The most popular advice about moving from Australia to Amazon US is also the least useful. It usually starts with listings, PPC, and launch timing, as if the main challenge is getting seen.

That's rarely where established brands come unstuck.

One pattern we continue seeing is brands treating US expansion as a bigger version of an Australian marketplace program. More ad budget. More inventory. More keywords. Slightly adjusted copy. The logic sounds sensible until the first serious shipment lands, the cost stack changes shape, and the commercial model that worked in Australia stops making sense.

For founder-led product businesses, from australia to the us: what most brands get wrong about amazon expansion comes down to two structural failures. They don't protect margin across a transpacific operating model, and they don't treat US compliance as a gatekeeping function. Everything else sits downstream of those mistakes.

The Scale Illusion Why US Expansion Fails Before It Begins

The first mistake isn't tactical. It's conceptual.

Australian brands often assume that domestic Amazon traction proves international readiness. In practice, local success can hide the fact that the underlying marketplace conditions are completely different. Amazon in Australia has grown quickly, with revenue rising to A$1.936 billion in 2024, yet it still represents only around 5% of total online sales. In the US, Amazon accounts for roughly 40% of all e-commerce, with about 1.1 million active sellers in 2025, according to this review of Amazon Australia filing results and US marketplace context.

That gap matters because it changes everything. Search behaviour is different. Competitive density is different. Review thresholds are different. The range of acceptable pricing is different. Even buyer trust forms differently because the marketplace is far more mature and far more crowded.

Australia success is not US proof

A catalogue that performs well in Australia may be riding on a smaller, less saturated demand base. The US asks harder questions of the same product.

- Inventory pressure rises earlier. Brands hit stock planning problems sooner because demand can move faster and replenishment errors cost more.

- Advertising waste becomes more visible. A weak launch structure gets punished quickly when competition is deeper.

- Operational gaps surface faster. Freight timing, returns handling, and contribution margin stop being back-office details.

The US isn't a scale-up exercise. It's an ecosystem change.

That's why treating the US as a larger version of Australia is a category error. The channel economics are different at a structural level, not just a budget level.

What stronger operators do first

They stop asking whether the product “should work” in the US and start asking whether the business is built for US marketplace conditions.

A recent marketplace review revealed the same pattern across several product categories. Teams that entered well usually rebuilt assumptions from the ground up. They reworked pricing logic, stock cover, review generation expectations, and fulfilment tolerance. Teams that struggled tried to extend the Australian playbook.

If you're evaluating Australian products in the USA, the useful framing isn't market size alone. It's whether your product, margin structure, and operating model can survive a marketplace that behaves by different rules.

The Copy-Paste Catastrophe Where Margins Go to Die

The second mistake is operational, and it's expensive.

Many brands still approach Amazon US as a catalogue transfer. They adapt the title, convert the currency, ship the stock, and assume the rest can be optimised after launch. That works just well enough to create false confidence, because early sales can mask weak economics.

The common failure mode is simpler than often acknowledged. Margins disappear. As noted in this guidance on expanding from Amazon Australia to the US and UK, brands often misprice freight, exchange-rate exposure, duties, returns, and promo spend, then realise the launch looks healthy on top-line sales but weak on contribution margin once replenishment lag, higher CPCs, and compliance costs are included.

Why localisation is an economic issue

Localisation gets framed as a marketing exercise. In reality, it's a commercial control mechanism.

US customers read value differently. They compare more aggressively. They're exposed to denser review environments. They also respond to local trust signals, category language, and pricing architecture that may not match what worked in Australia. A premium Australian brand can arrive in the US looking oddly expensive, thinly validated, or vaguely offshore.

That's where copy-paste launches break.

| Area | What brands assume | What actually happens |

|---|---|---|

| Pricing | Currency conversion is enough | Freight, duties, returns, and ad pressure shift the viable price point |

| Listing copy | AU messaging will travel | US shoppers often need different proof, positioning, and terminology |

| Reviews | Existing brand strength will carry trust | Sparse local review density can suppress conversion |

| Promotions | Initial discounts can fix momentum | Promo spend can hide weak unit economics rather than solve them |

The hidden problem is false profitability

One issue we repeatedly observe is that founders look at gross sales and feel reassured, while the P&L is deteriorating behind the scenes.

A launch can generate movement and still be commercially wrong. That's especially true when a team hasn't localised packaging assumptions, price architecture, or customer expectation around delivery and returns. Revenue arrives first. Margin leakage follows.

Operational rule: If the only thing you've localised is the listing copy, you haven't localised the business.

Here, a lot of “good products” become weak marketplace businesses. The product may still be sound. The channel model isn't.

For brands already seeing this tension, why your product sells on Amazon but makes less money is often the more relevant question than how to improve conversion rate. Better conversion on a bad cost base only scales the mistake.

What works instead

The better approach is slower and less glamorous.

Rebuild the unit economics for the US market before launch. Reassess what price the product can hold once all landed costs sit inside the model. Then decide whether localised positioning can support that price without forcing unsustainable ad dependence. If it can't, the issue isn't listing optimisation. It's market fit at the margin level.

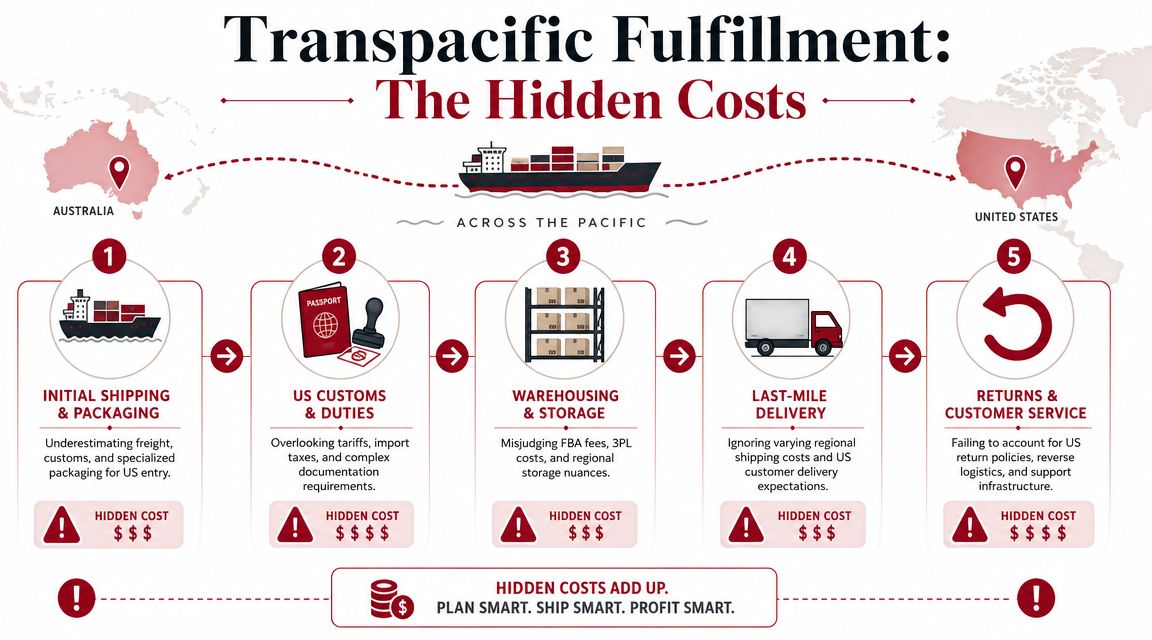

Miscalculating the True Cost of Transpacific Fulfilment

A weak fulfilment plan doesn't usually fail on day one. It fails after the first wave of sales, when cash gets trapped in transit, replenishment falls out of sync, and the business starts funding urgency.

That's why the freight discussion is usually too shallow. It gets reduced to FBA versus 3PL, when the underlying issue is whether the brand has fulfilment confidence across a long, exposed supply chain.

Australian operators usually know logistics well. That's not the same as being prepared for US Amazon logistics. The challenge isn't merely moving inventory further. It's managing a chain with more decision points, more cost volatility, and less tolerance for planning errors.

Where the model usually breaks

The pressure builds in layers.

- Freight and packaging assumptions slip. The shipment cost in the spreadsheet rarely reflects the actual cost once packaging requirements, handling, and US entry considerations are finalised.

- Inventory sits in the wrong place. Stock can be technically available but commercially unusable if allocation and timing are off.

- Returns become a structural cost. Reverse logistics in the US needs to be planned, not treated as incidental.

- Working capital gets stretched. Inventory on the water or in staging locations ties up cash while ads, promotions, and operations continue.

The central question isn't how to avoid stockouts. It's when the expansion improves enterprise value. As noted in TPR Brands' article on expanding to Amazon USA, Australian sellers need a framework for modelling working capital tied up in transpacific inventory and identifying which cost buckets break the business case. The practical answer is often phased expansion with conservative unit commitments.

A more realistic way to think about fulfilment

A founder should evaluate US fulfilment as a capital allocation decision, not a shipping decision.

That means testing the model against operational stress, not ideal conditions.

| Fulfilment question | Weak answer | Stronger answer |

|---|---|---|

| How much stock should we send? | Enough to support launch demand | Enough to test demand without distorting cash flow |

| Who handles storage? | Whichever option looks cheapest | The structure that protects speed, control, and margin |

| How are returns managed? | We'll solve it later | We know the path, cost, and owner before launch |

| When do we scale inventory? | Once sales appear | Once replenishment rhythm and unit economics are proven |

Inventory isn't just stock. In cross-border expansion, it becomes working capital, lead-time risk, and margin exposure at the same time.

For hardware, home organisation, and household products, this gets more severe because packaging profile, handling needs, and storage behaviour can alter the economics quickly. The mistake isn't choosing the wrong freight partner. It's launching before the full supply chain has been commercially modelled.

If you're building a global logistics strategy for international expansion, the right question is whether your fulfilment structure can absorb delay, cost variance, and uneven demand without forcing reactive decisions. If it can't, scaling just amplifies fragility.

The Compliance Blind Spot for Product Brands

Many brands spend months refining launch messaging and almost no time asking whether the product is ready for the US regulatory environment.

That imbalance causes some of the most damaging failures in international expansion. A good listing can't rescue a product that needs different documentation, revised labelling, fresh certification, or a clearer importer structure.

Compliance is market access

One issue we repeatedly observe is the assumption that Australian compliance files will transfer cleanly. They often don't.

For hardware, connected devices, consumer goods, and wellness products, US entry can require different conformity evidence, different warnings, tighter document control, and far more clarity about who acts as importer or exporter of record. The question, as argued in this article on what brands get wrong when expanding internationally, isn't “how do I localise listings?” It's which products can be exported from Australia to the US with minimal re-engineering, and which require redesign, certification, or a local compliance partner first?

That shift in thinking matters because it moves expansion from marketing ambition to regulatory readiness.

The products that look easy often aren't

The difficult part is that compliance friction doesn't always appear in obvious categories. Brands expect it in supplements or electronics. They miss it in adjacent consumer products where claims, materials, packaging statements, or safety expectations create new obligations.

A practical review usually needs to cover several layers:

- Product-level evidence. Certifications, safety files, test reports, and any supporting technical records.

- Packaging and labelling. Not just design, but warnings, ingredient panels, origin statements, and claim language.

- Importer responsibility. Someone has to own the legal and documentary side of entry.

- Marketplace exposure. Amazon may request documentation quickly, and weak record-keeping creates avoidable risk.

The moat isn't faster ad spend. It's having launchable SKUs with the right documentation before the market ever sees them.

Why this becomes a strategic advantage

Compliance is often treated as administrative drag. Stronger brands use it differently.

They know that category-specific readiness narrows risk, improves launch sequencing, and protects the account itself. In several premium product categories, the brands that move with confidence aren't always the ones with the loudest marketing. They're the ones that know which SKUs can enter cleanly, which need adaptation, and which shouldn't be prioritised yet.

That discipline also affects speed. Once a business has mapped the categories that are export-ready, commercial decisions improve. Forecasting improves. Inventory decisions improve. Ad spend becomes less speculative because the underlying product base is more secure.

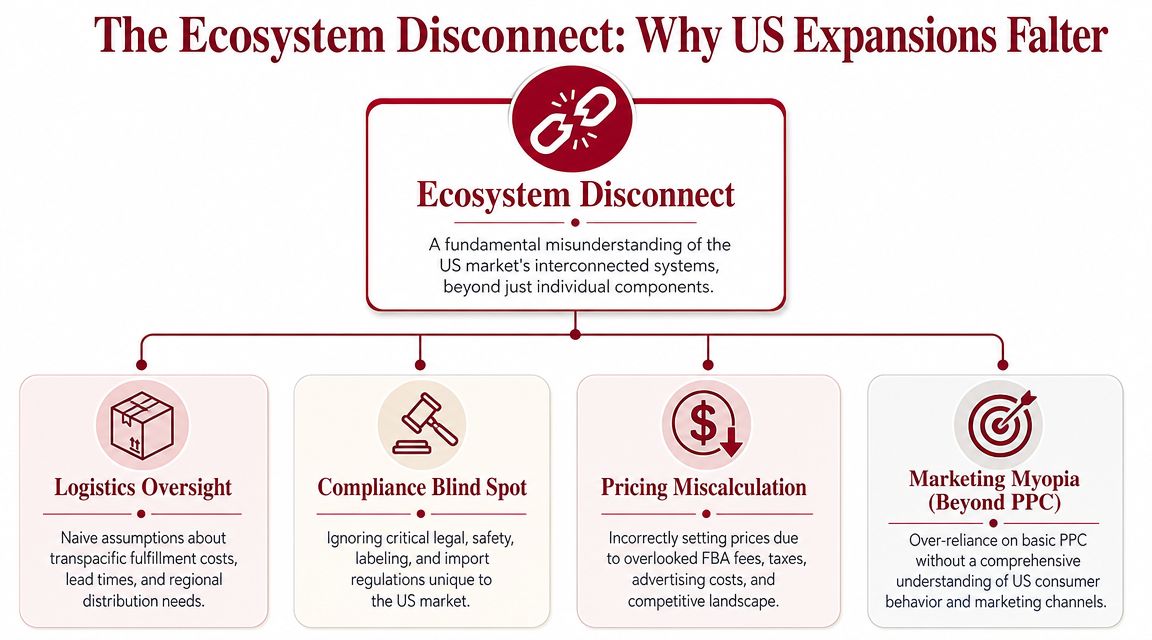

Beyond PPC The Inevitable Ecosystem Disconnect

Most struggling US launches don't suffer from one isolated mistake. They suffer from disconnect between parts of the business that should have been designed together.

Pricing sits in one model. Logistics sits in another. Compliance sits with a supplier or consultant. Amazon performance sits with a marketplace team. The founder sees sales activity, but nobody owns the total commercial system.

That's the deeper issue. Not weak PPC. Not imperfect listings. Ecosystem disconnect.

Why satellite management fails

Expert commentary on international Amazon expansion consistently points to the same structural truth. Each country operates as a distinct entity, with separate legal and regulatory requirements and the need for independent operational oversight, inventory, and budget allocation. Brands should stage entry with enough resources for each market, as outlined in this discussion of international Amazon expansion.

That means the US operation can't be run as a side project of the Australian business.

When it is, familiar symptoms show up:

- Inventory gets planned from AU assumptions

- Pricing ignores the true US cost stack

- Brand assets don't match local trust signals

- Budgets get allocated reactively

- Account management becomes fragmented

What ecosystem cohesion looks like

Across multiple marketplace ecosystems, stronger brands build a US centre of gravity. It might start lean, but it has its own commercial logic.

A cohesive expansion model usually includes:

US-specific economics

The market has its own P&L, not a converted AU worksheet.Dedicated operating oversight

Somebody owns inventory rhythm, compliance status, and channel performance together.Localised brand architecture

Copy, offer structure, review strategy, and customer expectation are aligned to the market.Sequenced growth

Scale follows proof. It doesn't precede it.

Brands don't usually fail because the product is bad. They fail because the US marketplace ecosystem was never built as a coherent commercial system.

This is also where specialist operators become useful. Some brands build that capability internally. Others use external partners who can integrate market entry, logistics, compliance, and positioning into one operating plan. TPR Brands' work on connected product ecosystems is relevant here because it approaches marketplace expansion as ecosystem design rather than isolated channel management.

Why PPC is the least interesting part

PPC still matters. It just isn't the deciding layer in most cross-border failures.

If pricing is wrong, ads accelerate margin loss. If compliance is weak, ads accelerate exposure. If fulfilment is unstable, ads amplify operational strain. Advertising only works as efficiently as the ecosystem behind it.

That's why tactical fixes disappoint founders who are solving a structural problem. The launch doesn't need more activity. It needs alignment.

Building a Commercially Viable US Market Entry Strategy

The brands that enter well usually look less aggressive in the early stages. That's not because they lack ambition. It's because they understand what needs proving before capital gets committed at scale.

A commercially viable US strategy starts with restraint. Not hesitation. Restraint.

The better entry logic

Founders are usually better served by a staged entry model built around decision quality.

- Start with a US-specific P&L. Build the economics around landed cost, fulfilment structure, returns exposure, promotional pressure, and realistic operating overhead.

- Choose launch SKUs selectively. Not every strong domestic product should go first. Prioritise products with cleaner compliance pathways and healthier cost resilience.

- Commit inventory conservatively. Early stock should test demand and operations, not lock the business into an oversized position.

- Define market ownership early. Someone needs clear responsibility for the commercial system, not just the Amazon account.

What experienced operators check before launch

A strong market entry plan can usually answer these questions clearly:

| Commercial question | Why it matters |

|---|---|

| Which SKUs are genuinely US-ready? | Avoids launching products that create regulatory or margin problems |

| What breaks margin first? | Identifies the cost category that deserves the most control |

| How much cash gets tied up in inventory? | Prevents growth from starving the wider business |

| What evidence would justify scaling? | Keeps expansion disciplined rather than emotional |

For established product companies, international marketplace work ceases to be channel management and becomes business design. The objective isn't merely to “be on Amazon US”. It's to build a version of the business that can survive there, scale there, and still protect brand value.

That's also why the right expansion support rarely looks like a generic Amazon service. It looks more like commercial modelling, market adaptation, fulfilment planning, and category-specific risk assessment operating in one conversation.

If you're assessing a US move and want a sharper commercial view before inventory, compliance work, or marketplace spend starts locking in, TPR Brands works with established product brands on the structural side of expansion. That includes market adaptation, channel fit, cross-border readiness, and the operational decisions that determine whether US Amazon becomes a durable growth channel or an expensive distraction.