you whether the channel around your product is stable enough to protect your brand when work stalls, claims drag on, or a builder collapses midway through delivery.

For hardware, home improvement, and building-adjacent brands, Australian insurance builders are not just contractors with policies in place. They're a signal. Their insurance position often reveals how disciplined they are operationally, how seriously they document risk, and how likely they are to stay commercially intact when conditions tighten.

One pattern we continue seeing across multiple marketplace ecosystems is that brands overestimate the value of visible distribution and underestimate the importance of partner resilience. In Australia, that mistake is expensive. A builder's insurance setup isn't an admin detail sitting in the background. It's part of the channel's operating system.

Your Partner's Risk Is Your Brand's Risk

A common assumption in market entry is that if the product is strong and the local partner is well connected, the rest can be managed later. In the Australian construction channel, that's backwards. The partner's ability to absorb disruption often matters more than their ability to place an opening order.

When a builder fails, the damage doesn't stay neatly contained inside their own business. It spreads to projects, suppliers, homeowners, installers, and any product brand visible on site. That includes brands whose goods were specified into jobs, promoted through builder networks, or associated with the finished outcome.

Insurance doesn't remove channel risk

Compulsory builder-related insurance in Australia is often framed as a safety net, but that framing can create false confidence. ABC News reported that this insurance is often a last resort and can leave consumers waiting for payouts when builders go bust, with one example from QBE showing a liability cap of $100,000 per unit.

That gap matters commercially. If an end customer believes “the job is insured” and then discovers recovery is delayed, capped, or narrower than expected, they rarely separate the builder's failure from the broader project ecosystem. They remember the kitchen brand, the door hardware brand, the waterproofing system, the appliance package, and the merchants involved.

Commercial reality: In a stressed project, customers don't audit contractual boundaries with much sympathy. They attach blame to whichever brands were most visible.

Why this matters for product brands

For a manufacturer assessing Australian entry, insurance should be read as a proxy for partner discipline. A builder with current cover, clear documentation, and realistic contract positioning usually runs a tighter operation than one treating insurance as a box-tick at tender stage.

That's especially important if your products sit inside:

- Defect-sensitive categories such as waterproofing, fasteners, roofing components, sealing systems, and joinery inputs

- Delay-sensitive projects where site shutdowns can trap stock, disrupt installation sequencing, or trigger disputes over storage and replacement

- Trust-dependent channels where referral reputation matters as much as direct sell-in

Brands that expand well tend to treat partner risk as part of channel design, not as a legal footnote after the deal is signed. That same logic sits behind broader control decisions during expansion, especially when businesses are trying to scale without handing away too much authority early, as discussed in this view on expanding to Amazon without losing control.

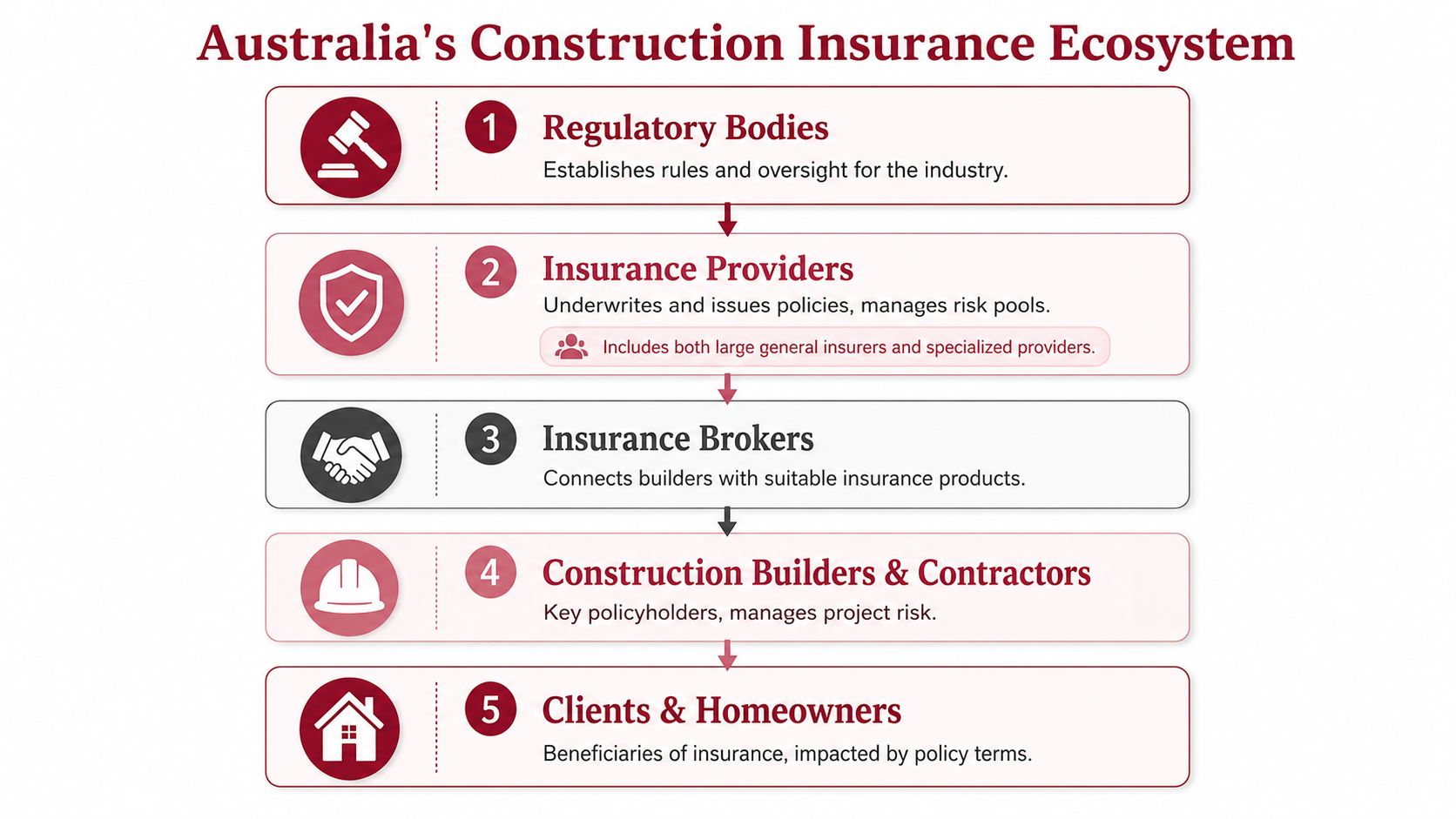

The Australian Construction Insurance Ecosystem

The mistake many overseas brands make is treating builder insurance as back-office admin. In Australia, it is a market signal. It reflects insurer appetite, catastrophe exposure, and how much operational variance the system is willing to tolerate at any given time.

The broader insurance market sets the terms builders live with. The Insurance Council of Australia's 2025 fact pack reports 88 general insurance companies operating in Australia and industry profit of $5.1 billion for FY24. The same publication says insured losses from extreme weather reached $22.5 billion over the five years to 2024, averaging $4.5 billion per year, which was 67% higher than the prior five-year period. Those are not construction-only figures, but they matter to construction because weather-driven claims affect reinsurance costs, underwriting caution, and claims capacity across the market.

Concentration changes procurement risk

Capacity is not evenly distributed. The Wikipedia overview of insurance in Australia, citing market share references for the local general insurance sector, notes Insurance Australia Group at about 29% market share, Suncorp at 27%, QBE at 10%, and Allianz at 8%. It also notes IBISWorld's projection that industry revenue is expected to reach $77.4 billion in 2024–25 and grow to $92.1 billion by 2029–30 at an annualised 3.5%.

For a brand building an Australian channel, the practical issue is concentration. If a small group of underwriters tightens terms around water ingress, combustible materials, rectification work, regional exposure, or subcontractor controls, the effects move quickly through builder pricing and partner selection.

That pressure shows up in commercial places brand teams often miss:

- Tender assumptions drift when insurance pricing or exclusions change between quote stage and contract placement

- Work-type appetite narrows when builders avoid jobs that are harder or more expensive to insure

- Approved installer pools shrink when insurers or head contractors favour operators with stronger documentation and claims records

- Product exposure increases when disputed causation pulls manufacturers into defect arguments, especially in categories tied to moisture, fire, structural fixing, or building envelope performance

That last point is why product liability insurance issues in construction-linked channels belong in market-entry planning, not just legal review after launch.

Why insurance builders sit in a different operating category

Insurance builders work inside a claims-driven delivery model. Their jobs often begin with damage assessment, emergency stabilisation, strip-out, repair scope validation, and insurer approval workflows before standard rebuild activity even starts. That creates a different commercial profile from ordinary residential construction. Documentation discipline, response time, subcontractor control, and dispute handling matter as much as build quality.

For product brands, this channel can be attractive and difficult at the same time. Claims work can create repeat demand, specification opportunities, and multi-site volume. It can also produce abrupt swings in workload after weather events, tighter scrutiny on substituted products, and more argument over causation when failures appear after reinstatement.

The result is simple. A builder active in insurance repair may have good revenue and still be under margin pressure, claims pressure, or insurer panel pressure. Those conditions affect ordering reliability, product substitution risk, complaint volume, and the likelihood that your brand gets pulled into a problem that started as an underwriting or scope-control issue rather than a product defect.

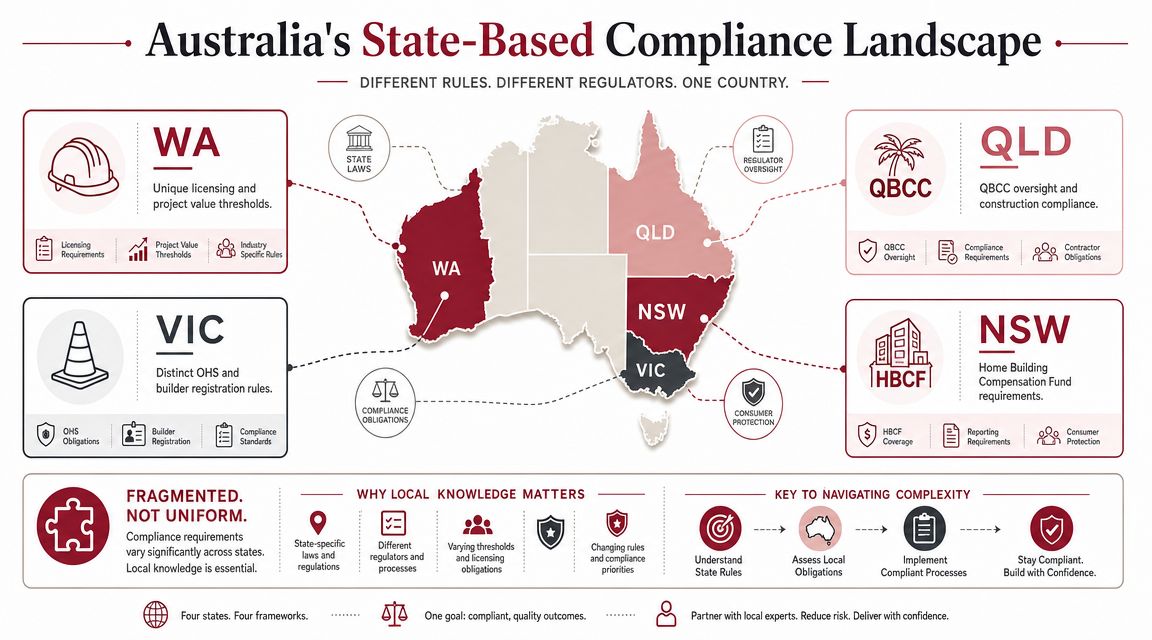

Navigating State-Based Compliance Fragmentation

Many offshore teams still talk about Australia as if it were one compliance environment with one set of construction rules. It isn't. It's one country with multiple state-based systems, different scheme names, different regulator behaviour, and different operational habits around licensing, certification, and insurance.

That fragmentation creates practical strain for builders trying to work nationally. It also gives brands a useful filter. If a channel partner says they operate “Australia-wide”, the next question shouldn't be about sales capacity. It should be whether they can manage compliance state by state without improvising.

National language hides local complexity

Domestic building insurance and home warranty style protections don't operate under one clean national template. Names, thresholds, triggers, and administration differ across states and territories. The result is predictable. A partner can be competent in one state and exposed in another.

That matters for brands supplying:

- Multi-site builders rolling the same product range across different jurisdictions

- Repair and rectification networks where claim work can cross borders

- Commercial teams assuming one approved partner can cover the full country with the same governance standard

One issue we repeatedly observe during international expansion is that localisation failure rarely begins with language. It begins with hidden operational assumptions. That's as true in construction as it is in digital marketplaces, and the same pattern sits behind why some products feel closer than others during marketplace localisation.

Hardening insurance makes fragmentation more costly

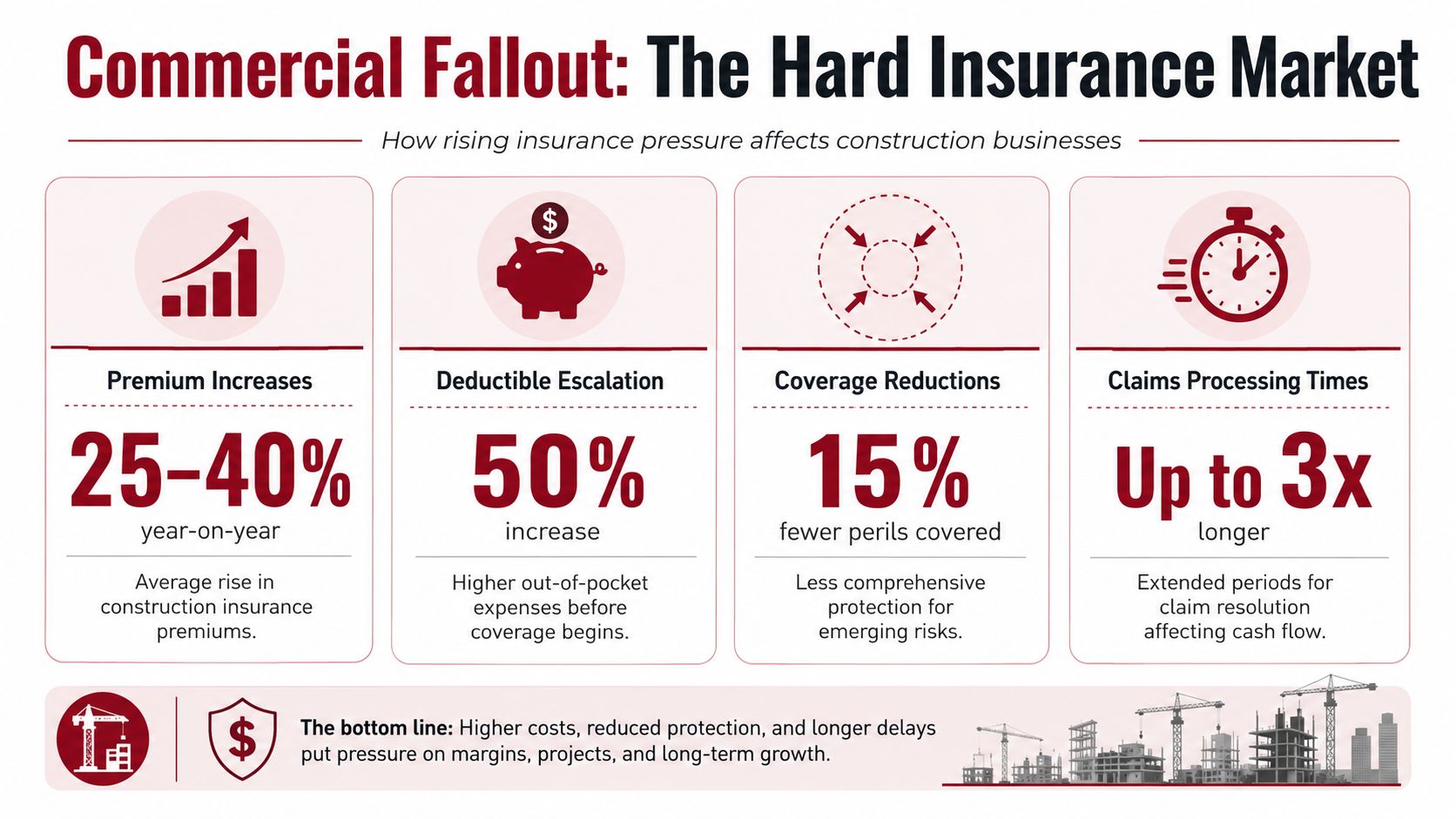

Marsh reported in its Australian mid-year construction insurance update that premiums were still rising across property and liability classes even as the pace of increases began to moderate, and that larger contractors faced the hardest market conditions because some insurers pulled back capacity in higher-risk areas. It also noted tighter underwriting, stricter scope documentation, and slower placement for jobs with higher risk profiles such as water ingress or structural defects.

When you place that on top of state-by-state compliance variation, the burden on builders increases fast. They need to satisfy local rules and insurer scrutiny at the same time.

State fragmentation doesn't just create admin. It creates different failure points, depending on the job type, the insurer appetite, and the jurisdiction.

What to ask before approving a partner

A brand doesn't need to become a legal practice to assess this properly. It does need to ask better operational questions.

| Question | Why it matters |

|---|---|

| Which states do you actively deliver in today? | “Can service nationally” is weaker than proven active coverage. |

| How do you manage insurance and licensing differences across jurisdictions? | Good operators have a process, not a vague assurance. |

| Who owns compliance internally? | If nobody owns it, problems surface late. |

| How do you handle scopes involving defects, water ingress, or rectification? | These are exactly the jobs where underwriting friction tends to appear. |

A better reading of national capability

National reach in Australia isn't just about depot coverage or account management. It means a partner can keep documentation, insurer communication, and project governance coherent while crossing different local frameworks.

For product brands, that's a meaningful distinction. A builder that can work across jurisdictions with consistent process is often more reliable than a larger-looking operator stitched together through opportunistic subcontracting. In this channel, administrative coherence is commercial strength.

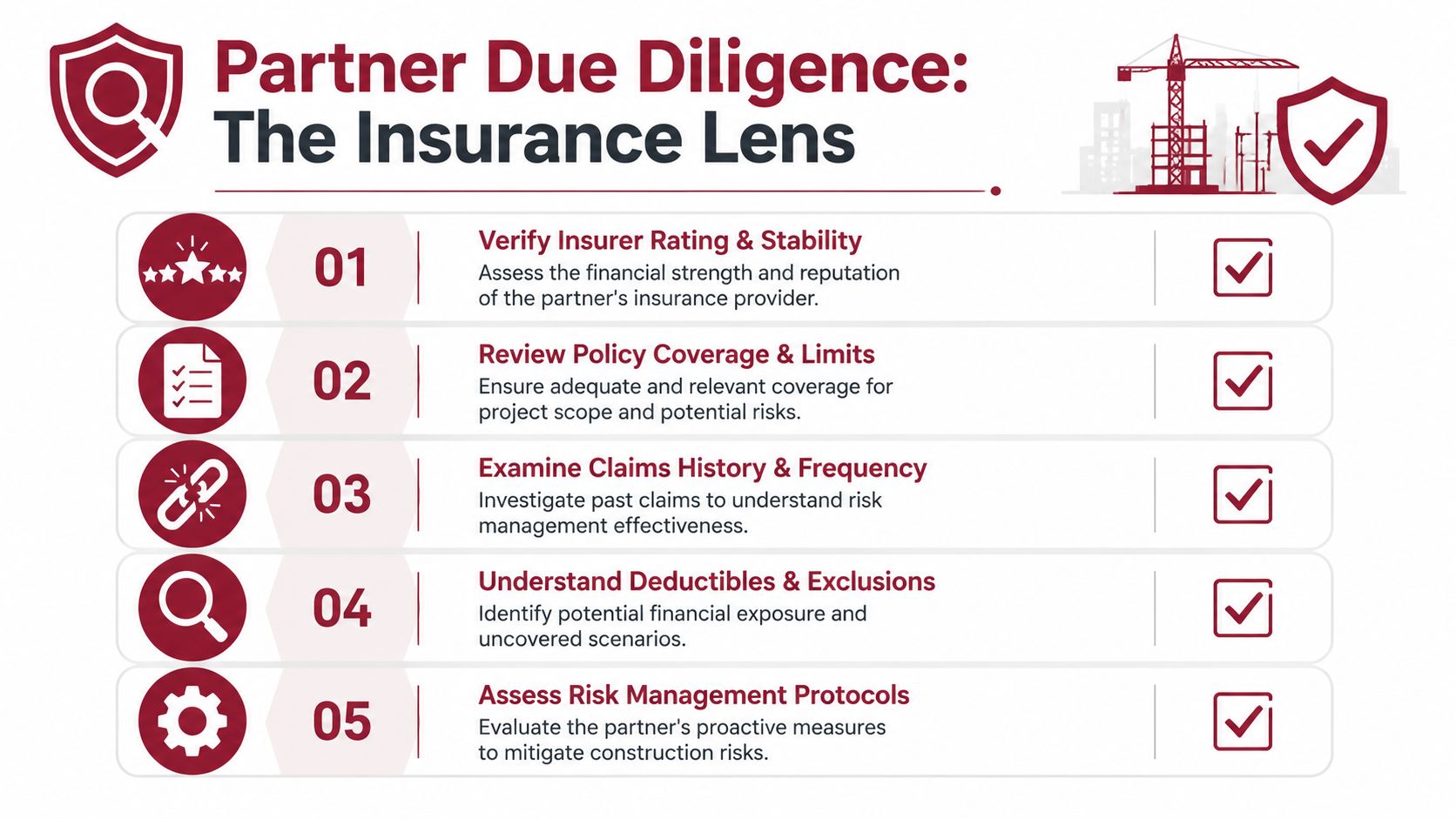

Using Insurance as a Partner Due Diligence Tool

Brands often overrate the sales presentation and underrate the insurance file. In Australia, that is backwards. A builder's insurance position is one of the clearest low-cost signals of how tightly the business is run, especially if your products will sit inside rectification work, insurance-funded repairs, or multi-state delivery programs.

A Certificate of Currency is only a starting point. Used properly, it helps separate partners with controlled operating discipline from partners held together by good account management and late-stage scrambling.

Read the document as an operating signal

Validity matters, but behaviour around the document matters more. A current certificate can still sit inside a business with weak controls, poor entity structure, or unclear scope boundaries. Those problems rarely stay confined to insurance. They spill into approvals, product substitution, reporting quality, and claim handling once a project comes under pressure.

The first read should focus on a few practical checks:

- Entity alignment. The insured name should match the legal entity signing your agreement and buying your product.

- Scope consistency. The cover should make sense for the actual work the partner performs, not a broader or vaguer version of it.

- Renewal discipline. Prompt, current documents usually indicate someone owns the process internally.

- Document control. Clean versions, correct dates, and quick turnaround suggest stronger back-office governance.

- Broker engagement. Clear answers from the broker usually point to a partner that manages insurer communication before problems become urgent.

One missed renewal does not make a builder unviable. A pattern of vague answers, mismatched entities, and last-minute paperwork should change your risk view quickly.

What insurance diligence tells a manufacturer

Insurance review works best as a proxy test. It does not tell you whether a partner is good at selling your range. It does tell you whether they are likely to create avoidable friction once they are carrying your brand into jobs where defects, delays, or client complaints can trigger scrutiny.

The stronger operators usually show the same traits. They have a defined intake process for new work. They document incidents in a repeatable format. They can explain who owns claims liaison, who approves subcontractor use, and how rectification scopes are reviewed before crews are dispatched. Those are commercial controls, not insurance trivia.

For a product brand, that distinction matters. A builder with average scale and disciplined process is often a safer channel partner than a larger operator relying on informal workarounds between offices, supervisors, and subcontractors.

Here's a useful reference point from a practical insurance perspective:

A practical due diligence screen

Keep the review commercial. The goal is not to audit the partner like an insurer would. The goal is to judge whether their operating discipline is strong enough that an insurance issue does not become your stock problem, your service problem, or your reputation problem.

Due diligence test: If a partner cannot explain their insurance position in plain language, they are unlikely to explain a claim dispute clearly when your products are tied to the job outcome.

A short screening checklist is usually enough:

- Does the insured entity match the contracting entity?

- Does the stated cover fit the work types they want to perform with your brand?

- Can they produce current documents without repeated chasing?

- Can they explain how incidents, defects, and claims are documented and escalated?

- Can they show a consistent operating method across the regions where they claim capability?

Commercial teams often get caught spending weeks testing pricing logic and rebate mechanics, then treat insurance as a tick-box collected by procurement. In the Australian construction channel, insurance records often give a better read on partner reliability than the capability deck does.

Decoding the Commercial Impact of Insurance Volatility

Insurance volatility looks like a builder problem until it starts changing your own economics. Then it becomes a channel problem.

In a hardening market, weaker operators often absorb stress badly. They delay renewals, hope wording issues won't matter, trim cover where they can, or accept work that doesn't sit comfortably inside their insurance position. None of that appears in the pitch deck. It shows up later in delivery friction, pricing disputes, and cash pressure.

Sophisticated builders price reality early

Pinsent Masons notes in its analysis of the Australian market that the infrastructure insurance environment had “hardened significantly over the past 18 months”, with higher premiums, drawn-out insurer response times, and more common last-minute wording changes. Its practical advice to contractors is to reflect higher premiums in tender pricing, begin renewals early, and consider carve-outs or liability sub-caps for uninsurable risks.

That's not just legal advice. It's a marker of commercial maturity.

A stronger builder will usually:

- Price insurance pressure into bids rather than relying on unrealistic assumptions

- Start renewal conversations early to avoid late surprises near project commencement

- Push for cleaner risk allocation when certain exposures can't be insured on sensible terms

A weaker builder often does the opposite. They win the work first, then scramble to make the insurance stack fit.

What brands should infer from partner behaviour

If your Australian channel depends on builders specifying, installing, or representing your products, their response to insurance pressure affects your planning in several ways.

| Partner behaviour | What it usually means for the brand |

|---|---|

| Early disclosure of insurance cost pressure | Better forecasting and fewer margin shocks |

| Clear contract carve-outs | Lower chance of disputes being redirected into product blame |

| Late-stage insurance issues | Higher risk of delayed starts and unstable purchase commitments |

| Vague answers on exclusions or renewal timing | Elevated governance risk |

The point isn't to avoid every builder facing insurance pressure. That isn't realistic. The point is to avoid partners who hide it until it becomes your problem.

One pattern we continue seeing is that advanced channel partners don't pretend volatility isn't there. They operationalise around it. For a product brand, that distinction matters far more than whether the partner looks impressive in a capability deck.

When Claims Happen How Channel Disruption Unfolds

The most expensive misunderstanding in this space is thinking that “insured” means “commercially protected”. It doesn't. A policy can exist, a claim can still be disputed, and the project can still seize up while everyone argues about scope, causation, responsibility, and timing.

That's where channel disruption becomes visible.

The disruption rarely stays on site

Take a fairly ordinary failure sequence. A builder is working through a project involving multiple supplied products, several trades, and a tight handover schedule. A site incident happens. It might be a fire, a theft event, a water issue, or an allegation of damage to adjoining property.

The claim is lodged, but the insurer asks for more detail. Questions start appearing around workmanship, sequencing, prior defects, moisture source, or whether the loss falls cleanly inside the policy terms. While that's being worked through, the builder slows purchasing, site access becomes constrained, and the principal starts looking for someone to blame.

The brand may not be at fault at all. But if its products are installed, visible, delayed, or discussed in the dispute, it gets pulled into the noise.

Where product brands get caught

This is usually how the disruption spreads through the channel:

- Inventory exposure: Stock already delivered to site can become hard to retrieve, inspect, or reallocate.

- Installation ambiguity: If goods were partially installed, arguments can emerge over replacement responsibility, damage causation, or whether materials contributed to the issue.

- Public dispute risk: Customers and developers often collapse distinctions between builder failure, insurer response, and supplier involvement.

- Future pipeline drag: Other channel partners may pause or reduce orders if they believe your brand is tied to a problematic project cohort.

Why exclusions and stress matter together

Many policy disputes become dangerous when they hit a builder already under financial pressure. A denial, reservation, or delay doesn't just create inconvenience. It can remove the cash-flow bridge the builder was relying on to keep the project moving.

A financially stretched builder can survive a small operational problem. They often can't survive a claim event that turns into a long argument.

For brands, the strategic lesson is straightforward. Don't assess partner insurance as if the only question is whether a certificate exists. Assess whether the builder could stay functional if a claim becomes messy, slow, or only partly recoverable.

That means asking different questions during onboarding. How are incidents documented? Who manages claim communication? What happens operationally if a site is suspended? How quickly can stock be accounted for, quarantined, replaced, or redirected?

Good channel design assumes claims friction will happen somewhere. It doesn't assume every claim will resolve neatly and on time.

Building a Resilient Australian Channel Strategy

Australian channel expansion in construction-adjacent categories doesn't fail because the market lacks demand. It usually falters because brands misread the operating environment around demand.

A builder's insurance position is one of the clearest indicators of that environment. It tells you how seriously the partner treats documentation, how exposed they may be to underwriting shifts, and whether they're likely to remain reliable when the market tightens. That's why Australian insurance builders matter beyond the insurance niche itself. They sit at the intersection of compliance, delivery, and commercial resilience.

The practical takeaway is not to become an insurance expert. It's to build insurance awareness into partner selection, account planning, and channel governance. Brands that do this well don't just ask whether a builder can sell or install their product. They ask whether that builder can stay stable under pressure, preserve customer trust, and keep the broader channel intact when conditions get less forgiving.

That same principle applies more broadly across Australian expansion. Strong products still need strong ecosystem design, especially in channels where local operating discipline shapes brand perception as much as product quality. For teams thinking about how to structure that expansion more coherently, Amazon Australia channel planning is one example of where ecosystem decisions and commercial control need to be considered together from the outset.

TPR Brands helps established product companies expand into new channels and regions with more control, better localisation, and a clearer view of the ecosystem risks that affect growth. If you're assessing the Australian market and want a more commercially grounded perspective on channel structure, partner quality, and scalable expansion, explore TPR Brands.